[#88] Do all roads in fintech lead to license aggregation (Part 8): 2 years later, if you're an Indian fintech, you need to be full stack, lend, or go xborder to make money

Part 8 of the fintech license aggregation series. Two years in, who's stacking, who's surrendering, and why you need to be either full stack, lending, or cross border to make money in India

Hi folks, and welcome back to the latest edition of the theme: “Do all roads in fintech lead to license aggregation?”

The first edition (Part 1) was written in May 2024! Looking back from May 2026, it has been two years since I started tracking this space. And, a lot has changed in this Indian fintech landscape. From the payment aggregator licenses officially being formalized by RBI in 2024, to the frenzy for entities (including non fintechs, such as Zomato) for getting licenses, and then returning them. To payments bank licenses being banned, and the cancelled. Then in 2025, the licenses being further birfurcated into PA-Online, PA-Offline (PA-P). And then the consolidation story playing out, across consumer payments, B2B payments, lending, wealth, and cross border. To fintechs becoming full stack, and going deep into the infra play (building own switches). And then, some major fintech IPO’s happening: Mobikwik in 2024, Groww and Pine Labs in 2025, Kissht in May 2026, and Razorpay and PhonePe coming soon, this is a sign of the maturing Indian fintech system. And a lot of recent moves are indicative of how strategies are also evolving, especially in the face of the limited monetization on UPI story.

To read some past pieces on this theme, which cover the above evolving landscape, do check out the links below:

Part 2: [#37] Having multiple licenses as an Indian fintech seems to be key

Part 3: [#54] There are very few “1 license players anymore” - PA seems to be the most popular

Part 4: [#63] It’s not just about license aggregation, it’s about stack specialization

Part 5: [#69] Payments is just the first step in going full stack

Part 6: [#74] Multi-license fintechs are driving profits and IPOs

Firstly, the news that have made headlines over the last few weeks

Just a summary of some headlines around this space over the last few weeks and months, and where I feel this suggests that we are heading.

1️⃣ Groww gave back its Payment Aggregator license in April 2026, which could start a trend of more mature fintechs in India surrendering licenses that don’t align with their core strategy any more.

I’m not surprised. I assume they had taken it for optionality, and now, as they scale into a fully blown wealth tech, especially after their blockbuster IPO in November ‘25, a very clear strategic decision has been taken NOT to get into merchant payments. This is also interesting to me, because usually in the case of big orgs, the build vs buy question, and in this case, it would be building vs buying payment services, usually tilts in the favour of ‘build.’ So this could be indicative of two things. One: what I mentioned above - Groww doesn’t need optionality, the path is clear. And two: the cost of building, apart from just the compliance overhead may not be worth it, in a market where UPI is driving prices to the bottom.

2️⃣ RBI finally cancelled Paytm’s Payment Bank license, and it looks like Fi is shutting down - no respite for the neobank story in India

RBI cancelled Paytm’s Payment Bank license due to “persistent non compliance and supervisory concerns, including KYC violations and issues with technology infrastructure.” This has been a long time coming. Paytm’s payments bank was first barred from onboarding new customers in March 11, 2022, and then banned further deposits or top-ups on February 29, 2024. I was rooting for them, honestly. As the first big fintech in India to capture public imagination, and take those steps to becoming a ‘full stack’ fintech, with the coveted payments bank license, I was hoping that this could actually be a comeback story. But, the message is clear from RBI - compliance over everything. That is one angle.

The other news here is that the neobank Fi seems to be on its way to shutting down. A linkedin post from one of its founders, also indicated that he was stepping away. Fi had reached a peak valuation of $524M at its peak in October ‘22, but RBI was never bullish on neobanks, and the hope that players like Jupiter and Fi, even though they started out as a wrapper around existing banking services, could eventually get a banking license didn’t seem to work out. That is pretty sad, and does lead me to question how RBI is thinking about the fintech evolution in India, especially when globally there has been proof of how neobanks actually drive financial inclusion. Nubank, Monzo, Bunq, and of course Revolut being some examples. And cases like Paytm don’t help much. However, what does give me hope, is that even if there is no story for neobanks in India, atleast we have what I call a “new” type of bank: with a start-up mindset to customer experience and support. That is Slice. The fact that it has become a SFB (Small Finance Bank) is promising, but only time will tell if the prediction for better customer experience holds true. I expect it to go after a Universal Banking License in ~5 years.

To read more about my thesis on neobanks, and why I believe India needs them, you can check out the link below:

[#64] Innovation at the edges, stagnation at the core: Why India needs neobanks for true financial inclusion

![[#64] Innovation at the edges, stagnation at the core: Why India needs neobanks for true financial inclusion](https://substackcdn.com/image/fetch/$s_!mm8d!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F59900c72-7141-4304-bc8a-ce8c3fd63865_1688x944.png)

A few months ago I had talked about neobanks, and why India needs some structure that allows neobanks to function in India. You can check out the article below:

3️⃣ Mobikwik joins fintechs (such as PayU) to get a NBFC license in May 2025 to drive lending ambitions, and sources suggest PhonePe has applied again for one, bringing the number of fintechs with NBFCs to 9+. The lending story for India focused fintechs is alive and kicking

Mobikwik IPO’ed in December 2024, where the big news was that its valuation for IPO dropped close to ~70% to ~$194M, from its peak valuation of $924M in 2021. It is, in its own right a full stack fintech. It has a UPI App, which in March ‘26, processed ~78M monthly transactions, and a total value of ~INR 9239 Cr, which brings it to lucky number 13 in the UPI App ranking list in terms of # of txns. It also has a PA-O (online) license, which is got the final approval for in April 2025, its PA-P (offline) license is under process, a BBPOU (Bharat Bill Pay, can directly connect to XX to enable bill payments), a PPI license holder, and now NBFC.

PhonePe seems to have applied again for a NBFC. No verified source, but I found the link to a tweet that says that it does (you can see it here). This is the link to the screenshot shared in the tweet, which suggests that PhonePe applied in November 2025 for the third time.

There is a trend here. It is interesting to me that both Mobikwik and PhonePe have a PA-O, and a PA-P. They glaringly do not have a PA-CB, either approved, or at any stage of approval. This seems to very clearly signify India ambitions at this point, and could also point that you if you want to make money, and keep India as the primary market, lending seems to be the only way out. More on this below:

4️⃣ The consolidation trend continues: Billdesk bought the India business of Worldline for offline payments, and Pine Labs bought Shopflo to beef up Pine Online, and I expect more to happen for the online, offline and consumer app play

Billdesk, which till now had an online only business, bought the India business of Worldline, for its offline payments business.

Pine Labs bought Shopflo to scale up Pine Online. Shopflo is a payments infrastructure player, but focused more on the ecommerce and D2C side of things. The best way to describe them would be a sort of checkout enabler, where they optimize experience, checkout rates, pre-fill addresses, and reduce RTOs for merchants. This makes sense. Pine Online aka Plural was launched in 2021, but it really hasn’t scaled its online presence meaningfully, and Shopflo reportedly has ~1000 merchants on its network, which is probably why the acquisition happen, it will boost Pine Online’s merchant base. This is in additional to the acquisitions that Pine has already done.

