[#89] The convergence bet: NBFCs are getting TPAP licenses, TPAPs are getting lending licenses. Both sides are betting that NBFC + TPAP is the winning combination for Credit Lines on UPI

NBFCs are building UPI apps. TPAPs want lending licenses. The convergence of NBFCs and TPAPs seems to suggest that NBFCs expect CLOU to be opened to them, and TPAPs are betting on credit to monetize

A few months ago, I wrote about Credit Lines on UPI (CLOU), what it is, why it matters, and why I think it will reshape how credit is distributed in India. My thesis was straightforward: CLOU has the potential to turn every UPI transaction into a credit transaction but only if certain pieces fall into place. The biggest missing piece? NBFCs.

Today, only banks can offer credit lines on UPI. But the entities that actually do small ticket lending in India, the ones for whom a INR 10,000 credit line is core business are NBFCs. That disconnect has been bugging me. So I went digging. I pulled NPCI’s TPAP registry, RBI’s full NBFC list, UPI volume data across four quarters, and license records across NBFCs, PPIs, and UPI apps. There’s a pattern that has emerged, that seems to be point to unlock coming.

![[#81] Credit Lines on UPI (CLOU) will eat small ticket lending, but requires key ecosystem unlocks to reach that inflection point](https://substackcdn.com/image/fetch/$s_!htjJ!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ff56133cc-88b7-43cc-8957-d0d9a07af9e0_1684x950.png)

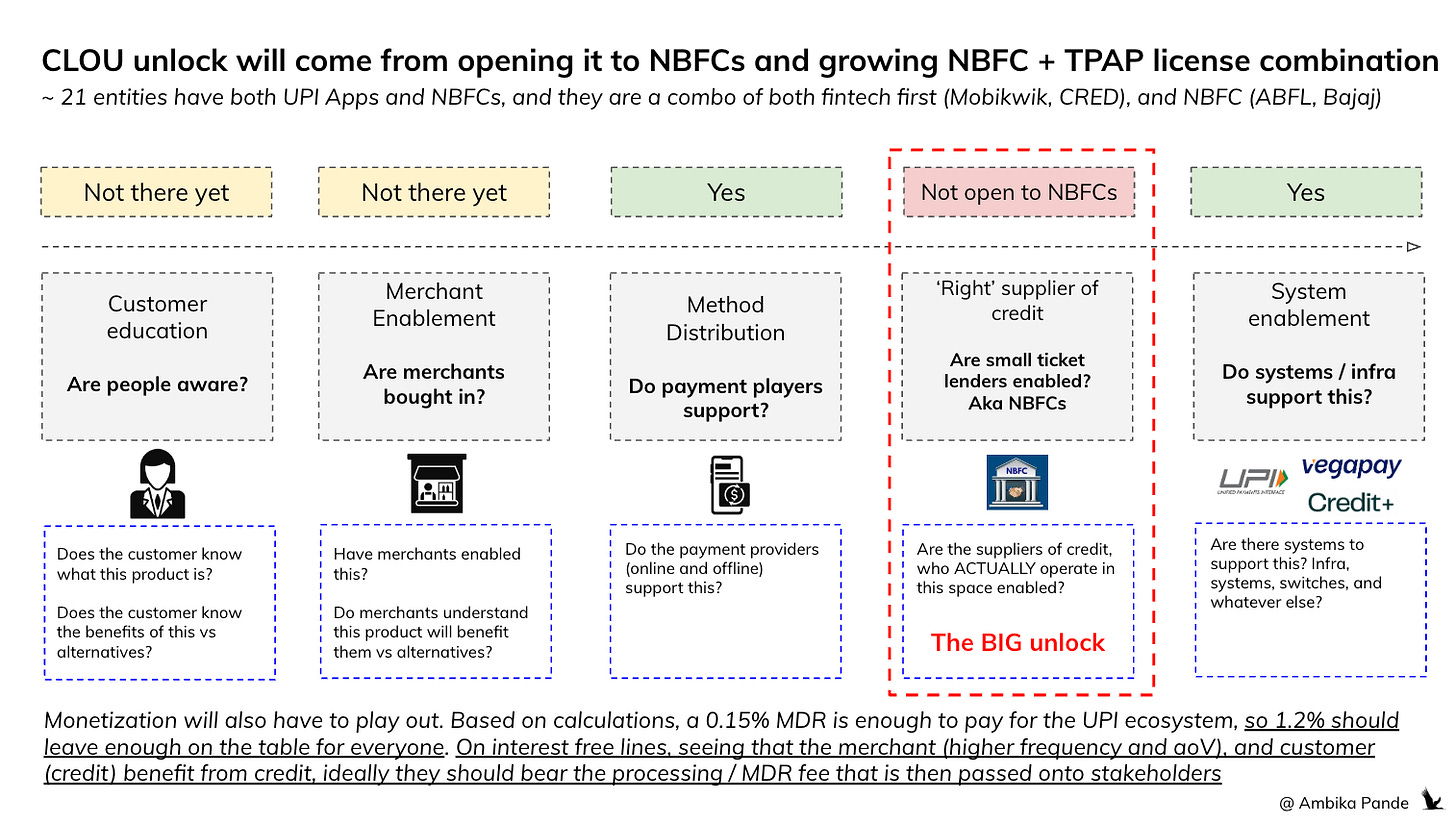

TLDR. I’m bullish on the concept of Credit Lines on UPI, but subject to certain unlocks happening the ecosystem. I see five unlocks that need to happen for this to work:

Does the customer know about this and understand this product? Not to the extent that is needed, but I’d say that with the recent launches of Paytm and BharatPe, we are getting there 🟡

Do merchants understand this product, and the value it brings to them: Again, I’d say similar to the previous point. Not to the extent that is needed for this to take off, but something that is evolving. (example: credit increases frequency and average transaction value) 🟡

Do the payment players support it at the time of transaction? Example, at online checkout, and offline POS terminals, can customers see this as a way to pay? 🟢

Is the right supplier of credit enabled for this? Example: NBFCs are the entities that power small ticket lending in India, not banks. If they are not enabled, then the supply will never truly be there to help scale this 🔴

Are systems enabled? Are there credit line management systems? Is the infra ready? Can apps enable this? 🟢

Why is the NBFC unlock the ‘magic’ answer to everything?

