[#81] Credit Lines on UPI (CLOU) will eat small ticket lending, but requires key ecosystem unlocks to reach that inflection point

All signs point to CLOU solving for existing problems in small ticket lending, but it'll require market awareness, a robust monetization construct, and NBFC enablement to reach that inflection point

There’s suddenly a lot of buzz in the market about Credit Lines on UPI (or as the term is now called - CLOU. How is it pronounced though - is it clue? Or perhaps clow (like clown, but without the ‘n’).

But the point is, Credit Lines on UPI, as a concept, have been around in the market since 2023. It’s been more than 3 years. And when it initially came out, no one was really sure what to do with it. Or even, what it was. Was it a new payment method? A new payment rail? Who was it even for? This is something Manan (Product & Strategy @ Vegapay) and myself have been discussing for quite a while - not the pronounciation (although that is also important), but what’s the potential?

Well, CLOU was promoted as being the messiah for small ticket lending in India. It aimed to bring together the best of both ‘affordability’ and ‘customer experience’ albeit in a kosher way that all regulated entities were comfortable with. But to understand this, let’s go back to the past.

How small ticket lending originally worked: This is the original LSP and lender aggregator model, and the problems

Well, the original LSPs (or lending service providers) were the Zestmoney’s of the world. They really put small ticket lending on the map, and were a key reason for the DLG (Digital Lending Guidelines) that came in. These players had the right idea - and essentially introduced the idea of ‘checkout affordability,’ which brought together the supply of credit, and the customer demand, at a specific point in time. Unsecured lending went up, with Zestmoney doing INR 300 - 400 Cr per month, Axio doing (I would hazard a guess, that there were similar volumes), Shopse doing probably half that in their offline model. While the demand, and the supply was there, what wasn’t there was a robust business model.

Credit goes to these players (excuse the pun): They highlighted the need for a model like this, and did whatever innovation they needed to make this work. (A key one being FLDG)

The concept of FLDG helped boost approval rates, but placed huge risk on the system

These lenders were able to boost approval rates with a concept called FLDG. FLDG is “First Loss Default Guarantee” where the fintech would commit to covering xx% of the lenders losses. To give you an example:

Let us say, lender A has disbursed 10 Cr through Fintech X. Fintech X has agreed to give a FLDG of upto 10%. This means that Fintech X will cover ALL losses of lender A, upto 10% of disbursal, which in this case is 1 Cr. (there is some negotiation here, it can be total disbursal, principal outstanding etc). So, in the case that Lender A loses INR 90L, fintech X will cover this entire amount. If lender A loses 5 Cr, Fintech X will still only cover 1 Cr and no more.

Problem #1: Approval rates were boosted because of the FLDG concept. Lenders knew that upto xx % of losses would be covered, so they didn’t do the due diligence that they should on some of these customers

When this model originally started, FLDG was as high as 100% of the disbursed amount! And then gradually this reduced to about 10-20%, but the amounts were still extremely high. That is one reason DLG came in, RBI got extremely cagey with a ‘non regulated’ entity taking so much of risk. And if these risks blew up, and the fintech was unable to pay, it could cause a collapse of certain financial institutions!

Note: Although DLG mandates FLDG to be ~ 5%, there are a lot of ways to get around this, you can put an ‘equivalent’ deposit in the bank the size of the credit supply you want, or even have a lien on a FD, in the name of the lender giving the supply of credit.

Problem #2. Lack of lender liability: there weren’t any guidelines around this, so a lot of lenders offloaded KYC and customer verification onto the fintech itself

The customer here would be a customer of the fintech. The fintech would onboard the customer, do the KYC, and match the profile of the customer to the lender policy. All the lender had to do was accept the customer profile, accept the documents that the fintech had collected and verified, and just disburse. The customer wouldn’t even know who the lender was unless they bothered to check their email, and that too, the email they would get would be from the fintech, specifying the details of the loan. Naturally for most customers, they probably didn’t read it in detail, assuming that all was well.

Problem #3: Not being able to get to the right TG:

There were two types of customers that these fintechs pulled.

Customer type #1: Low risk customers, who had options to take other credit products, and probably had 1-2 credit cards. And they weren’t willing to pay any interest or extra fees. So the ‘3 month no cost EMI’ was set up for customers like these. And someone had to bear the cost of the interest on the loan. This would end up being either the fintech itself (under marketing expenses, and especially if the merchant had a lot of leverage - like Amazon), or in some cases the merchant would bear the cost. (the concept of subvention). So here, there were high marketing expenses

Customer type #2: This customer type wanted the credit. They needed that affordability. But these was also the desperate customer, and NPAs and collection costs were higher

There were customers in the middle - that were probably customers who didn’t have as much access to credit as they’d like, but at the same time, were not at risk of default. But in this model, identifying them was difficult, since every customer was a NTB (or new to bank customer), and the lending was mostly happening via NBFCs.