👇 Just to recap:

Razorpay - online first. Then they bought Ezetap (now Razorpay POS) in 2021, and Pop (UPI App) in 2025 for its offline and consumer app presence. 2 acquisitions for license aggregation. However, reportedly Razorpay is scaling back its offline business now

Pine Labs: offline first. Then bought Fave (a consumer loyalty platform in 2021, now operating as a UPI App in India. Transactions for this app first appeared in December 2025, and in March 2026, it closed about 60k transactions, and ~INR 10 Cr in volume. They also bought Setu in 2022, I am assuming for its AA license (Setu got the AA license in July 2022, the Pine acquisition completed in June 2022). Setu also has APIs that enable BBPS functionality both for consumer apps who want to embed bill payments, and for billers who want to onboard on BBPS. Pine also bought Mosambee, which is POS devices, for offline expansion in 2022. So, 2 acquisitions for functionality, and 2 (Shopflo and Mosambee) to increase base (both online and offline)

PayU bought Mindgate which is a UPI infra player (and integrated with 2 big banks, SBI and HDFC for UPI switch), in 2025, immediately strengthening their online play.

A non relevant observation I had, while I was trawling the internet to find updates I may have missed is about CCAvenue.

CCAvenue changed its registered name to AvenuesAI, from Infibeam. Odd. I assume that this is to signify increasing focus on ‘AI.’ I found this accidentally since at least on RBI websites now, Ctrl+F would just NOT show up for Infibeam. So, this could be the newest casualty of the AI positioning phase.

That’s it with the big updates. Now, for the sake of consistency, I thought to go back to some past predictions I made, and see how they panned out.

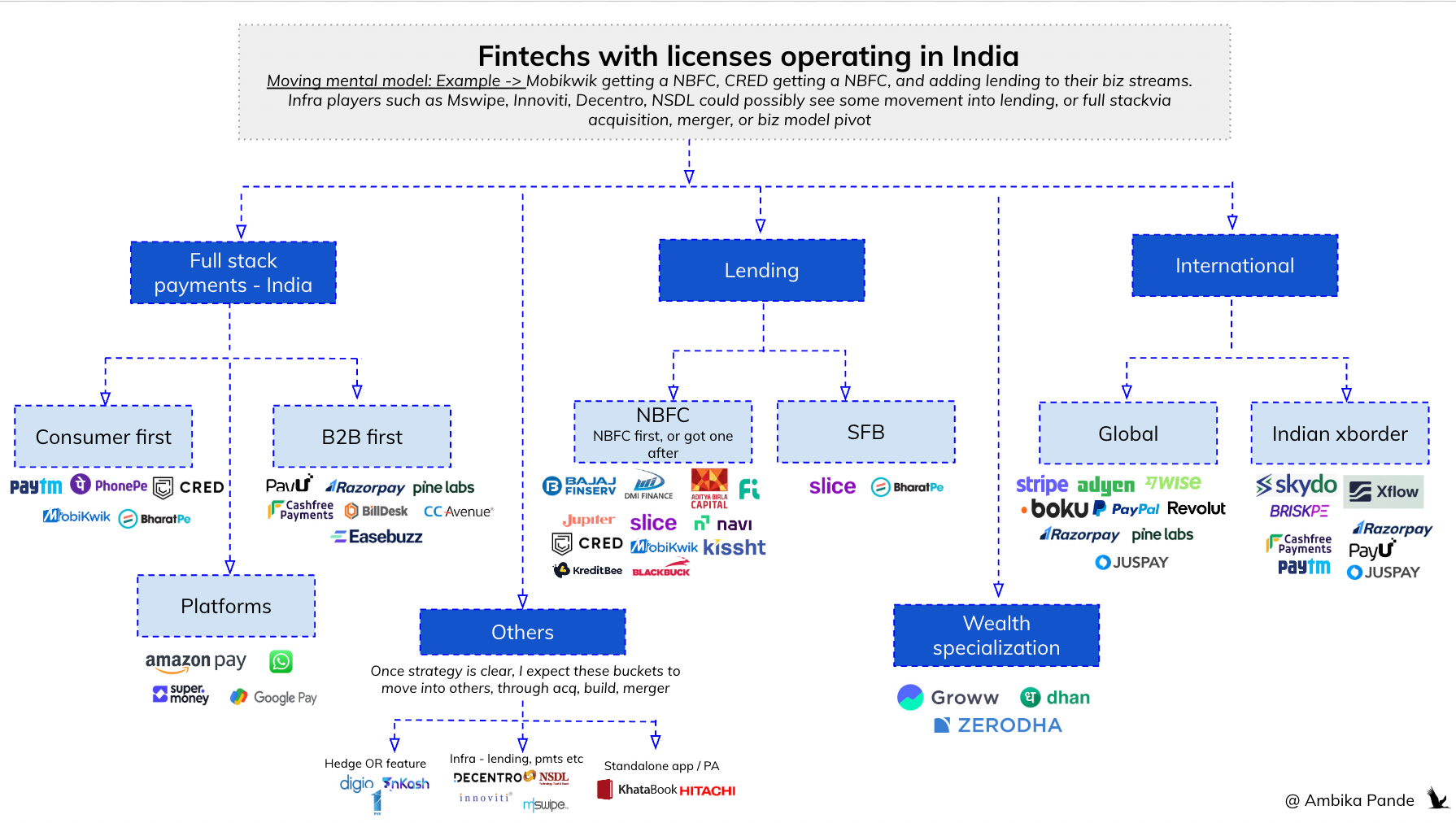

If you folks remember, I had divided the licensing game into 4 broad trends. The regulatory hedge, the full stack play, the India focused strategy, and Xborder. In the interest of Indian fintechs, what I’ve also done is expanded this mapping, to see where players sit, and where possible movements could happen.

Few points to note here are that

This is a moving model. And, there is still a lot of consolidation that I feel is pending, and especially with the state of monetization in India. I expect to see more online + offline acquisitions (like Billdesk - Wordline), and a lot of B2B + B2C plays (like Razorpay - Pop, Pine Labs - Fave, PhonePe, Paytm) etc.

Players can sit in multiple buckets. Example: most full stack PA’s in India, also are going after the xborder (and in some cases, a global play, by setting up entities in USA, Singapore, Malaysia and so on). Second example: Mobikwik - is a full stack fintech, but not a market leader in either B2B or B2C, so it’s been trying to expand streams, by getting into broking in 2025, and now getting a NBFC license in 2026. I expect this to also happen with other fintechs.

The “others” bucket has mostly standalone infra / app players, which are either TSPs for specific use cases (which could be lending - such as standalone LSPs without NBFC licenses, or purely for underwriting / collections / identity, and are NOT part of a fullstack play yet), have gotten a license to give optionality or hedge, or want to provide it as an added feature (like PPI for example). In India, I think it is pretty clear that unless you’re a lender, or a serious xborder player, it is very tough to survive standalone, and hence, I expect movement here, either via acquisition, merger, pivoting, or perhaps even shutting down. An example: Juspay, before it’s international expansion, would actually be classified as a infra player. It’s now scaling internationally, both as a global TSP, and a potentially a xborder money movement player, and turned profitable in 2025.