Because Credit Lines on UPI (CLOU) is inherently seen as small ticket lending. Credit lines start at around INR 10,000 on average (which could go lower) but this is a good starting amount. Now, who are the credit suppliers that do small ticket lending in India today? NBFCs!

So by opening this to just banks, you’re not really solving any problem per se in terms of supply. This was never REALLY a product that banks were going after. So by telling banks “hey - you can now give credit lines on UPI” is like telling banks, hey now you can start a cab service. It’s not a great analogy but you get my point - opening it up to banks doesn’t mean banks are going to do it; it’s not like this was a strategic area of focus for banks anyway.

You have to open this up to the entities for whom this is a core business. Which are NBFCs. And then that is also what will drive point 1 and 2 in terms of what is needed to unlock this: customer and merchant awareness. There is credit demand in India. Credit has grown across sectors (industrial, personal loans, agri, service sector, real estate in double digit numbers). It’s just about getting the right suppliers on board, and progressing, from just a framework, to something that banks can actually sell as a credit product. And the flexibility that is envisaged from a credit line on UPI product, along with the distribution that UPI already has (PhonePe cross 700M+ lifetime registered users on UPI), will enable quick discovery and ease of us.

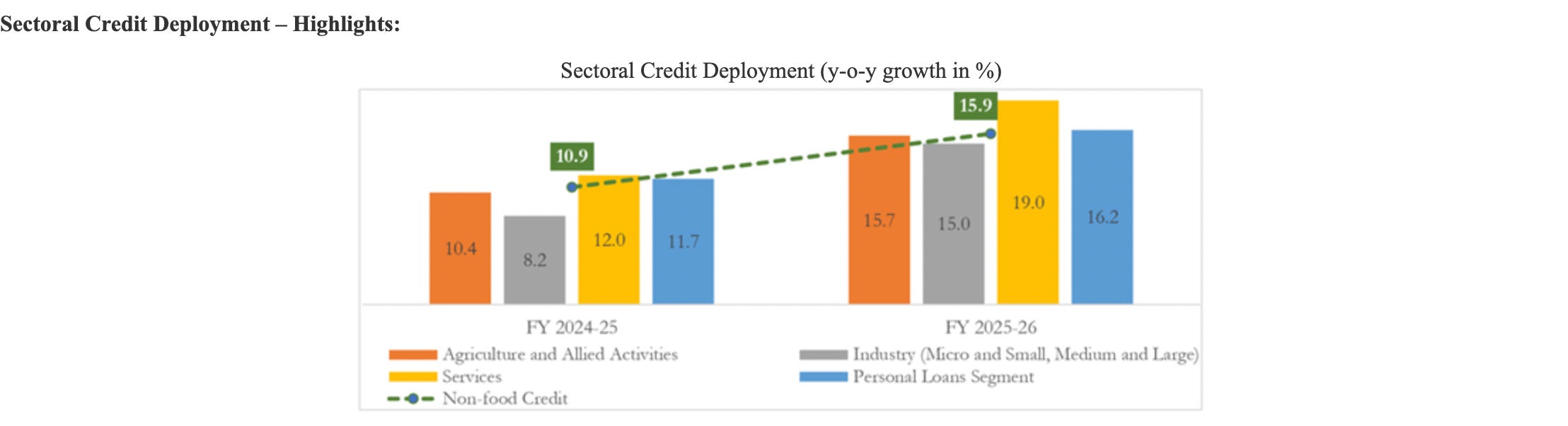

Below: A screenshot from the Ministry of Finance press release, highlight that the year on year credit deployment has grown from 10.9% in FY 24-25, to 15.9% in FY25 - 26.

