[#91] The great fintech re-rating and the death of the India premium

The India fintech hope premium is dead. I benchmarked 50+ companies across 7 sectors and here's what the data shows

Hey folks, and welcome back to this edition of The Painted Stork!

It’s been a while since I looked at fintech through this lens. But with IPOs gathering pace, consolidation becoming inevitable, and profitability finally taking centre stage, it felt like the right time to revisit the market.

Indian fintech has also reached a different stage of maturity. The first decade was about proving that digital financial services could scale. The next decade will be about proving that they can become durable, profitable businesses. That shift is particularly important in India, where Digital Public Infrastructure (DPI) has dramatically reduced the cost of building financial products, but has also commoditized large parts of the stack, making monetization far more difficult.

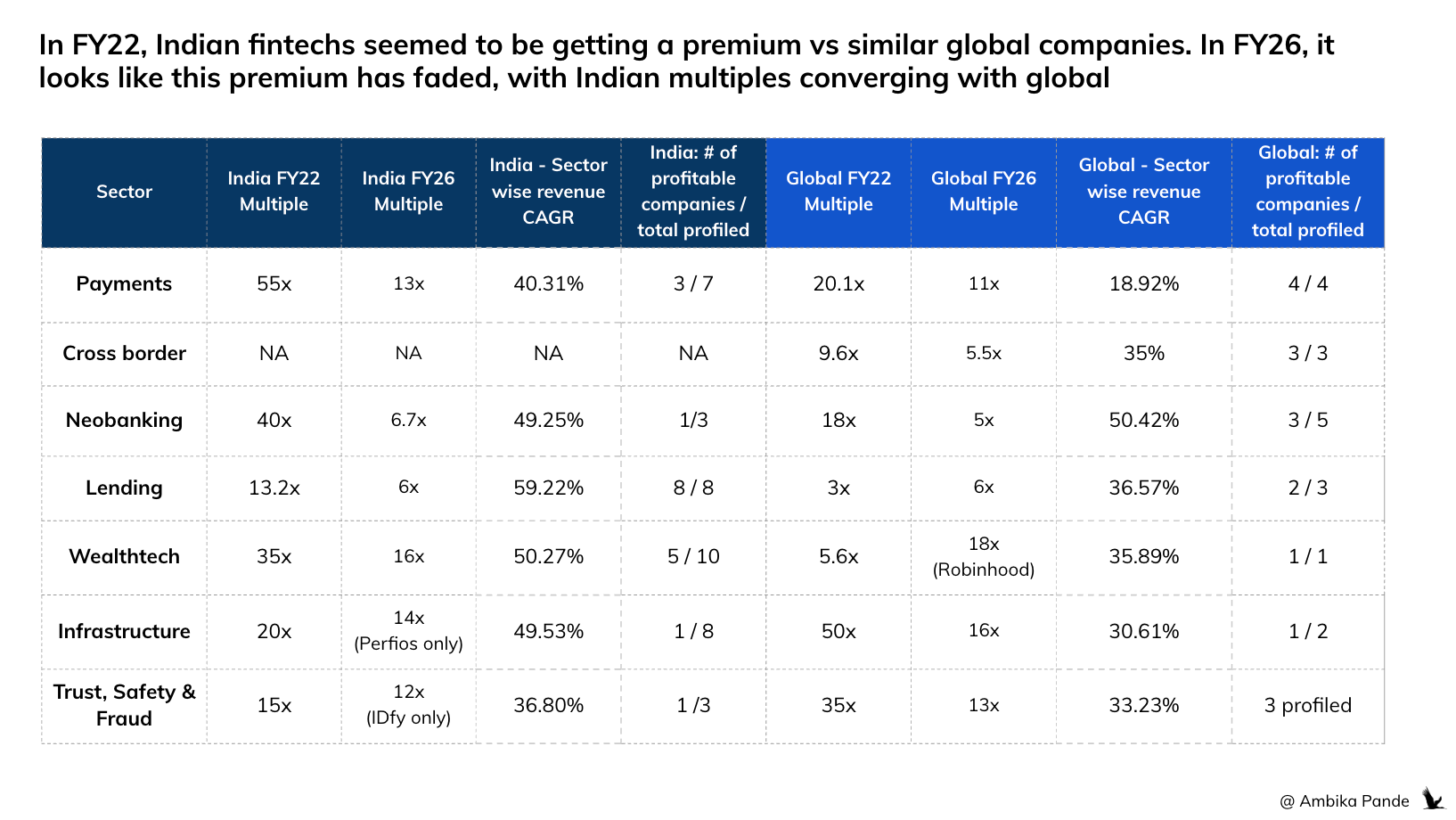

One trend stood out as I went through the numbers. In FY22, Indian fintech companies were consistently valued at a significant premium to global peers operating in the same segments. Investors were underwriting not just current revenues, but the promise of India’s enormous market: a population of 1.4 billion, rising digital adoption, and the belief that regulation would continue opening up new monetization opportunities.