Note: This analysis only includes fintechs with licenses. It doesn’t include TSPs which don’t have a license (like underwriting, identity, data TSPs that still operate standalone - although its possible that consolidation is in their future). And fraud and risk is a separate category - it is fintech adjacent, but not fintech itself in my opinion

Lets dive in.

👉 The regulatory hedge: may be true for smaller players, and RBI’s 2028 payments vision actually supports this strategy but bigger players who have figured out their strategy will surrender licenses

To be honest, this may still exist for smaller players, but for bigger players where their strategy is clear, and they’re also not in a payment flow, will probably not hold true. This is a maturity signal, where companies realizing they can’t do everything. Some examples, where the strategy is clear:

Groww surrendered PA-O in January 2026 after holding it for 2 years (it got it in 2024). It is doubling down on wealth management, and its lending business, which reportedly has started contributing meaningfully to overall profits. Going forward, Groww is planning to deploy earnings and proceeds from its fundraise via IPO towards this business. (a sign that lending, unlike payments probably makes money)

Stripe returned both PACB-I and PACB-O (retreating from India cross-border) in 2024.

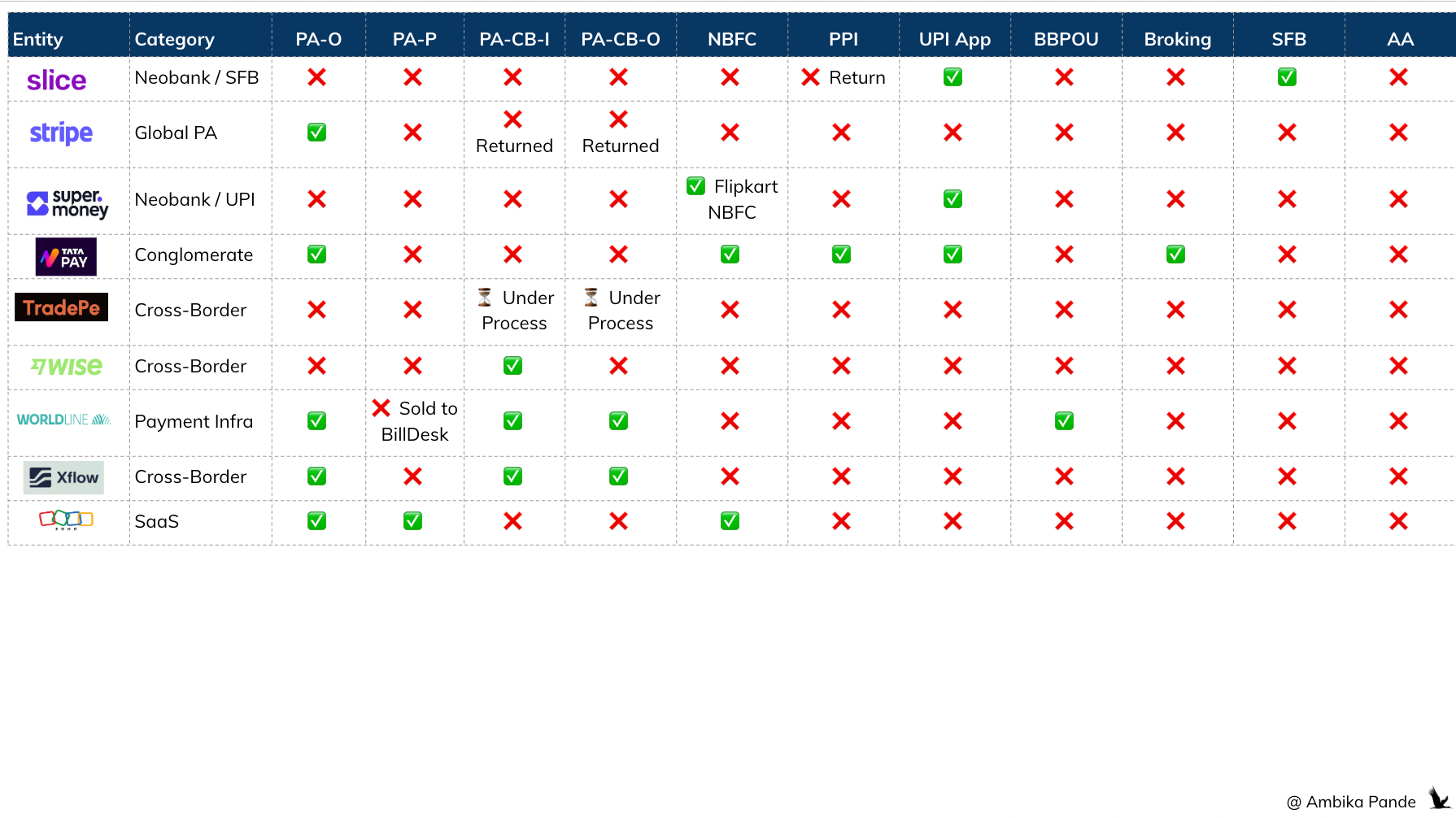

Slice gave back PPI when it merged with North East Small Finance Bank (NESFB) to form Slice Small Finance Bank. If you folks remember, they originally started out as a faux credit card - leveraging bank / NBFC PPIs to hold money in a wallet, and then funding this via short term loans via NBFCs. When this model was shut down by RBI, they pivoted to a LSP model, and now have successfully become a bank.

I expect more of this to happen, but in fully scaled up fintechs. Smaller fintechs may still need that optionality, and this will always be mostly PAs. Some examples of regulatory hedging (in my opinion) are Digio (identity TSP, has a PA), Khatabook (accounting for SMEs, has a PA), Hitachi (payment infra), 1Pay (haven’t heard too much about these guys, but I think they’re a logistics payments company). Another point in favour of the regulatory hedge strategy: RBI’s payment vision 2028 does talk about reducing the regulatory load for newer players to encourage innovation. Now, if that means the creation of a new license altogether, or of a tiered type license depending on volume, size (like Singapore), that is something that remains to be seen.

👉 Full stack play is the only way to survive ( if you are a non lending fintech in India)

For fintechs that started with something that was not lending, they have gone full stack, with most either placing their bets on lending (Mobikwik, PayU, PhonePe reportedly applied for NBFCs), or going hammer and tongs into crossborder (Cashfree, Juspay). Juspay in fact turned profitable in 2025, with a profit of INR 115 Cr, after it started expanding internationally in 2020.

I’ve already talked about this a little bit in the above point about consolidation, so I won’t spend too much time on it. But, seeing the Worldline and Billdesk piece play out, and the Pine Labs and Shopflo, I’m expecting big time online / offline consolidation to happen. Key suspects

Easebuzz and Cashfree are online, raised money in 2025. Easebuzz raised $30M in 2025, and Cashfree raised $53M in 2025

Mswipe and Innoviti are offline first players.

While all 4 have both PA-O, and PA-P licenses, they are very obviously dominant in either online or offline. If we go by the assumption that to make it as a payment player, you need to be full stack, then it is possible that there is consolidation on the horizon. Now if they get acquired by a third larger player wanting to enter, or consolidation happens between these guys, that is yet to be seen

I’d say this is a no brainer.