Problem #4: transparency in general: these small ticket loans were given by an entity under the term ‘credit lines’ when they were essentially small ticket loans

You had a player like Fintech X telling the customer that they were eligible for a credit line of INR 1,00,000. But this wasn’t actually a credit line. Every time the customer transacted, there would be a small ticket loan that was taken. Example:

The customer was told that they got a INR 1,00,000 credit line from the fintech. Actually this was just the total drawdown amount. The customer would then transact at various places using this, and instead of being reported as a usage against that limit, it was reported as an individual loan! Example:

Electronics: INR 10,000: actually reported as a 10k loan to the bureau

Clothes: INR 5000: reported as a 5k loan to the bureau

And customers were never aware of this! In their minds, Fintech X gave them the credit line, and they were using it like they would a credit card. They didn’t know that Fintech X was just the aggregator, and in the backend, it was a Piramal, or a ABFL giving the loan. And that in reality these were small ticket loans, and if you take multiple small ticket loans like this, it’s going to really damage your credit score. Which is what happened: customers found their credit scores affected, and severely hurt them when they tried to apply for auto / home loans on other platforms.

There were a bunch of players operating here, some are still operating while some got acquired / pivoted their business model

Lazypay: in-house lending arm of PayU, powered by PayU Finance, an NBFC. Operations slowed down a bit in 2021 - 2022 after the crackdown on unsecured lending. In FY25, PayU got investment from its parent entity, Prosus to boost its credit offering

ZestMoney: Was doing INR 300 - 400 Cr per month. NPAs boomed, marketing expenses went through the roof (3 month, no cost EMI), ended up being sold in a fire sale to DMI Finance in 2024. Zestmoney had an in-house NBFC.

Axio: Again, was doing 200 - 400 Cr per month, majorly through Amazon. Was wholly acquired by Amazon in 2025. Axio also had a in-house NBFC.

Slice: Tied up with banks (SBM) to use their PPI license to issue cards linked to a PPI wallet, which were infused with small ticket loans from the partner bank. Essentially it was a small ticket loan pretending to be a revolving credit line. DLG came in, and shut down this model, and Slice merged with NE SFB in 2023 to become a small finance bank. My bet? RBI provides a way for SFBs to become universal banks after 5 years of operations, and among other things, the bank also has to be public. I expect an IPO soon. I had written a piece on SFBs, that you can check out here: [#78] Banking in India: FDI investment, bank consolidation, and the “great re-bundling”

The point being, that due to regulatory uncertainty, a lack of systems being set up to actually support this (credit bureau, loan vs line, targeting the right customer base), in hindsight (which is 20/20) this was always going to see roadblocks

Fintechs with no regulation, and lack of capital adequacy to adhere to were giving massive guarantees in case of failure! If some sort of massive default happened for a fintech with very high FLDG, and it was actually required to pay it up to the lender, it quite probably would not be able to, and cause a collapse

Not able to target the right customer: Going after the credit worthy customer required huge expenses to subvent the interest. Going after the risky customer required funds to manage NPAs. And fintechs seemed to be unable to actually isolate the ‘right’ customer for this product - the customer with a bank account, and not enough access to credit.

Not able to find a balance between affordability and customer experience: The onboarding flow to actually get this was very long and convoluted. Only the customer who REALLY wanted the credit would go after this. It was not seamless enough to attract the customer who maybe had another option. The affordability AND good customer experience was not being met, players were either solving for affordability (Zestmoney, Axio), or for experience (Slice, Jupiter, and 1-click players such as Lazypay, Simpl etc, although I would argue it wasn’t really a credit product, it was a 1-click payment product that was being powered by credit)

Ecosystem wasn’t set up for these sorts of credit products: All these innovations in credit, required systems that were flexible enough to understand. Things like ‘partial cancellation,’ (imagine you buy 2 t-shirts, return 1), or grace period (3 days no interest in case the customer forgot) were things that existing bank systems find tough to understand, requiring a lot of manual recon. And of course, whole issue of credit bureaus treating each transaction as a separate small ticket loan, instead of credits and debits against a line really ended up screwing the credit score of a lot of customers

What we do owe thanks for to these OG players, is that they brought to light a market that clearly existed - what was needed was to figure out the right model that could serve it sustainably

Demand: atleast 1000 Cr per month (if I combine all online / offline small ticket lending sources) ✅

Product Opportunity: Being able to provide “affordability” options, with a good customer experience ✅

Distribution: Already existed via consumer apps, checkout pages, and POS terminals offline, where the supply of credit could be connected to the customer at the time when they needed it ✅

CLOU (clue? clow?) solves not just for the affordability + CX piece, but also the regulations of it all

I’d say that Credit Lines on UPI is an outcome of all the original innovation that the OG lending fintechs did. And it solves for most of the problems that exist.