Some movements in the ecosystem make me think that this unlock is expected soon

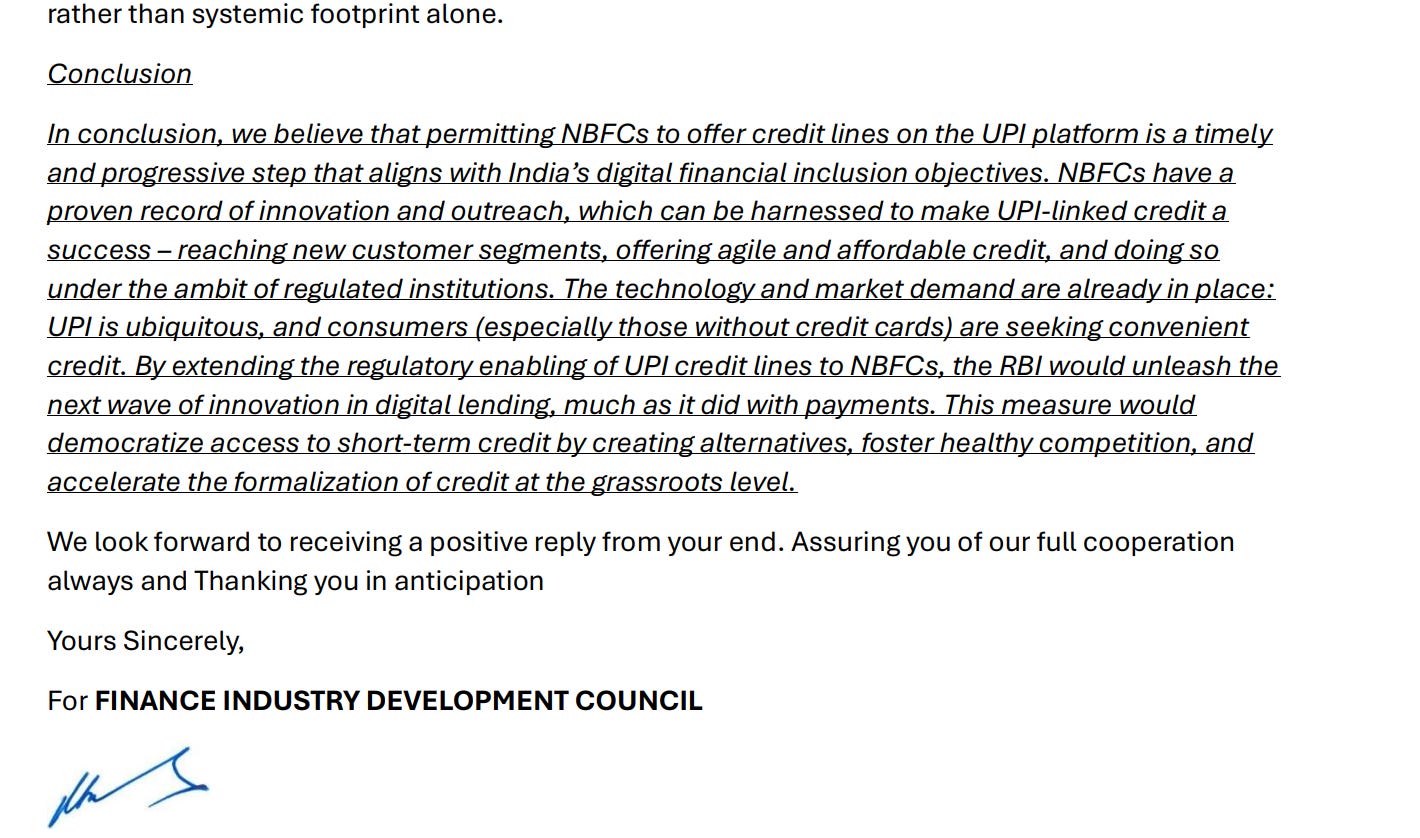

NBFCs also seem to be seeing Credit Lines on UPI as something that will help them grow, especially for newer NBFCs. This letter from the FIDC (Finance Industry Development Council) shows that NBFCs are now clearly lobbying for this unlock to happen, to unleash the next wave in digital lending. A screenshot of the linked letter below.

Lots of NBFCs have a scaled up UPI App, or are in the process of getting one: ABFL, Bajaj, Moneytap, Moneyview, Kreditbee, Hero Fincorp, Stashfin, Jumpp, are either established NBFCs, or new NBFCs, and all are in the process or have a scaled UPI App. While the reverse is also true, that is not surprising, we have established that you cannot operate as a domestic payments player in India without getting into cross border or lending. But the fact that there are a lot of scaled up NBFCs that are going for a UPI App is interesting to me.

These same NBFCs seem to be giving up their PPI licenses. Example: Piramal gave up its PPI license voluntarily in November 2025, PhonePe’s PPI license is expiring in August 2026, and Mobikwik in September 2026 is expiring. Now, if you go through the list of who holds a PPI license, and what is expiring when here, its possible that it’s also the timing - lot of entities (including Ola, Livquik have PPI licenses expiring in 2026, and the real indicator will be if they apply to renew or not. But Piramal giving it up makes me think that it also speaks to the redundancy of the PPI, especially in this flow.

Note: FIDC was granted SRO status by RBI in 2025, as the overseeing body for NBFCs. Some examples of SRO’s in India are AMFI, IRDAI etc.

I was recently doing my regular review of where fintech apps are, what is the license status, and who sits where, and it looks like NBFC + TPAP is the new play, vs the earlier NBFC + PPI + consumer app.

To read the deep dive, you can check out the below link. One theme that has consistently come up in the last 7 editions of this theme that I have covered over the last two years is NBFCs trying to leverage distribution using consumer apps.

![[#88] Do all roads in fintech lead to license aggregation (Part 8): 2 years later, if you're an Indian fintech, you need to be full stack, lend, or go xborder to make money](https://substackcdn.com/image/fetch/$s_!viWB!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F41b90acd-b74b-4721-8bb0-bbbf74e5b339_1790x1012.png)