👉 India first plays in fintech - if you’re not full stack, and not going cross border, then only lending will save you.

There are many Indian players here, but the big question is how to make money? I’d actually call this a substack of the full stack play, without the PA-CB license. So, this could be PA-O, PA-P, and everything else that is India first, so PPI, AA, NBFC all sit here.

✅ Here is where the lending thesis holds across the board. That if you want to make money, and you are an India first player (so you can’t leverage the margins from the cross border business)

MobiKwik, PayU, CRED, Grow, Slice (founded 2016, got a NBFC in 2019), BharatPe (founded 2019, got a NBFC in 2023), sit here. Slice, and BharatPe of course when the SFB way, with Slice SFB, and Unity SFB. The point being: Almost every payments company that added an NBFC did it after establishing payments. They built distribution, scaled their business, and then realized that this is not making money (possibly because of UPI scale and lack of monetization), and then because the focus was on India, decided to go behind lending for monetization. Paytm is a prime example also: built distribution and brand, and then bundled lending into its products to make money.

In fact, out of the profiles sampled (details in the appendix), 8 start-ups have the NBFC, PPI and UPI App : which is AmazonPay, Bajaj, CRED, Jio, Jupiter, Mobikwik, Navi and Tatapay.

And then 5 that have NBFC and UPI App, but not PPI: BharatPe, Fi, Groww, KreditBee and Supermoney. Although, recent news suggests that Fi is winding down, I remember reading a post on linkedin where the founder announced that they’re stepping back, and reports suggest that they are discontinuing their operations also.

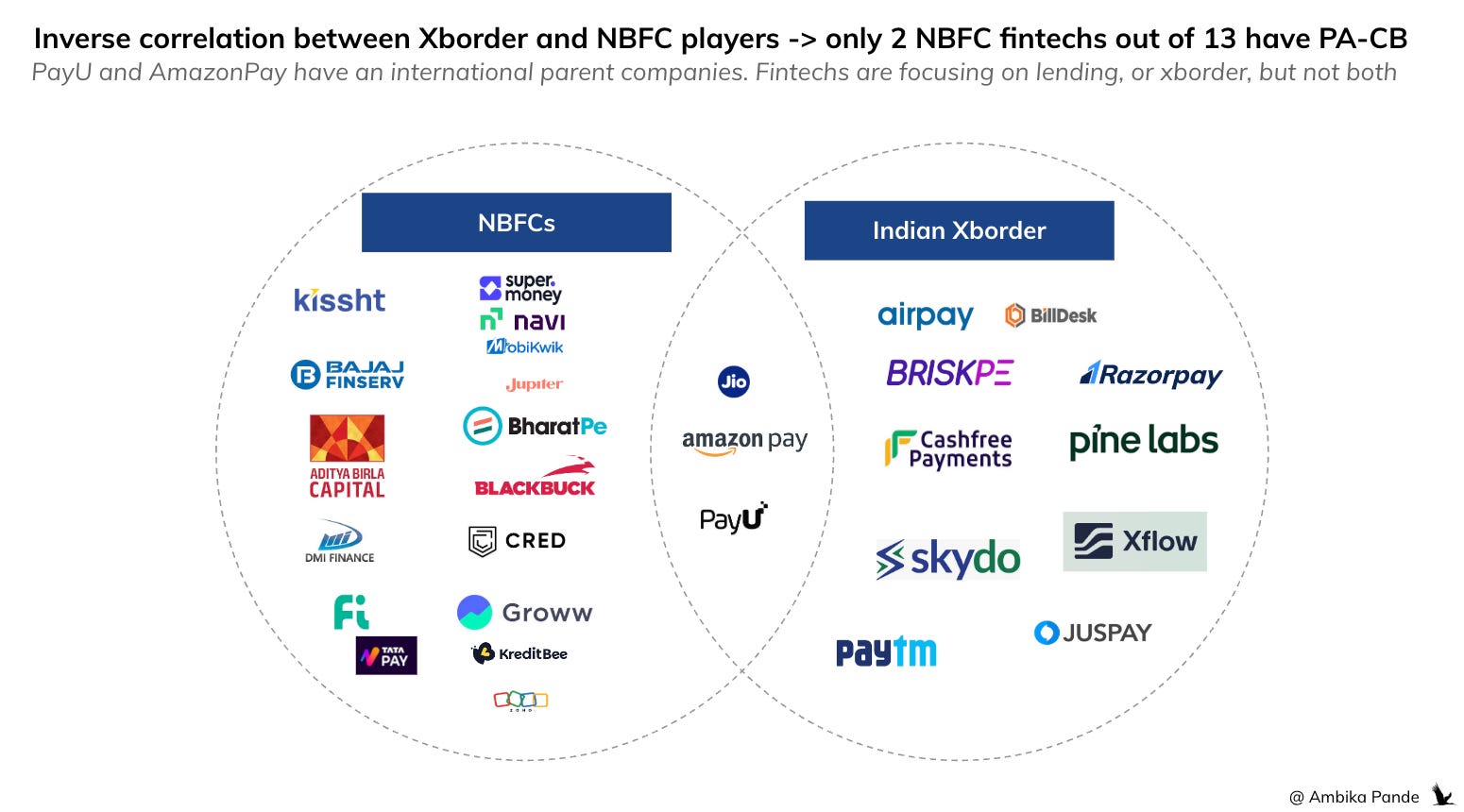

👉 Here’s another interesting point: there seems to be an inverse correlation between fintechs having a NBFC license and PA-CB. Take a look at these stats.

The number of fintechs / financial institutions that have NBFCs: 19. Aditya Birla Capital, Amazon Pay, Bajaj Finance, BharatPe, Blackbuck (Zinka), CRED, DMI Finance, Fi, Groww, Jio, Jupiter, Kissht, KreditBee, MobiKwik, Navi, PayU, Super.money, Tata Pay, and Zoho.

Even if I remove the original NBFCs from here: ABFL, Bajaj, DMI, Kissht, KreditBee, and TataPay, that still leaves 13. Out of the 13 left, only 3 have a PA-CB license (either I or O): AmazonPay, PayU, and Jio. And Jio is a conglomerate, so I’d take it out of this comparison list as well. So, out of 13 fintechs that also went and got NBFCs, only 2 are looking at cross-border.

That seems to strengthen a larger thesis emerging in Indian fintech: companies are largely choosing between becoming India first financial institutions or internationally-oriented payments platforms, but very few are seriously trying to do both. And if you areeaning India first are increasingly converging toward NBFCs. And the overlap between the two groups is surprisingly small. Which suggests that structurally, it seems like fintechs are deciding to pick one or the other, but not both.

👉 In 2025 Paytm announced focus on international markets, and said they expected results in 3 years, so they do have a strong xborder focus, and are looking to capture domestic acquiring in international markets

In FY25, its subsidiary Paytm Cloud Technologies acquired a 25% stake in Brazil-based embedded finance startup Dinie. Paytm also incorporated wholly owned subsidiaries in the UAE, Singapore and Saudi Arabia to distribute its “technology led merchant payments and financial services stack” in these countries. This also seems to explain why, in its

In India, they have merchant distribution, both online and offline. They have lending partners And all said and done, building a lending business is not as easy as just getting a NBFC license. After getting the license, you also need to get debt financing (to along with your equity capital), so you can actually start building your book.