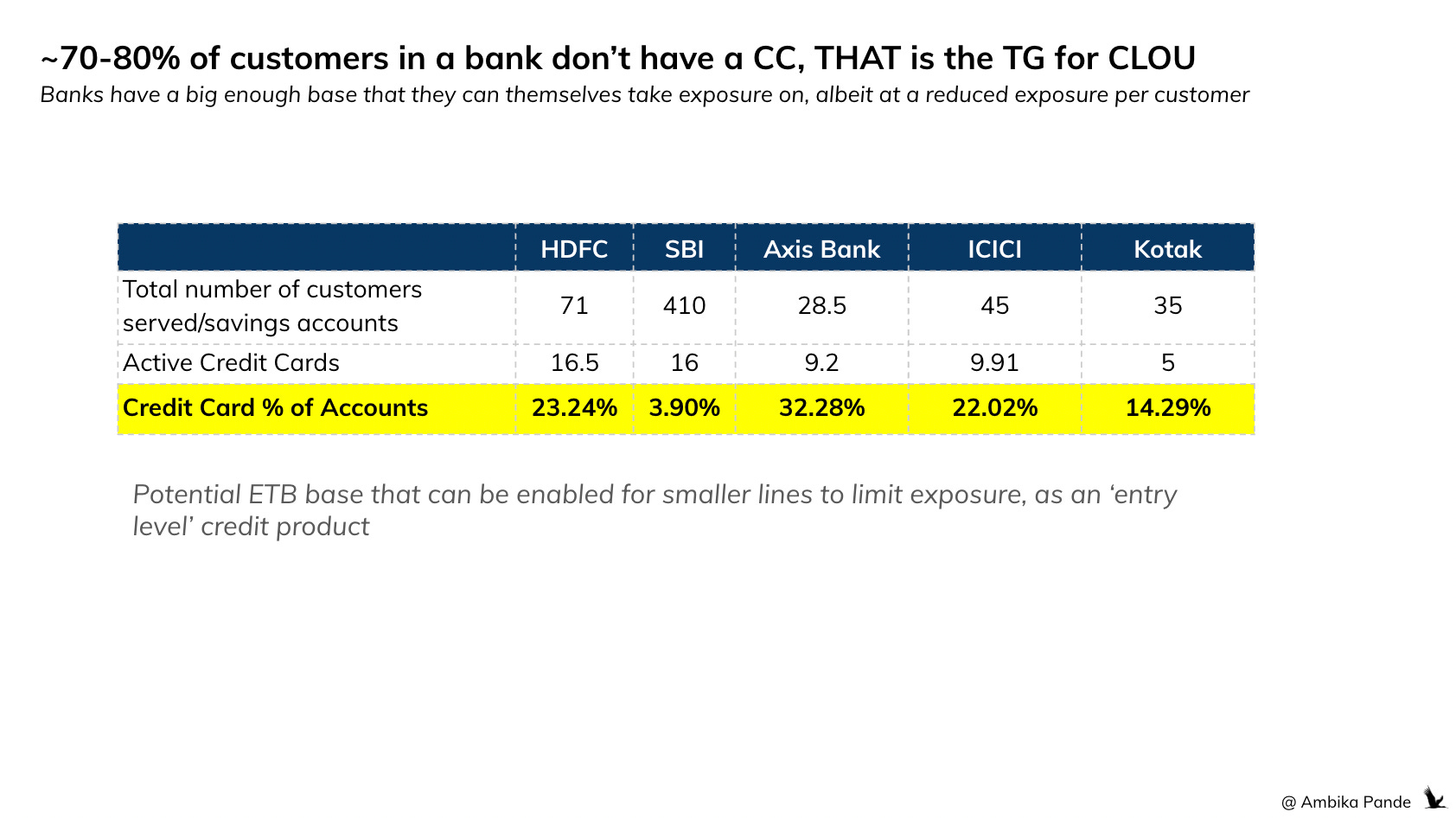

It solves for ‘experience’ because it is a product that is marketed towards the ETB (Existing to Bank base). Let’s break down the bank customer base shall we? In any bank, 10 - 20% of the creme de la creme customers are the ones that get a credit card. There are still ~80-90% of customers who have a bank account, and probably half of this who are credit worthy. So the whole “additional effort” and the ‘friction’ that exists in user onboarding journeys for NTB (new to bank) customers goes away, since this already a customer known to the bank. I equate this to a flow that is similar to a customer using their mobile number to avail of offers, here I assume there would be a PAN entry step as well.

It solves for affordability, credit lines start at INR 10k, but I’m assuming the sweet spot would be INR ~30 - 50k (and these can be revolving / non revolving).

It de-risks the bank since this is a customer already known to them. Through other features on UPI such as Autopay, the user can also set up repayment, which helps reduce collections cost for the bank, AND makes them amenable to take lower exposure on a higher number of customers. I’ll give an example: banks (and even NBFCs) don’t really like small ticket lending that much. Because the cost of NPAs and collections is usually not worth it, and at an absolute amount, higher than the revenue they’re probably making from a INR 5000 loan. Now, if there is a seamless way to set up collections, then this cost reduces, and probably makes the economics look a lot better

Distribution is solved, which increases usage, and revenue TAM: 400M individuals are anyway on UPI. This is a method on UPI rails. So it’s not an additional headache, like it is in current lending flows, the process of using this to pay is fairly seamless, and it is familiar, unlike currently flows across lenders which are fragmented

Monetization seems to be there: The reason why earlier lending fintechs went bust (apart from general operations in the ‘grey’ area of regulations), was also because monetization was tough. Lenders would make money through the interest, merchants would benefit from the increased frequency and average order value (10-15%) due to a credit method being enabled, and the lending fintech would make money through processing fees (and that also would be lost by the time you account for marketing / subvention expenses). 1.2% MDR is mandated on interest free lines.

A common question I hear is: Isn’t this the same as a credit card? What is it actually solving for?