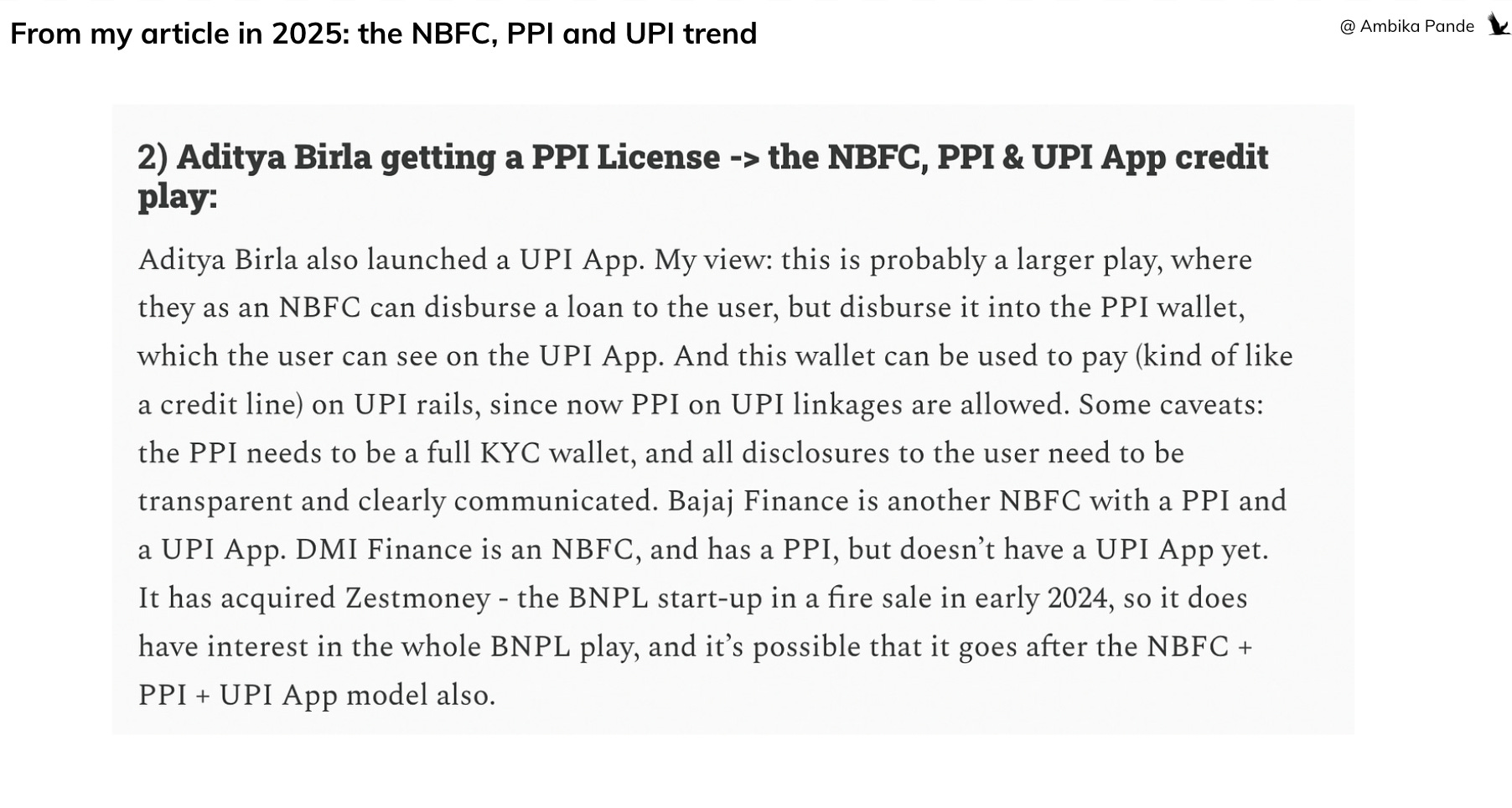

Now, before this Credit Lines on UPI thing started heating up, NBFCs seemed to be doing this via another structure, the PPI on UPI way.

The challenge for NBFCs was straightforward: they couldn’t get customer accounts linked to UPI. Today, when you open any UPI app and go to link an account, you can only link bank accounts. Your UPI ID, say, ambikapande@okhdfc is tied to your bank. NBFCs don’t issue bank accounts, so they were locked out of the rails entirely.

They found a workaround through PPIs, prepaid instruments like wallets and cards. In 2021, RBI mandated interoperability for full KYC PPIs, which meant wallets could be linked to UPI, but initially only through the PPI issuer’s own app. Then in April 2024, RBI went further: it allowed full KYC PPIs to be linked to UPI via third-party apps as well. So a wallet issued by one entity could now show up inside PhonePe or Google Pay, linkable to UPI rails, usable with a UPI PIN. This opened a door for NBFCs. My hypothesis was that they would go after both PPI and UPI app licenses to create a quasi credit line experience: disburse credit into a PPI wallet, link that wallet to their UPI app, and surface it as a payment method - a faux credit line on UPI, built on existing rails. I covered this in Part 4 of my series on “Do all roads in fintech lead to license aggregation.” which you can check out below:

This strategy seemed to be in the right directionally because as of April 2026, 9 out of 59 fintechs / financial institutions I profiled had these three licenses in some combination.

In April 2026, I took a look at 59 fintechs. Out of them, 9 had a NBFC, PPI and UPI license. And 5 had a NBFC and a UPI license.

This was interesting to me because it suggested two things.

Clearly somewhere my hypothesis was playing out, because NBFCs wanted to ensure that they’re able to give credit in a more flexible manner. Since UPI Apps are the best way to do consumer distribution, and NBFCs are not allowed to link accounts to UPI rails, with the opening of PPI on UPI, it enabled them to act as credit accounts.

Now, while the Credit Line on UPI announcement happened in 2023 - when during the Global Fintech Fest (Mumbai), NPCI announced pre-approved credit lines extended by banks, that could be linked to the UPI network, they announced this only for banks, not NBFCs. So NBFCs somewhere needed the PPI so that it could act as a ‘store of funds’ that could be linked on UPI rails.

But the fact that the number of NBFCs that have a NBFC and just a UPI App, combined with the fact that Piramal was surrendering its license was interesting, because it suggested that NBFCs had their supply of credit and distribution figured out, but the missing piece of connecting credit supply to UPI rails, which originally was PPI, seemed to be being potentially solved by someone else