And this explains why Paytm made the point they did during their Q4 FY26 earnings call in May, saying that they (especially after their Payments Bank license being cancelled), that they do not need a NBFC license right now and are focused more on scaling payments and credit distribution. I would argue that this proves my point further. They are a full stack fintech. They have 6 licenses: All the 4 PA licenses, a UPI App, and broking. And they have international focus, which clearly seems to be what they are going after, vs on the books lending.

👉 Xborder requires its own focus and has the TAM and margins to potentially be profitable.

There are 2 emerging trends here

✅ Both PACB I and O (inward - export, and outward - import), for xborder only players

Crossborder has high margin, and the TAM and margins could be enough for standalone players. You have players such as Skydo, Xflow, that sit here, and focus on this only

✅ PACB O - for outward money movement (import flow)

Adyen, Boku, and Amazon Pay sit here (although Amazon Pay also has a lot of India focus, with the NBFC, PPI etc). But in the case of Adyen and Boku, they very clearly are focusing on providing value for their international merchant base, and enabling them to collect money from Indian customers, and not the reverse.

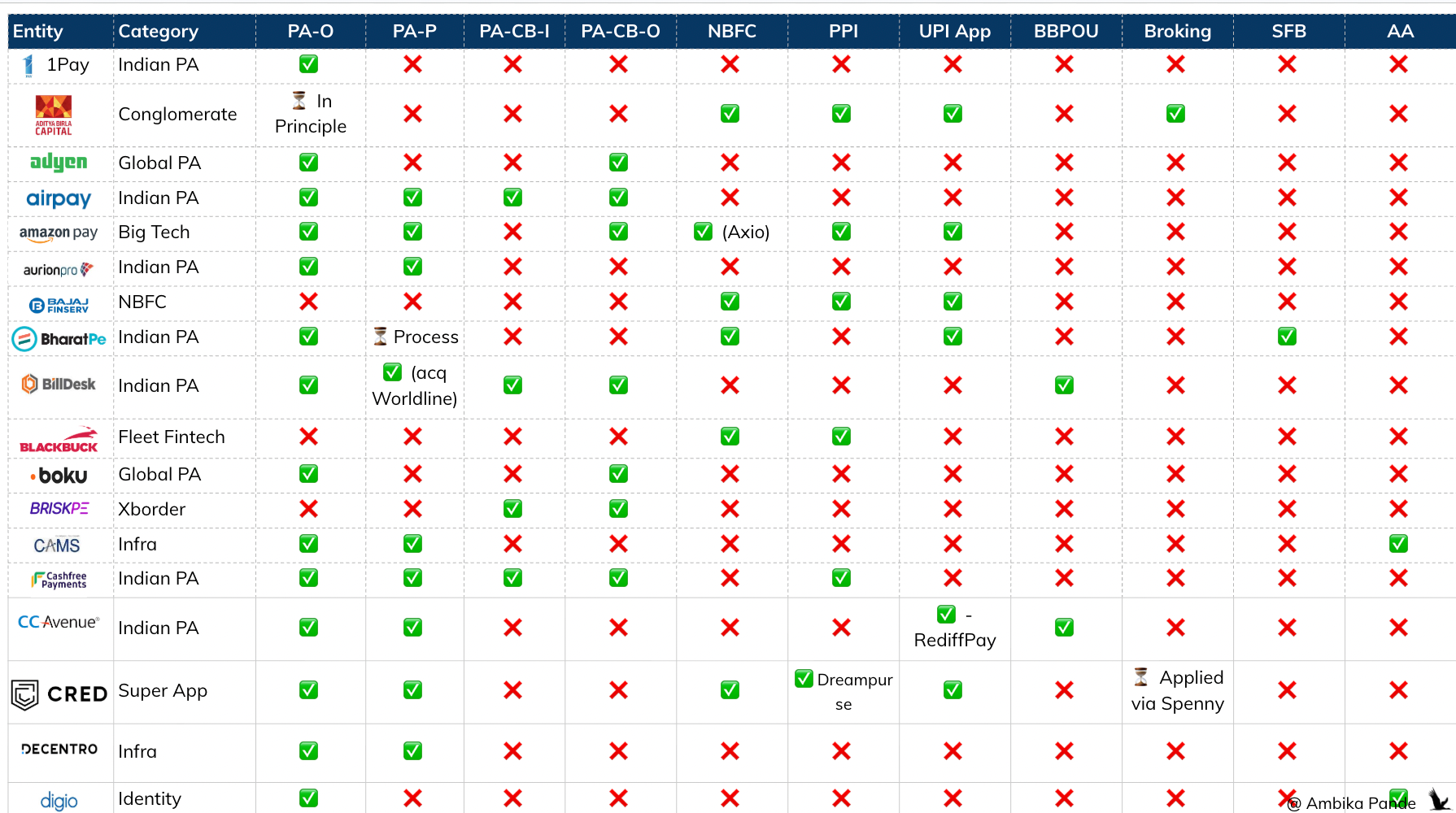

Now, the second part of this article, where we take a look at the initial license aggregation story, and see where fintechs sit in terms of licenses, specializations, and apart from what I discussed above, is there anything we can identify from what fintechs are going after.