Well, yes and no. Is a credit card a credit line? Sure. But banks see a credit card product in a very specific way. A ‘Credit Card’ product is defined. It’s been around for a while. It has defined systems, and defined policies. Banks mandate that a credit card can ONLY be treated in a certain way, and only CERTAIN customers are actually eligible for this. An example:

A credit card is not a very flexible product. It provides a revolving credit, with some % if you don’t pay on time.

There is a minimum payment, or complete payment option available at the end of every month

Only the top 10-20 % of the bank customers get the credit card. It also comes with a host of other perks (lounge access, reward points, which by the way are funded by the issuer bank only, so there is vested interest in giving these perks to the top customers who probably don’t use all of them)

It’s built with a premium customer in mind, it’s not seen as ‘entry level’ credit.

At its core, that is not at all what Credit Lines on UPI are solving for, and there-in lies the difference

In a nutshell, Credit line on UPI, or a CLOU, is a revolving or a non revolving credit line. It is a ‘small ticket credit limit, that allows banks to take less exposure on thin file, or riskier customers, but still on customers that they know.

It is primarily aimed at the customer who needs this credit, and not necessarily a premium customer. Think of it as a construct that allows credit to be given in an incredibly flexible fashion. Example: You want a 1 week, no interest limit? Sure, we can give that via CLOU. How about 2 months, @ 10% interest? That is possible too. And, unlike the core UPI method, which is 0 cost, this is a way of getting UPI stakeholders to actually make money. There are 2 models:

Interest free lines: These have 1.2% MDR

Interest bearing lines: These have zero MDR

Just looking at the type of investment, and the stakes that existing fintechs have on UPI, I’d actually expect them (once CLOU scales) to invest heavily here, as it allows them to attribute some of that revenue to the core UPI, which is currently a cost centre, not a revenue generating asset.

There’s also another angle: Credit Cards are inherently a more expensive method for the bank

Credit cards have a gross interchange of ~2.1%. After accounting for network fees, BIN fees, technology costs, and blended merchant categories, the net interchange in a bank’s P&L is ~1.2%. CLOU has a gross interchange of ~1.2%. After adjusting for network costs, lower interchange merchants, and zero-MDR categories, the net interchange is ~0.85%. While this appears lower on the surface, CLOU removes several structural cost layers that exist in cards:

No BIN ownership costs

No plastic manufacturing or delivery

No card lifecycle management in core systems

No re-issuance or replacement costs

No POS-linked reward or lounge infrastructure

As a result, the effective unit economics per active user are comparable to, and in some cases better than, cards, despite lower headline interchange, because there are fewer costs, easier distribution, and easier usage.

Distribution and activation further strengthen the case. CLOU is embedded within high-frequency UPI flows, leading to:

Lower customer acquisition cost

Faster activation compared to cards

Higher transaction density, even with lower initial limits

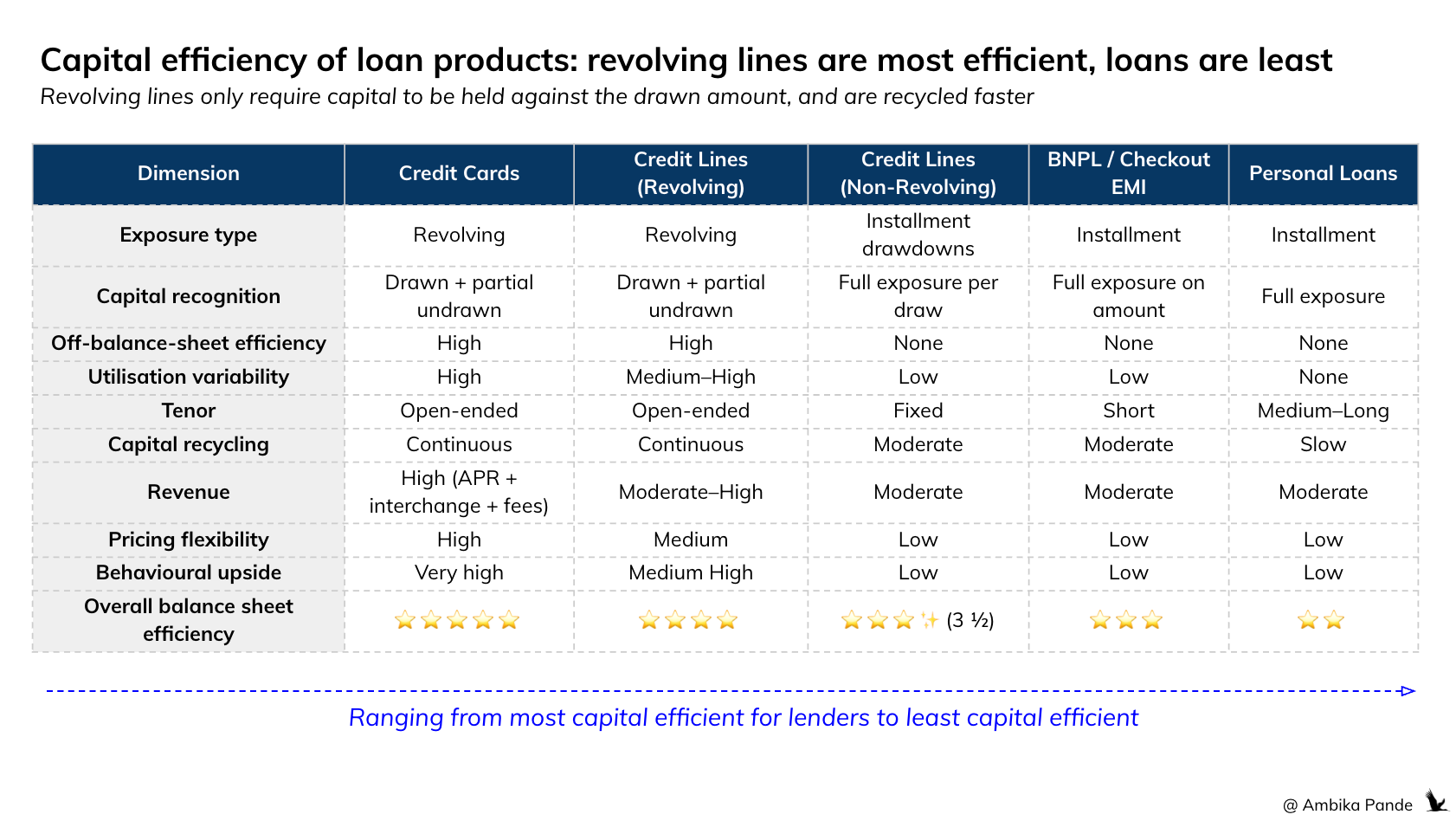

CLOU are also more capital efficient than term loans

Capital efficiency is essentially how much lending exposure can a lender take for each unit of regulatory capital it must hold. In simpler terms, If Product A and B both are required by RBI to hold INR 100 as a capital buffer (almost to protect against losses in case the customer defaults), and Product A generates INR 10 as profit, and Product B generates INR 50 as profit, then Product B is more capital efficient.

Capital recognition: When and how much of a credit exposure gets counted toward risk weight assets, which determines how much regulatory capital the lender must hold. Credit Cards are super efficient here, since the lender holds capital of the ‘drawn limit’ and a % of the ‘undrawn limit.’ Example: The user’s limit is INR 100. The user has utilized INR 60. Capital is held against this INR 60, and some % is held on the balance INR 40, which is usually 20-25% (called CCF or credit conversion factor). Credit Cards are efficient since capital is not held against the whole INR 100. Loans are very inefficient, since capital has to be held against the entire disbursed amount. Revolving credit lines are closer to credit cards, while non revolving credit lines are closer to loans with 1 key difference: the capital buffer ideally should be taken against the ‘drawn amount,’ not the total sanctioned amount.

Ranging from most capital efficient to least capital efficient, I’d rate it as:

Credit Cards → Revolving Credit Lines → Non Revolving Credit Lines → BNPL / Checkout EMI → Personal Loans

Okay, sounds good in theory. But what is the actual scale and ecosystem readiness for CLOU? It has been around since 2023

Lets take a step back to answer that. What is needed for CLOU to scale, firstly?

Systems that support a flexible credit construct: The likes of Vegapay, Credit+ allow banks to actually handle new and flexible types of credit products. I’d say this is in the market. In fact, Paytm Postpaid via SSFB, BharatPe Pay Later with YBL, and Navi have all been launched via Vegapay

Bank buy-in: Banks have to buy into the concept of a credit line, and understand that this isn’t a product that will cannabilize their existing credit card base, but rather, enable them to give credit to the base of customers that currently do not get it. My view? This will probably take a bit of time, since banks aren’t really the suppliers that are giving small ticket loans, those are NBFCs. Which brings me to my next point

NBFC enablement for Credit on UPI: What is the current product that this competes again? Small ticket lending. Who powers that? NBFCs! So by opening this to just banks, you’re not really solving any problem per se, banks were never REALLY looking at going after this segment with hammer and tongs. It’s the NBFC enablement, which wants to do small ticket lending, which will solve for this

Distribution via UPI Apps, and merchant networks: UPI Apps are easy. But a big part of small ticket lending also happens via checkout - the erstwhile checkout affordability, which contributed to majority of Zestmoney and Axio volumes, especially on e-commerce. Being able to 1) Get merchants exited about this, via co-branded lines and 2) work with suppliers for a simple activation flow at the time of payment - usually merchants are against this, is another lever. This also helps reduce CAC, and makes this easy to activate and distribute.

Usage is easy - it can be used anywhere there is a QR: Theoretically, this is true. Practically though, I will say that this does require merchant buy-in, since this is a method which could possibly have MDR attached to it.

CLOU also solves a long-standing gap in Indian lending: profitable, compliant small-ticket credit. Unlike BNPL, which RBI mandated must follow credit-card-like guidelines if interest-free, CLOU products are structured cleanly as OD, EMI, or card-equivalent products from day one, avoiding post-facto compliance risk. Importantly, CLOU is emerging as a large scale NTB (new to bank) and NTC (new to credit) acquisition engine. Banks are acquiring customers at very low marginal cost while remaining profitable, something that card programs increasingly struggle to achieve.