Four years later, that premium has largely disappeared.

The market has become more realistic about what the addressable market actually is. Rather than 1.4 billion potential customers, the focus has shifted towards perhaps 50–100 million consumers and a few million digitally sophisticated businesses that can realistically be monetized. Growth alone is no longer enough. Profitability, platform depth, and durable business models have become the metrics that matter.

Which brings me to the title of this edition: The great fintech re-rating, and the death of the India Premium.

Over the past few weeks, I benchmarked Indian fintech companies against global peers across payments, cross-border, neobanking, lending, wealthtech, infrastructure, and trust & fraud. The goal wasn’t simply to compare valuations, but to answer a broader question:

Where does Indian fintech go from here? Which categories are maturing, which are only just beginning, and where will the next generation of large fintech companies be built?

How does India compare with Global companies? Lets go one by one.

I’ve looked at this across the above seven categories. The purpose of this space, is to understand revenue has grown, what profitability looks like, and how valuations have changed across both India and Global companies, across sectors.

Overall, it looks like multiples have normalized across sectors. with India multiples dropping more as a %, despite Indian companies having a greater revenue growth.

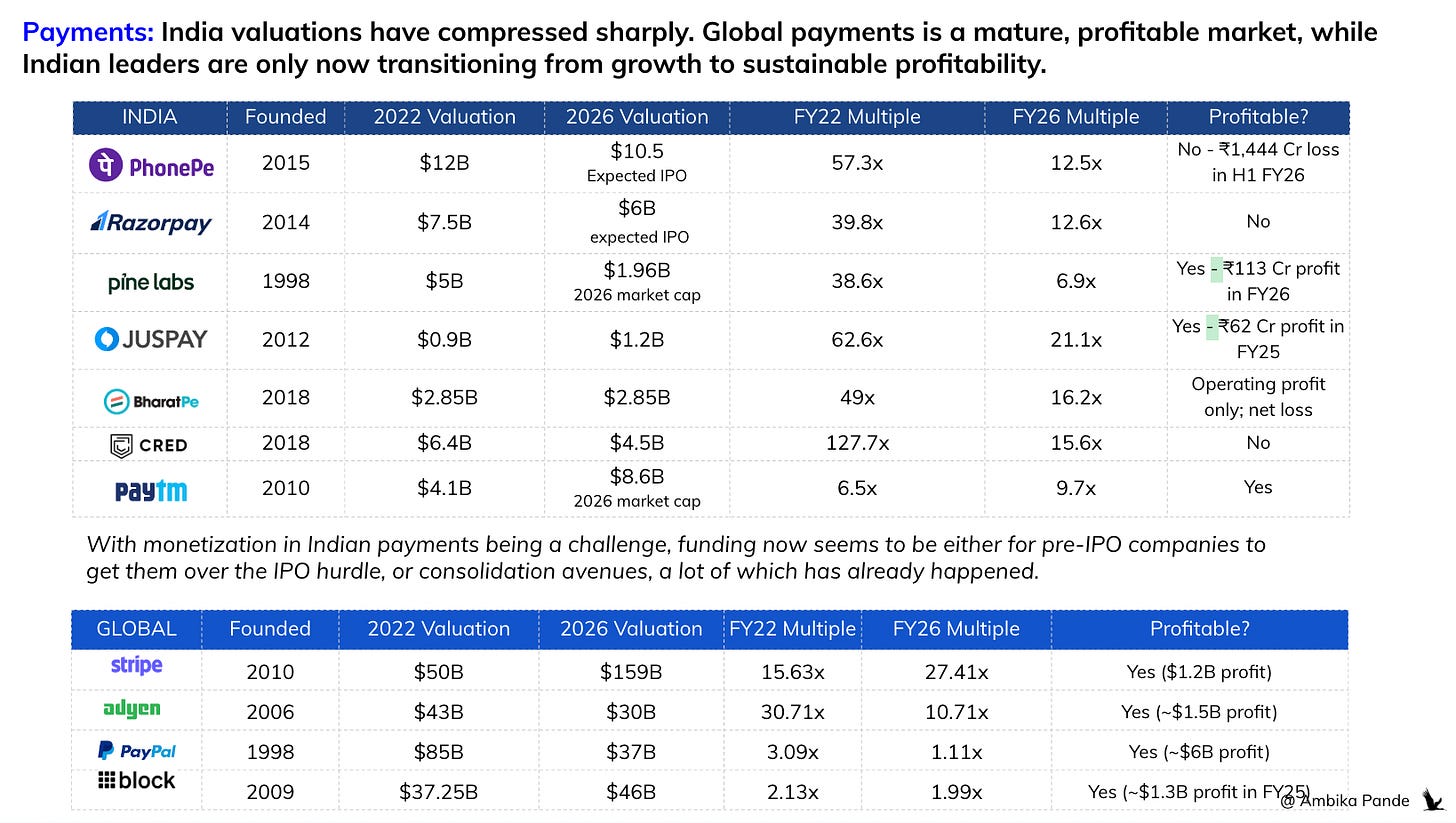

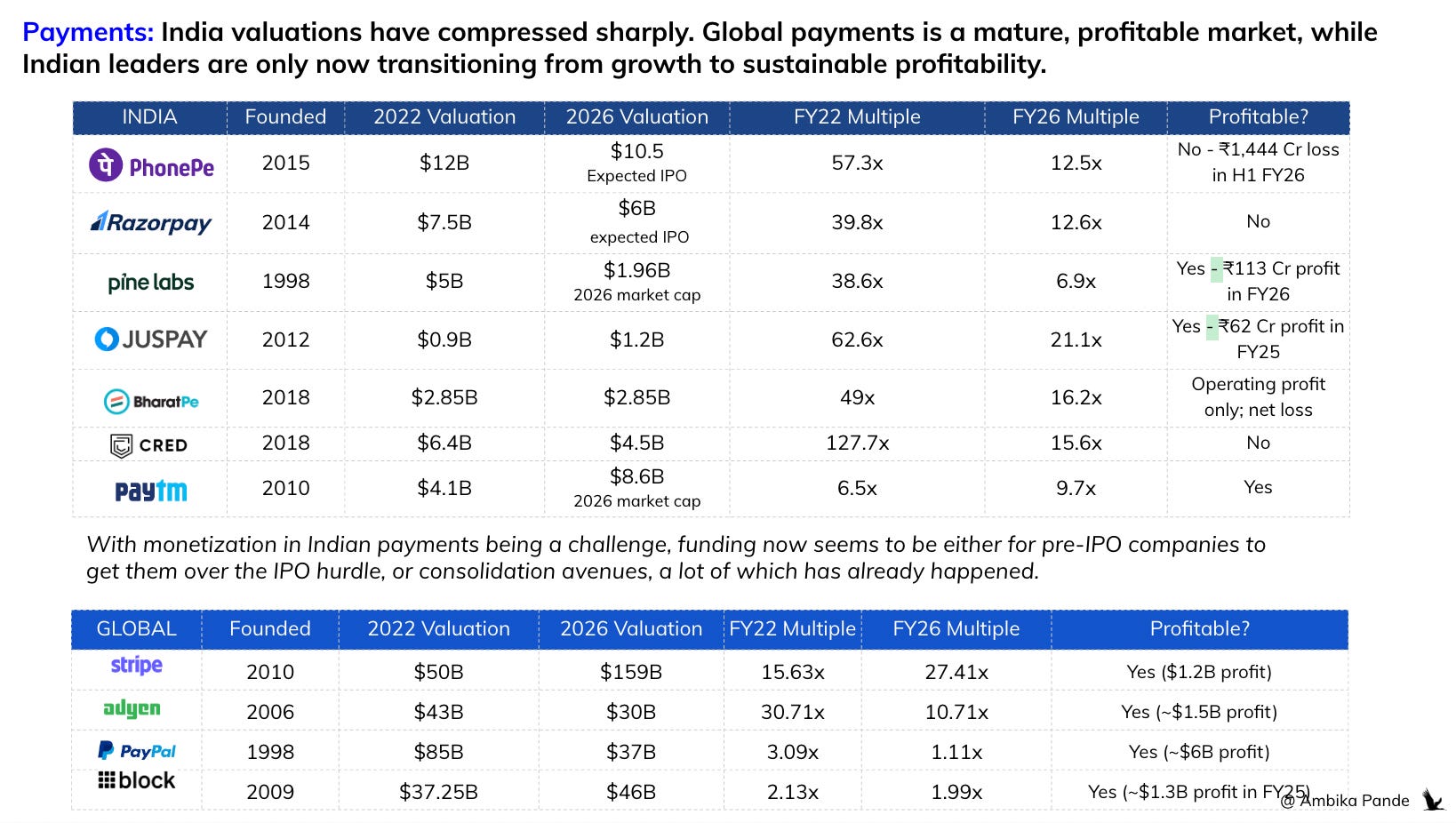

1️⃣ India valuations have compressed sharply. Global payments is a mature, profitable market, while Indian leaders are only now transitioning from growth to sustainable profitability.