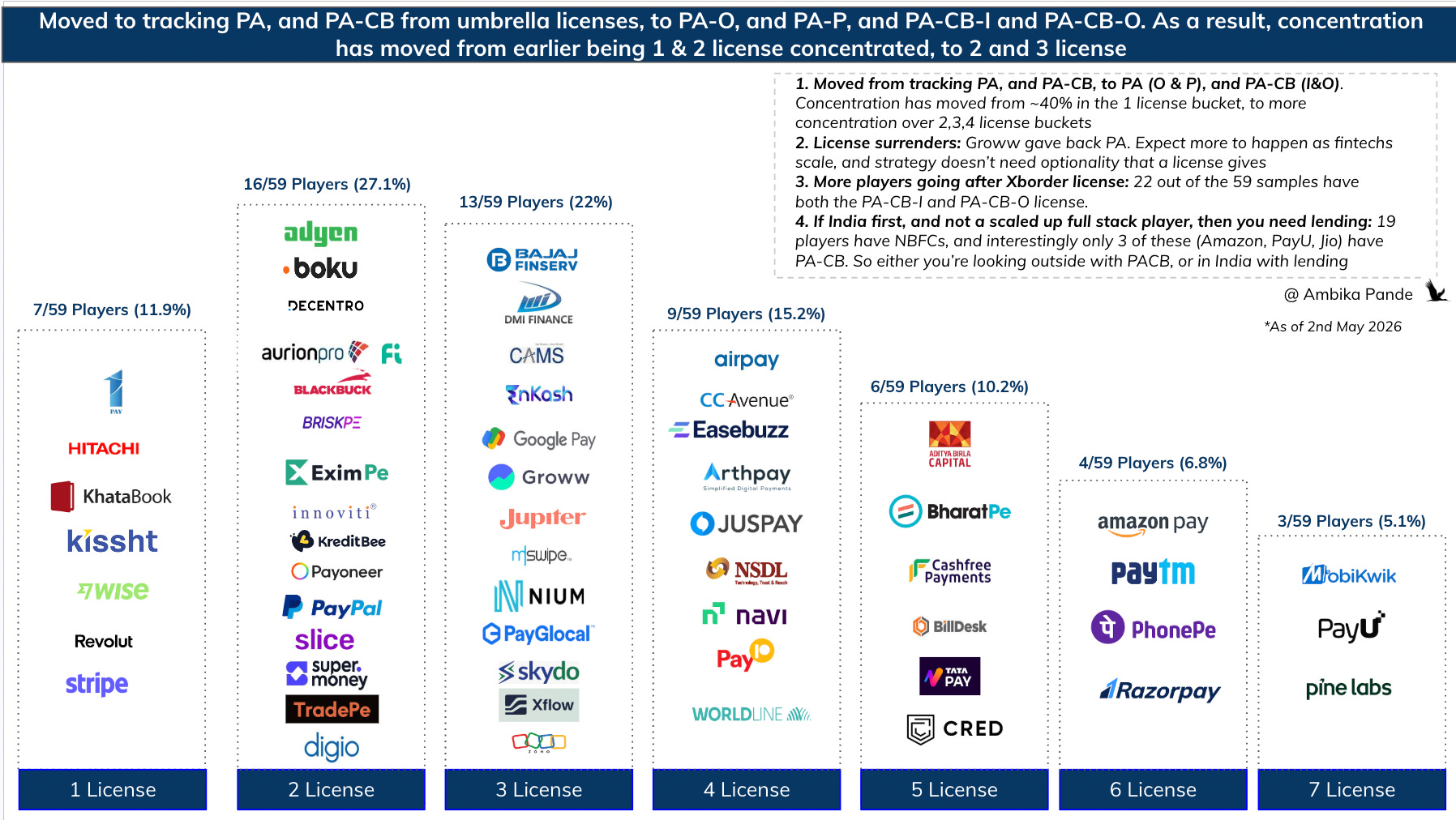

Note: This is a smaller sample set, since I have increased the number of licenses I am looking at. The last profile I did had 73, this time it is 59, but that was PA as a whole, PACB as a whole. PPI, NBFC, Broking, UPI App, and AA. Now, after the new regulations in September 2025, PA is broken into PA-O, PA-P, PA CB I and PACB O. Then, I have also added tracking for things like SFB, and BBPOU (for bill payments) to provide a more holistic view of what potential capabilities each platform has.

Some trends that I see:

One license fintechs (7/59) or 13.56%

This is mostly the PA-Online bunch (details in the appendix), although you have a few non PA-Online here such as Wise (PA-CB I), Kissht (NBFC, which just IPO’ed on 6th May 2026, at a ~12% premium) and Revolut (PPI - which is interesting).

Stripe. Needs no introduction. Pioneer of payment aggregators, big on card payments. Has struggled with UPI, like other non Indian players. It has a PA license, but voluntarily withdrew from the PA-CB (I&O). It is one of the companies I admire (the documentation and content is amazing, and they’re leading the world in the development of agentic commerce and machine payments.) But for a company that’s strength is their global merchant network, the fact that they have voluntarily withdrawn from PA-CB licenses is interesting. I’m pretty sure they’re still involved at a infra layer in terms of orchestration, but the cost of directly owning the customer is not worth

Wise: (cross border, money movement fintech): It has a PACB I license. I = inward flows. So, enabling investment in Indian stocks, or transfer to Indian clients. It is interesting to me that it doesn’t have a PA-CB O license, to help serve its international merchant base, by collecting money from Indian customers

Revolut: Global neobank, supremely profitable. $75B valuation, with reported $2.3B profits in 2025. This JUST has a PPI license. But according to their website they are targeting ~20M customers in India by 2030. Now, if they are, then ideally if they are moving money, they should get a PA license, and if they are targeting the 20M base, which is into international travel etc (which fits into their Revolut SIM / travel strategy), then they should also get a PACB (I&O), and UPI App. Remains to be seen, I expect them to beef up their stack.

2 license fintechs (16/59 or 27.1%)

Most fintechs that out of this sample seem to have two licenses atleast. The reason for this is possibly because from this piece onwards I’m tracking PA-CB I and PA-CB O separately, since fintechs have taken decisions to take one but not the other. Similarly with the PA license, this is broken into PA-O and PA-P, since there are fintechs that have chosen to take the online license, but not the offline. Because of that, while in past editions of this theme, the overwhelming majority has always been “1 license fintechs,” the distribution has shifted to sitting in the 2 and the 3 bucket. This is proven - take a look at the data below.

5 have PA-CB (I&O): Briskpe, Eximpe, Payoneer, Paypal, TradePe.

3 have PA-O and PA-P (Indian play) - Aurionpro, Decentro Innoviti

2 have PA O and PACB O - Adyen and Boku (international players, want to serve international merchants by collecting money from Indian customers)

👉 I did touch upon this briefly earlier: the NBFC + PPI / UPI App story.

3 have the NBFC + UPI App, which are Fi, KreditBee and Supermoney. Supermoney is under the Flipkart umbrella, and Flipkart got a NBFC license in 2025, so I’m counting this is more as a NBFC under an affiliated entity.

There is a UPI App and SFB story (which is like the Bank and UPI App story, but I’m calling it out here since it is Slice, that started out as a Fintech). And then there is BharatPe, which has a UPI App, SFB, and a NBFC (apart from other licenses).

1 has NBFC and PPI - Blackbuck. But I expect this to get a UPI app as well.

This combination of licenses, the NBFC + UPI App + PPI story is something that shows up in the 3,4 and 5 license fintech story as well. On another point: PPI expires is something to keep an eye on: MobiKwik PPI valid till Sep 2026, PhonePe till Aug 2026. Both are expiring within months, something to keep an eye on - if they renew or pivot