In terms of scale, it was around ~100 Cr per month in 2024. Some % above this is probably what it is at today

Now, real talk. I’ve spent this whole article talking about how the construct of “credit on UPI” will take off, and how it is the next big thing in credit in India. I think what has a lot of people excited, that just in terms of how this offering is constructed, it can actually solve a lot of existing problems in the current construct of credit products in India.

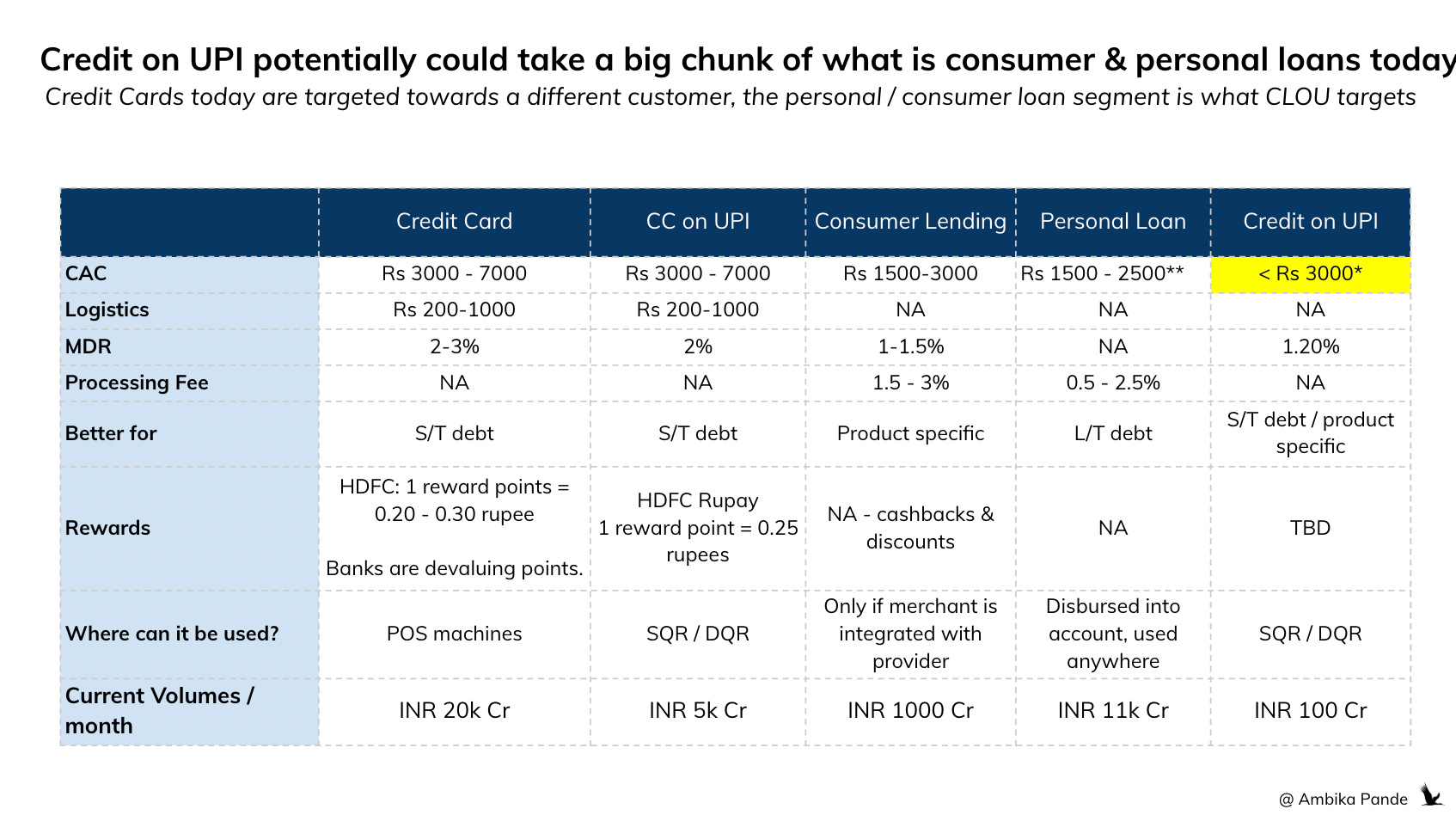

As a product, it is primarily built to target not the top 20% of customers, which are being served by a Credit Card (Mastercard, Visa, maybe Rupay), but the middle, which don’t have access to a credit card yet, but want some sort of credit account that they can use seamlessly and wherever they spend. Right now, those customers shop using consumer loans, or take personal loans, and then use that for their expenses. THAT is the base that CLOU is targeting. Again, very high level numbers, but the personal loan market in India is INR 11k Cr. And just in terms of fintech lenders (I’m not counting players like Bajaj Finance etc that are present in offline stores), the consumer loan market is INR 1k Cr. These are big numbers that Credit on UPI has the potential to tap into.

So then why hasn’t it taken off yet?