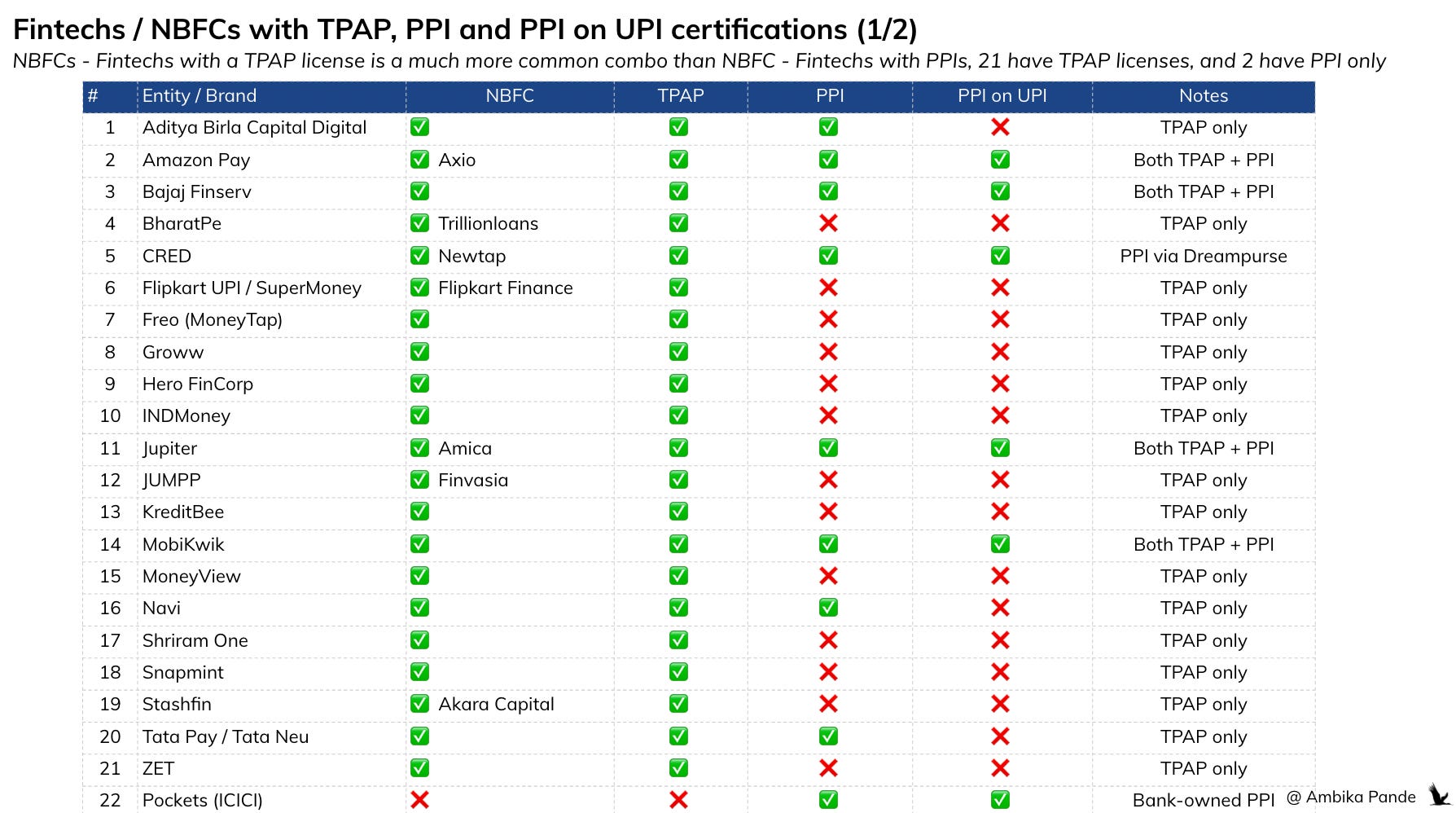

So I decided to pull this thread more. I pulled the list of TPAPs that are certified by NPCI today (total of 47), and mapped out how many of them have NBFCs, PPIs, and what category do they fall in. Example: Are they NBFC first, or UPI app first - since one suggests a credit distribution story which ties more into the Credit on UPI story, but UPI Apps to NBFCs is the same old monetization story.

Out of the total of 47 3rd party UPI Apps / TPAPs certified by NPCI today, 21 of them have some combination which is UPI + NBFC. Listing them down below:

Aditya Birla Capital. NBFC since 2007. Got its UPI App certification in April 2024. Got a PPI license in February 2025.

Amazon Pay: Got a PPI in 2017. Became a TPAP in 2019. Acquired Axio in 2025, but Axio (aka CapFloat) has been a NBFC since 1993.

Bajaj Finance: NBFC since 1987. TPAP since March 2021. PPI since May 2021.

CRED: TPAP in April 2019. NBFC (Acquired a stake in Newtap in 2022, but Newtap has been around since 1995). Cred also acquired Dreampurse in 2021, which got a PPI in 2024.

Jupiter: Got a NBFC (Amica Finance) in 2019. Got a TPAP license in 2021.Got a PPI in 2024.

MobiKwik: Got a TPAP license in 2018. Got a PPI license in 2013 (which is expiring in 2026). And RBI approved Mobikwik’s NBFC license in April 2026.

Navi: NBFC in 2012. PPI in 2015. TPAP in 2023.

Tata Pay: NBFC in 1991. TPAP license in 2022 under Tata Neu. PPI in 2024

Note: PhonePe seems to be getting into this space as well. It got a TPAP license in 2016. PPI license in 2014 but expiration in 2026. It seems to be applying for a NBFC (applied again in 2025 according to reports, and its DRHP)

13 have a combination that includes NBFC and UPI (but no PPI).

BharatPe: It got its NBFC - Trillionloans in 2018. Went live with consumer UPI payments in August 2024.

Groww: NBFC - Groww Creditserv in 2021. TPAP license in October 2022.

Freo (MoneyTap). Got its NBFC license in 2019. TPAP license in 2024.

Hero Fincorp: NBFC incorporated in 1991. TPAP license in December 2025.

INDMoney: TPAP license in October 2024. NBFC incorporated in 2024

JUMPP: Its parent company Finvasia has a NBFC since 2009. TPAP License in December 2025. Currently in CUG testing.

KreditBee: NBFC - Krazybee started operations in 2016. TPAP license in 2025.

Moneyview: NBFC in 2017. TPAP license in October 2024.

Super.Money & Flipkart UPI: Got a TPAP license in 2024. It’s parent company Flipkart got its NBFC incorporated in 2021, but the official license was granted in 2025.

Shriram One: NBFC since 1990. TPAP license in September 2023.

Snapmint: NBFC incorporated in 2019. Got a TPAP license in March 2026.

Stashfin: Its NBFC by its parent company is Akara Capital Advisors Private Limited, which was incorporated in 2016. It got its TPAP license in February 2026 (through Unity SFB, which is operated under the BharatPe group) which is currently in CUG testing.

ZET: Got a NBFC license in September 2025. Got its TPAP license in December 2025.

Other call outs:

Jio: NBFC in 2000. Jio Payments Bank set up in 2016 (so not a 3rd party App, can directly participate in UPI). Got a PPI in 2018.

Slice: NBFC - Quadrillion Finance in 2018. Enabled UPI via its app (TPAP license in 2022). Had a PPI but got cancelled in 2024 when it merged with NE SFB. And now, since it operates as Slice SFB, isn’t a 3rd party TPAP anymore, but participates in UPI by virtue of it being a bank

This is a pretty big list. 21 out of the 47 3rd party apps listed on NPCI’s website have a NBFC and UPI App combination. That is 44%! And out of them, a fair number are NBFCs first: Aditya Birla, Bajaj, Navi, Tata, Moneytap, Hero Fincorp, JUMPP, Kreditbee, Moneyview, Shriram One, Snapmint, Stashfin, and ZET!