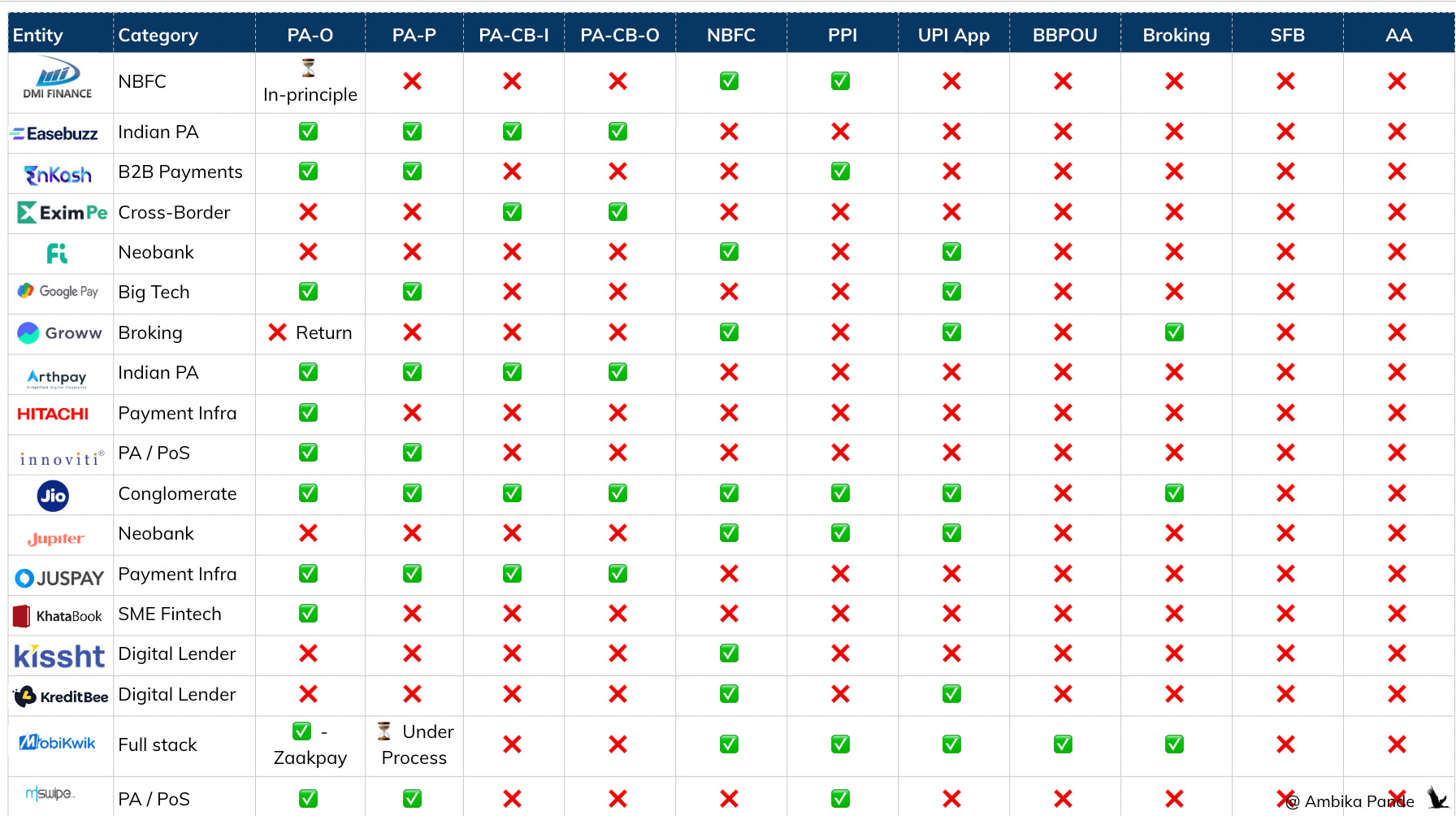

3 license fintechs (13/59 or 22.03%)

Continuing on from one of the trends identified in the previous section, we see that most that sit here are either some form of the payments play (PA-CB + 1 more), or India payments focus (PA-O, PA-P, and 1 more).

👉 NBFC, PPI, UPI App. The lending via UPI play. Two sit here, out of the fintechs I’ve profiles. Bajaj and Jupiter. More about this in the next edition, but it isn’t just payments (UPI) → lending. We’re also seeing the converse, where NBFCs are scaling up on UPI volumes.

Bajaj Fiserv (NBFC first)

ABFL (NBFC first)

👉 International focus. 4 sit in the PAO, PACB I and PACB O. Nium, Payglocal, Skydo, and Xflow. All very obviously are cross border first.

The PA-O seems to be something that is taken for optionality, since it’s not like the PA-O is required if you’re taking a PA-CB I / O license.

👉 Indian payments focus. The PA-O, PA-P and a third, depending on the strategy

CAMS. Has a PAO, PA-P, AA.

Zoho: PAO, PA-P, NBFC. Very publicly an India first company, although I’m unsure of how much this payments and fintech play has scaled for them. Despite all the hue and cry about them getting into payments, and fintech, it isn’t that easy.

Googlepay: PAO, PA-P, and a UPI App

Enkash and Mswipe have PA-O, PA-P, PPI. I do expect to see some consolidation here.

👉 Others in the 3 license bucket

Groww: NBFC, UPI App, and Broking. Surrendered it’s PA-O license. I talked about this in the headlines section, so I won’t get into it here.

DMI Finance: PA-O, NBFC, and PPI. It is a NBFC first, but acquired Zestmoney (BNPL) a few years ago, when it went bust. Seeing the trend of NBFCs getting UPI Apps for distribution, I expect to see something happen here

4 license fintechs (9/59 sit or 15.25%)

Especially because now I’m tracking payment licenses individually, it makes sense that as you get into more licenses, you probably have more payment licenses than anything else.

👉 Full stack payments: PA-O, PA-P, PA-CB-I, PA-CB-O

Airpay, Easebuzz, GVP, Juspay, sit here. Juspay is making big moves internationally. Then we also have some combinations.

CCAvenue or as we call them now: “AvenuesAI” versus plain Infibeam: PA-O, PA-P, UPI App (Rediff Pay, but no volumes yet), and BBPOU. So this is some sort of India first play. I guess they do have distribution, they are one of the original payment aggregators, founded in 2001.

Navi: Their PA-O (is under process), they are a NBFC first, have a PPI, and are a UPI App. Their UPI App is one of the top (not counting the top 3 - PhonePe, Gpay and Paytm). In April 2026, their UPI App processed XX

NSDL: PA-O, UPI App, they are a payments bank (they partnered with Cashfree to launch a UPI switch, which is part of the full stack play specifically in UPI), and they also have a AA (via Protean). You can read more about the full stack UPI play here: [#60] The UPI Dilemma: What happens when infra and apps are commodities.