Well, that is a good question. Multiple reasons:

Customer education on what a “credit line” is, is still probably not where it needs to be. Customer education → demand → supply will catch up

The ‘right’ suppliers of credit aren’t enabled on this. There’s a reason SFBs (Small Finance Banks) have moved on this - they are the challengers. But to truly open this up to the masses, we’ll need it opened to NBFCs

Merchant narrative needs to catch up: The actual tech going into enablement is not tough, but the ‘why’ merchants should enable this is something that is still evolving.

From a bank perspective, I’d say policy and underwriting haven’t reaaaally caught up to what this product is - it’s not yet another credit product for the premium base, but an entirely new credit construct, allowing banks to serve the 70-80% of its base that doesn’t have a credit card. To do that, risk teams need to start looking at customers differently: types of use cases, (gold, education, travel etc), the rate of activation, and be willing to take lower exposure but across a wider range of customers

An open question I have is on NBFC enablement: how will this work?

Let’s assume that this does open up to NBFCs and NBFCs can then give credit lines. How will this model actually work? It’ll solve for affordability for sure.

From an experience perspective, the first credit line will require full KYC. So unlike the bank flow, where the customer is already known to them, there is some friction that is introduced in this journey. But that’s okay. I see that as the first time a user is opening an account with a financial institution - the friction is expected, especially if this is a customer that wants / needs this credit.

The second is that the NBFC account will have to be linked to UPI rails, I’m assuming no problem in either, but this is a change in the current construct, which only allows PPI / bank accounts linked to UPI. Again, not a challenge, just something I’m calling out.

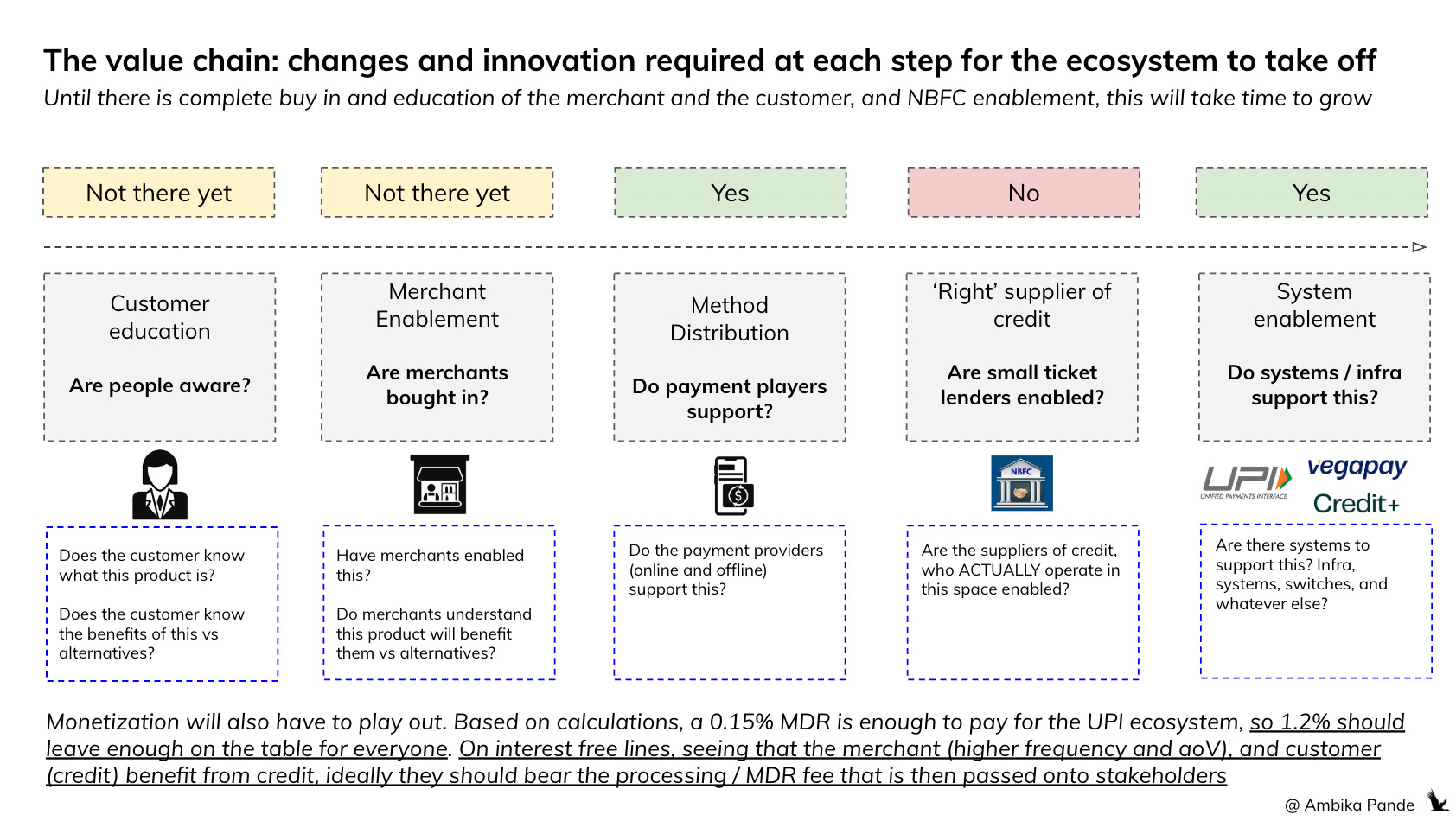

This isn’t really a specific product play, but an ecosystem evolution. And so, for this to take off, the ecosystem needs to open up on certain pieces