13 of them, even if Stashfin, JUMPP and ZET are new, started out as tech enabled NBFCs, with the TPAP license being a pure distribution play, and potentially a piece of the Credit Lines on UPI puzzle.

It looks like NBFCs are betting on the Credit Lines on UPI being opened up to them over PPI as a stored value

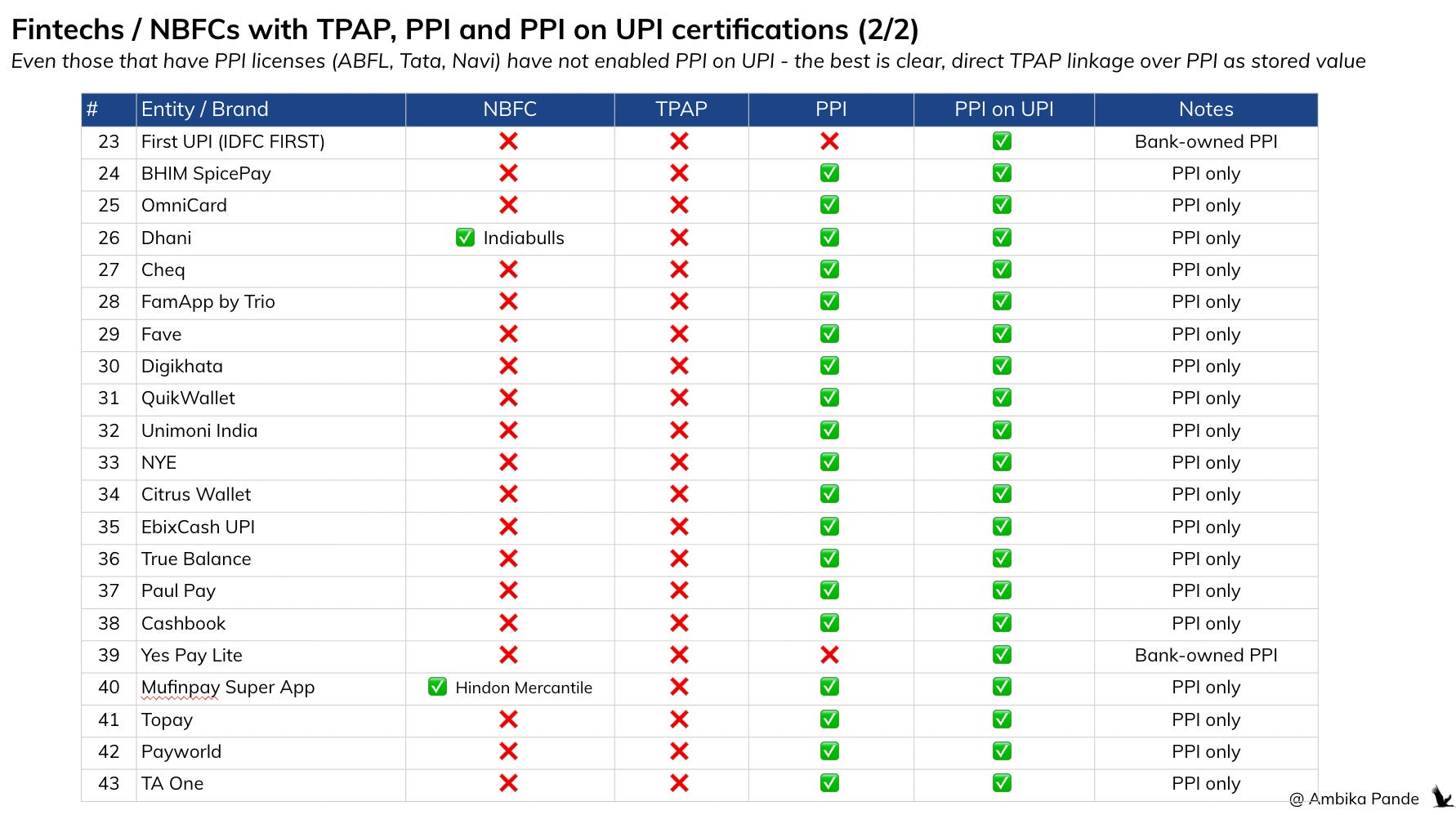

Here’s a list of the PPI on UPI Apps. Bajaj, Jupiter Money and Mobikwik are here, where they have both PPI on UPI and TPAPs / UPI, but the volumes are coming purely from their TPAPs, not the PPI on UPI flows. Take a look:

Points to note here:

The entities I have mapped are those who are fintech / NBFCs with TPAP licenses, and then see how many of them have PPI licenses, and PPI on UPI enabled.

And then those entities that have PPI on UPI enabled, and how many of them are NBFCs.

What I was trying to do is see where the ecosystem seems to be going. And very clearly, it is the NBFC + TPAP way. Out of the PPI on UPI enabled entities, 8 are also NBFCs. But out of them only Dhani and Mufin are PPI + NBFC but no TPAP. All the rest - Bajaj, CRED (Drempurse), Mobikwik, Amazon also have a TPAP, and their volumes are coming via TPAP, not their PPI on UPI wallet. Note: PayU also sits here with a NBFC and a PPI license, but they don’t have a consumer play.

The top 21 (until ZET in the previous slide) is the list of TPAPs that also have some NBFC license in an affiliated entity. 6 of them have PPIs. But what is interesting is, out of them, Aditya Birla, Navi and Tata Pay, despite having a PPI, have not enabled their PPI on UPI. And these are big NBFCs. In fact, they are NBFCs first, before being TPAPs. So this is interesting, because it points to them betting on direct UPI rails, over PPI on UPI rails for lending.