Pay10: PA-O, PA-CB-I, PA-CB-O, PPI

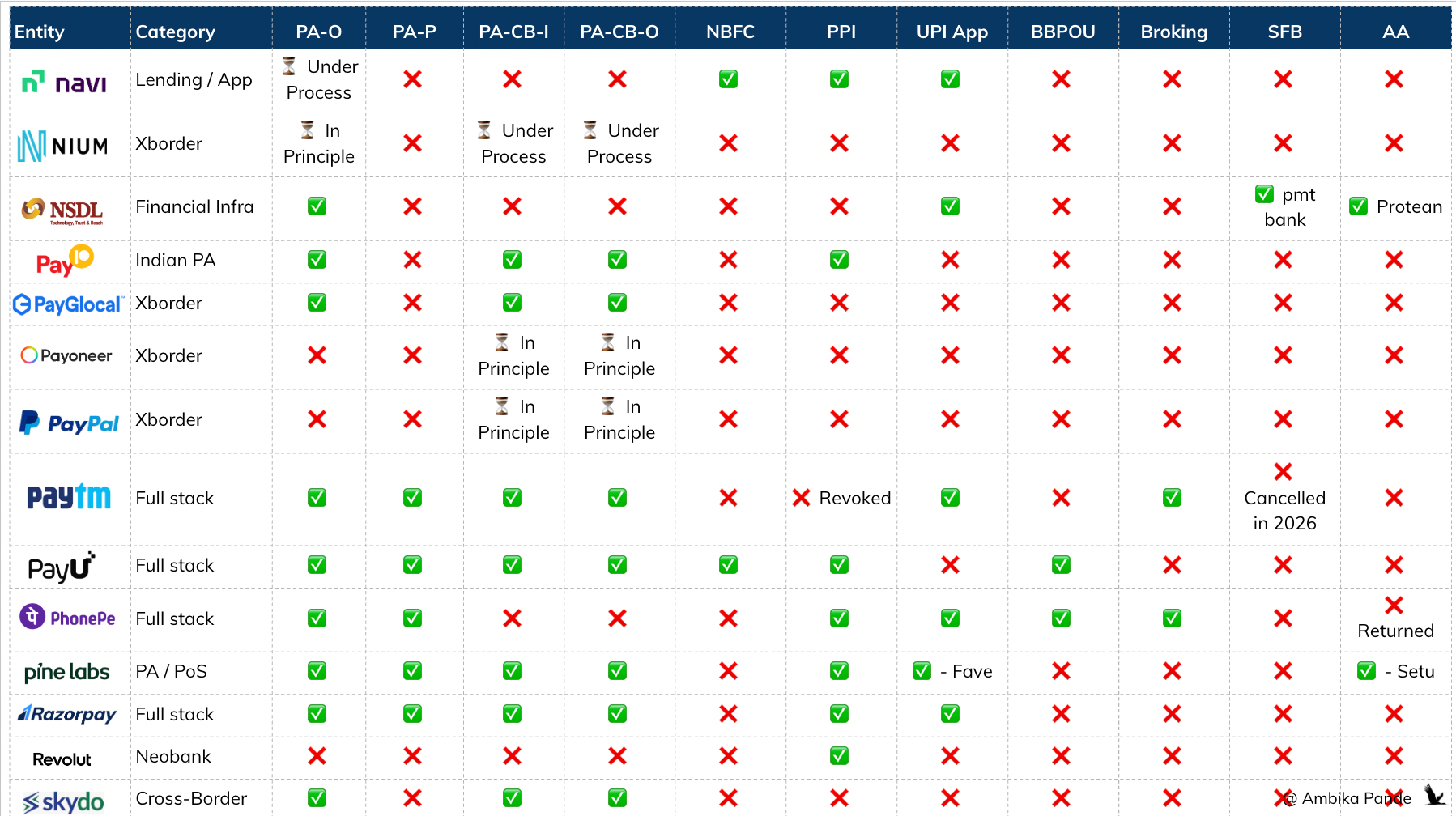

5 license (6/59 or 8.47%)

We’re entering serious infra players, or conglomerate territories in the 5 and 6 license buckets. Now, the more licenses you have, the tougher it is to make exact buckets, so here, I have bucketed via “most common license overlaps” between entities.

👉 Billdesk and Cashfree, have PA-O, PA-P, PA-CB I & O, and one more.

For the 5th license, Billdesk has BBPOU, and Cashfree has PPI. The way the payments space is going, I expect further consolidation for players with some volume. Razorpay, PineLabs, Paytm, PhonePe, PayU are the big 5, with each having online, offline acuriing volumes, some combination of both, or consumer volumes. With players such as Billdesk (although it did buy Wordline’s offline business in 2026), Cashfree, Easebuzz, Innoviti, and Mpurse, I do expect further consolidation in this space. Billdesk was actually on track to be acquired by PayU for $4.7B in 2021, but it was called off. The logic is simple. UPI is driving volumes down. Monetization may not come in anytime soon, and subsidies are not enough. With ~20%+ of market share, players are not profitable. So, the market may not have space for more than 3-4 players at this stage.

👉 3 have NBFC, PPI, UPI App, and then 2 others licenses.

ABFL: In additional also has PA-O, and broking. Aditya Birla umbrella - it is a conglomerate.

CRED: In addition, has PA-O, PA-P. I had read some news a few months ago suggesting that they were trying to get into broking via Spenny (which is a savings and investment platform CRED acquired in 2023), but no reports on confirmation of this.

TataPay: In addition, also has PA-O, Broking. TATA umbrella, conglomerate play.

👉 BharatPe: India first play. PA-O, PA-P, UPI App, NBFC, and is a SFB (Unity SFB), which happened via its merger with Centrum in 2021. It’s going to go for a Universal Bank license is my hunch, and I expect the same with Slice

I expect it to go for a Universal Banking License in a couple of years, which RBI has provided a path to. RBI’s minimum guidelines on the path for a SFB to become a Universal Bank is to have 5 years of successful operations as a SFB, be listed on public stock exchanges, and have a net worth of >= INR 1000 Cr. ($104M at current USD to INR exchange rates). For both BharatPe and slice, for this strategy to work, I expect an IPO in the works soon. On a side note. I had written a piece on how banking in India is evolving, and how banks are moving up the tiers. You can read more about it below:

[#78] Banking in India: FDI investment, bank consolidation, and the "great re-bundling"

![[#78] Banking in India: FDI investment, bank consolidation, and the "great re-bundling"](https://substackcdn.com/image/fetch/$s_!Xe0Z!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F800fcabe-2b7f-4397-8780-3456f829160a_1506x846.png)

Hi folks - and welcome to the first Painted Stork newsletter of 2026 🚀

6 license entities (4/59 or 10.17%)

As I said in the 5 license bucket, this is payments territory. Everyone here has PA-O, PA-P. Similar to the above section, I have bucketed via “most common license overlaps” between entities.

👉 PA-O, PA-P, PA-CB-I, PA-CB-O, UPI App - Razorpay + Paytm. More payments focus, with the strategy to leverage distribution

Razorpay: In addition to the above 5 licenses, Razorpay also has a PPI

Paytm: In additional, Paytm also has broking, through Paytm Money.

👉 PA-O, PA-P, PPI, UPI App: Amazon Pay, PhonePe

Amazon Pay. In addition, Amazon Pay also has PA-CB-O. It is interesting to me that they don’t not have PA-CB-I. So from an international focus, they seem to be more interested right now in providing their international merchants an option to get paid by indian customers, but not via versa. They also have a a NBFC that they got via acquiring Axio, which in 2025, which was a leading BNPL player.

PhonePe: PA-O, PA-P, UPI App, PPI, Broking, BBPOU. 50% market share in consumer payments, and a full stack fintech. Should be IPO’ing soon. Originally the target to IPO was in 2026, but reports suggest that this was paused due to geopolitical reasons. Other reports suggest it was because early predictions indicated, that PhonePe would list at a $9 - 10B, which was lower than their current valuation of of $14.5B (got via a secondary to General Catalyst in 2025).

7 license. (3/59 or 5.08%)

Fintech / payments territory.

PayU: PA-O PA-P PA-CB-I, PA-CB-O, NBFC, PPI, BBPOU. Reports suggest that they’re going to focus on scaling up their lending.

Pine Labs: PA-O, PA-P, PA-CB-I, PA-CB-O, UPI App, PPI, AA. Full stack fintech, but offline first. Shopflo should help strengthen their online case.

Mobikwik: PA-O, PA-P, NBFC (in 2026), UPI App, PPI, Broking, BBPOU. India first. Their NBFC license suggests a strong focus into lending going forward.

Appendix