I’ve broken it down by the following:

Does the customer know about this and understand this product? Not to the extent that is needed, but I’d say that with the recent launches of Paytm and BharatPe, we are getting there 🟡

Do merchants understand this product, and the value it brings to them: Again, I’d say similar to the previous point. Not to the extent that is needed for this to take off, but something that is evolving. (example: credit increases frequency and average transaction value) 🟡

Do the payment players support it at the time of transaction? Example, at online checkout, and offline POS terminals, can customers see this as a way to pay? 🟢

Is the right supplier of credit enabled for this? Example: NBFCs are the entities that power small ticket lending in India, not banks. If they are not enabled, then the supply will never truly be there to help scale this 🔴

Are systems enabled? Are there credit line management systems? Is the infra ready? Can apps enable this? 🟢

By the looks of this, it seems like the ecosystem infra is ready to take off. What is missing are key levers to enable this, which are customer awareness, the merchant narrative (which are getting there to be fair). The key unlock will be NBFC enablement, and once that takes off, I see customer awareness going up as well.

So that is the first part. The ecosystem is ready. What is needed is some sort of inflection point, that will really be the ‘spark’ that makes this scale.

The second piece that needs to play out is monetization

There are two models.

1.2% MDR on Interest Free lines

No MDR on interest bearing lines

I’d done some calculations earlier on what it takes for UPI to pay for itself, and you can check out the details below:

![[#56] FY25 Budget Implications on UPI (Part 1): MDR on regular UPI transactions is now essential](https://substackcdn.com/image/fetch/$s_!5OAU!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fbdadd201-6844-4b81-b0f1-aadc51680154_1600x903.png)

But TLDR: 0.15% MDR on P2M transactions > INR 2k is enough to pay for the ecosystem. So, I’m assuming that 1.2% on Credit Lines on UPI is good enough to make sure that no one is losing money on this. But that is on the interest free lines.

On the interest bearing lines, I’m assuming that this will mirror the current construct of interest bearing EMIs. In the current construct of loans:

The lender charges some interest

The merchant pays some MDR for this method. This is either paid by them, or its subvented by the fintech facilitating this

Sometimes the fintech also charges a processing fee, either to the merchant or the customer for helping facilitate this transaction

But in interest bearing credit lines, there is supposed to be 0 MDR.

So then, there is probably still going to be some processing fee that the fintech facilitating this makes, the lender makes interest, and the folks on the infra side make their money from the cut that the bank / fintech is getting.

I’m harping on about the monetization because at the end of the day, this has to make money for stakeholders to invest in this

We saw that with UPI, that leaving the ‘market’ to figure this out is perhaps not the best way. It’s probably better if there is a defined structure that communicates the value, and monetization potential clearly, for all models, to ensure that this takes off. Market awareness, and the NBFC unlock is what is now needed.

Some things that I’m excited to see play out:

NBFC unlock - if this does happen, then the ecosystem will blow up, and this will drive customer AND merchant awareness

New credit products that are not bound to traditional 3/6/9 EMIs or 30 day revolving credit. With players such as Vegapay, Hyperface, Falcon and Credit+, I think this really depends on how creative merchants / lenders are, and how flexible systems are. I think the standard 30 day revolving credit, or the 3/6/9 month EMIs that were defined could change, with the type of credit really evolving depending on the use case.

Co-branded credit lines: Like a Paytm / BharatPe, but this is still at a UPI App level. I was thinking more in terms of merchants, especially those with frequent purchases. Example: a Zomato / Swiggy credit line that is payable every week

A credit orchestration play: An assumption here is that a customer could have multiple credit lines for multiple merchants use cases, if we assume #3 will play out. And in any situation, when there are multiple providers, there is an opportunity for an orchestration level player to come in, and in real time, direct the user to the most relevant credit method available.

All of this is exciting, no doubt. But what we will have to remember is that this is an ecosystem play, and multiple players need to be aligned for this to scale

A word of caution though. There’s a growing narrative among new age apps and infra players, that simply enabling credit on UPI is a path to winning the market. That framing misses the point. Credit Lines on UPI are not a distribution advantage by themselves. They are, at their core, a balance sheet and infrastructure efficiency unlock - a way for lenders to deploy capital more flexibly, reduce friction in disbursement, and potentially cycle capital faster. That, and the fact that this can be used via UPI rails reduces the barrier to entry significantly. That matters for lender economics, but it doesn’t automatically translate into customer adoption.

But let’s go back to the basics here for a second.

Customers don’t choose products because of the rails. They choose based on approval rates, pricing, UX, trust, and contextual relevance.

Distribution still matters. Underwriting still matters. Merchant integrations still matter. Positioning still matters. An app offering traditional loan products with better reach, stronger risk models, or clearer value propositions can outperform a CLOU native product despite CLOU being structurally more efficient for lenders.

The infrastructure is largely in place. What will determine outcomes is execution across the stack: policy alignment, compliance, risk discipline, distribution depth, and product design. It is important to remember that CLOU is an enabler, not the strategy.