In India, profitability is still a very recent phenomenon (coming in for 3/7 companies I looked at), and all happened in FY25 / FY26. Most established payment companies in the world seem to be profitable. India valuations in payments have also fallen more than global valuations. Stripe is the outlier here. Stripe was valued at ~$156B in 2026 after an employee tender offer. There was also a bunch of speculation in 2026 that Stripe was planning to acquire Paypal, but nothing really happened (till now). And with monetization in Indian payments being a challenge, funding in India in this sector now seems to be either for pre-IPO companies to get them over the IPO hurdle, or consolidation avenues, a lot of which has already happened.

Let’s look at the players here:

India first players → everyone is going towards a full stack play to own everything. All multiples are being corrected, in some cases, valuations as well.

Not profitable yet. 12 -14x seems to be the sweet spot

PhonePe: Market leader in UPI payments with ~49% market share. Present in B2B and B2C. Has applied for a NBFC license also - is a full stack fintech. Valued at $12B in 2022, and now eyeing an IPO listing of $9 - $10.5B in 2027 now looks like. Still unprofitable, made a lost of ~$152M in H1 in FY26. At a $10.5B valuation, and ~$842M revenue in FY26 (annualized), this is a ~12.5x revenue multiple, down from ~57x in FY22.

Razorpay: Market leader in online payments. B2B first, and then acquired a majority stake in Pop UPI (B2C App) in 2025. Acquired Ezetap (Razorpay POS). in 2022. Another full stack fintech, with international ambitions as well. Valued at $7.5B in FY22, at a revenue multiple of ~40x. Now looking to IPO at $6B in FY26 / FY27, with $450M revenues in FY25. Assuming a (VERY) conservative growth to FY26 of ~20%, this is a revenue multiple of ~12.6x. Not profitable as a whole yet.