Out of the list, only 2 NBFCs have bet on the PPI way over direct UPI linkage. Dhani (Indiabulls) and MufinPay (Hindon Mercantile). I think its a fair bet to say that NBFCs clearly seem to be betting on the Credit on UPI piece opening up for loan distribution, and PPI’s may not be very relevant anymore here.

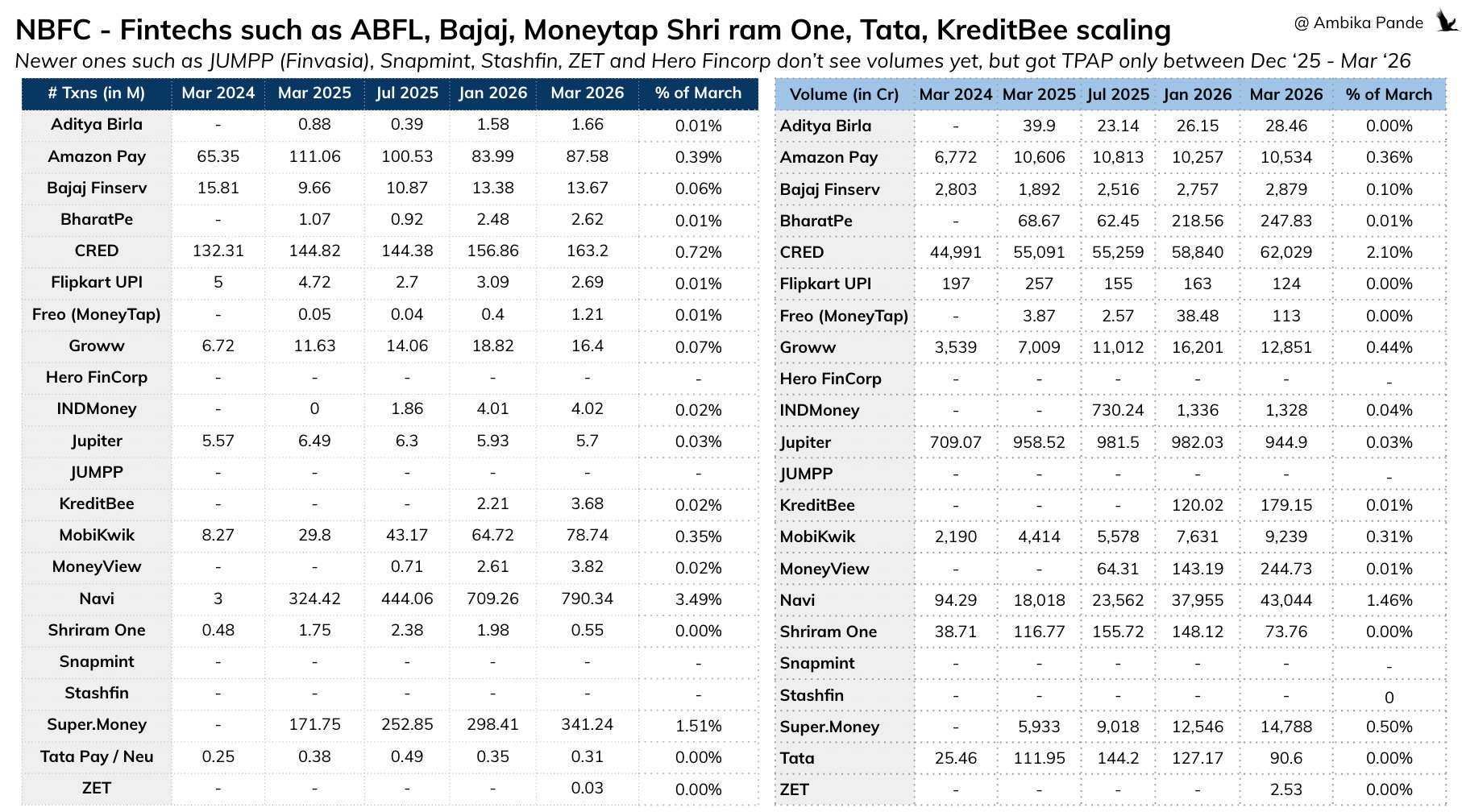

These NBFCs also seem to be funnelling serious volumes from their UPI Apps: for distribution yes, but they also general transaction data that they can use to underwrite better, and also, through UPI Autopay, set up repayment

While UPI is a top 3 player game today, the NBFC - Fintechs seem to be channeling decent volumes. Some of the top contenders (NBFC first)

Aditya Birla: 1.6M txns, and 28.46 Cr volume in March 2026 (0.01%)

Bajaj Finserv: 13.67M txns, and 2879 Cr volume in March 2026 (0.1%)

Freo (Moneytap): 1.2M txns, and 113 Cr in March 2026

Kreditbee: 3.68M txns, and 179 Cr in March 2026.

Moneyview: 3.82M txns, and 244 Cr in March 2026

Shriram One: 0.55M txns and 73 Cr in March 2026

The above are all NBFC first. And they are all TPAPs. Not PPI on UPI. Even for players such as Bajaj Finserv, Jupiter etc, although they do have their PPI license, and PPI on UPI enabled, all the volumes are being channeled via their TPAP, not their PPI wallets.

And, other NBFC first fintechs, where we will probably start seeing volumes soon are: Hero Fincorp, JUMPP, Snapmint. Stashfin, and ZET, which all got their TPAP certifications between December 2025 and March 2026. So it is fairly recent. And this trend seems to suggest 3 things:

TPAPs with India focus are going to go get NBFC licenses for monetization

NBFCs want TPAP licenses and own UPI Apps for distribution

The NBFC + UPI trend, vs the NBFC + PPI trend seems to suggest that NBFCs are putting their eggs in the Credit on UPI basket.

But RBI is also actively cleaning house - the days where you could buy a shell and slap a brand on it for ~ INR 2 - 5 Cr are gone, so it isn’t that easy to get a NBFC now

Before we get into this, important to understand why this is the case. So today, NBFCs have different scales basis which they were audited. (a little like what I’ve talked about before, how Singapore / UK have different levels of compliance and audit depending on the scale of the fintech). You can check out the details here:

Base layer: If the NBFC has < INR 1000 Cr in assets. This is the biggest bucket, and out of the total 9075 registered NBFCs on the RBI website, 8389 NBFCs sit here.

Middle layer (559 sit here): If the NBFC has > 1000 Cr in assets , then it sits here. Most fintech NBFCs sit here actually → Krazybee (Kreditbee), Navi, Groww Credit, Kissht (Si Creva), etc.

Upper Layer (14 sit here): There is no fixed asset class here, it is safe to assume that it has > 1000 Cr. But apart from that, the top 10 NBFCs in terms of their asset size, will automatically reside in this layer. There are 14 here today: Aditya Birla Capital Limited, Bajaj Finance, Bajaj Housing, Cholamandalam Investment and Finance Company, HDB, L&T Finance, LIC Housing Finance, Mahindra & Mahindra, Muthoot, Piramal PNB Housing, Sammaan Capital, Shriram Finance, Tata Capital.

Top Layer: According to the link above, - “The Top Layer will ideally remain empty. This layer can get populated if the Reserve Bank is of the opinion that there is a substantial increase in the potential systemic risk from specific NBFCs in the Upper Layer. Such NBFCs shall move to the Top Layer from the Upper Layer.” I didn’t really get the point of having a Top Layer that is designed to be empty, but from what I understood, it’s kept as a category that NBFCs can temporarily exist in only if there is enhanced risk, which is what will call for enhanced scrutiny. Kept to deter the market.

And out of these 9075 NBFCs, I’d estimate that only about ~1500 are actually active.

Few reasons for this:

Out of these 9075 NBFCs, close to 4000 are still not registered on FIU-INDs portal, making them non compliant with Anti Money Laundering laws

There was a NBFC boom in the 1990s. During the 1980s and 1990s, NBFCs experienced a significant increase in investor interest which resulted in a rapid expansion of the industry, with the number of NBFCs quadrupling from approximately 7,000 in 1981 to around 30,000 in 1992. Out of the 9075 NBFCs registered today, ~ 7300 were incorporated before 2000. At this point, the barrier to register the NBFC was really low. Its fair to assume that a big portion of them are inactive.

Now, since then, from 1997 to 2026, RBI has gradually increased to requirements to get a NBFC license. A case in point is Net Owned Funds (NOF)

Pre-1997: There was no requirement

1997 onwards: INR 25 Lac as Net Owned Funds (Equity Capital + free cash)

1999 onwards: New NBFCs had to have NOF of INR 2 Cr

2015–17; Even existing NBFCs had to have INR 2 Cr as NOF, not just new ones applying

2022 onwards: Move toward INR 10 crore for core lending NBFCs

This is a way for RBI to clean up the NBFC landscape, its an audit overhead, and there is shell company risk

The recent cancellations (150 in May 2026, 35 in Dec 2025) + the voluntary surrender window until Sep 2026 suggest that RBI is actively pushing cleanup. This is for two main reasons:

Supervisory burden: RBI has to track 9,000+ registered entities, collect returns, monitor compliance. Most don’t file anything.

Shell company risk: Inactive NBFCs with valid CoR would get sold/misused for money laundering, loan sharking, or circular transactions. A valid RBI license gives credibility. By increasing the NOF requirement, RBI is raising the barrier to entry.

RBI also introduced the NBFC Registration Amendment 2026, where if you don’t meet certain criteria, you don’t even need to be an NBFC, effective from July 1 2026.

RBI created a new category called “Unregistered Type I NBFC” which are entities that no longer need an RBI Certificate of Registration. The eligibility criteria for this is (must meet ALL):

Asset size below INR 1,000 crore

No customer interface: Doesn’t deal with public/retail borrowers

No public funds: Doesn’t raise money from deposits, NCDs, bank borrowings, or any indirect public sources

Naturally, if you have smaller asset size, are not customer facing, and don’t take public funds, then you are at a lower risk. What RBI is saying here is that if you’re a small holding or investment company that doesn’t lend to anyone and doesn’t take money from anyone, then you don’t need to be an NBFC anymore. Think family investment vehicles, corporate treasury arms, or inter group lending entities. NBFCs that fit this criteria get a one time surrender window

This is RBI’s elegant solution to the 8,000-shell problem. Instead of cancelling thousands of CoRs one-by-one (150 here, 35 there), they’re saying: “If you’re not actually doing NBFC business, you’re no longer an NBFC. Exit voluntarily.” It shrinks the register without needing enforcement action for each entity.

So, coming back to the NBFC + Credit on UPI story, it means that while the strategy seems to be clear: TPAPs go after NBFCs to boost margins, and leverage the Credit on UPI story, it wont be that easy

The strategy looks obvious on paper: TPAPs (PhonePe, Google Pay, CRED, etc.) have the distribution, hundreds of millions of users transacting daily. NBFCs have the license to lend. Marry the two via Credit on UPI, and you unlock massive monetization. That is the winning play. But.

NBFCs are coming for distribution. Every serious NBFC, your Bajaj Finservs, Shrirams, is building or has built a UPI app. Navi went from 3 million UPI transactions a month to 790 million in two years. They’re not doing this for payments revenue. They’re building a customer acquisition engine on UPI rails, so they can lend directly without sharing economics with a TPAP. Why pay a platform for leads when you can own the customer relationship? And Credit on UPI is a lending play, not a UPI play. You need to know how to lend, how to underwrite, and how to manage NPAs.

And TPAPs going after NBFCs is harder than it looks. RBI has raised the minimum Net Owned Fund to INR 10 crore (headed to INR 25 crore). Shell NBFCs are being systematically wiped out. Getting a fresh NBFC license now means real capital, real compliance, and real intent.

I genuinely believe that Credit on UPI has the potential to be massive, but this is subject to the unlocks I talked about at the start of the article. And the key is the NBFC piece. But even if my hypothesis is correct, and the ecosystem does seem to be moving towards this being opened up to NBFCs, the winners won’t be the apps with the most users, they’ll be the lenders who figured out distribution first.