BharatPe: Full stack fintech with an India focus. Payment aggregator, UPI App, NBFC, and a Small Finance Bank (49 % in Unity SFB). Valued at ~$2.85B in FY22 and FY26. Has an FY26 Multiple of 21x. Operationally profitable (excluding ESOP expenses), though not yet profitable on a reported basis due to stock based compensation.

Profitable

Pine Labs: Full stack fintech, but not too much of an online presence. Market leader in offline payments. Has a consumer play through Fave app, and also an international play. Valued at $5B in FY22. This dropped to a valuation of ~$3B pre-IPO. And now, its at a market cap of ~$1.9B. in FY22, it had a multiple of ~40x. Now this is at ~7x. Recorded its first full year of profit in FY26, at $12M (INR 113 Cr)

CRED: Diversified in terms of licenses, so the vision at some point was to be a full stack fintech. Practically, it has scale on the UPI App side (#4 in terms of value processed). Valued at ~$6.4B in FY22, which dropped to ~$4.5B in FY26 after the Meta investment. Multiple was ~127x in FY22, and now at a more reasonable ~15.6x in FY26. Still a little high, but it is now a META company. In June 2026, the Ken reported that CRED has just had its first profitable quarter.

Juspay: Payment infrastructure player, and expanding globally. Valued at $1.2B in FY26, with a $61M revenue in FY25, its FY26 numbers are not reported yet, but seeing that its revenues grew almost ~70% from FY24 to FY25, I’d assume a 50% growth from FY25 - FY26 in INR, which is ~$85M, which brings its valuation multiple to ~14x, which is down from about ~50x in FY22. Reported ~$7.5M in profits in FY25.

Paytm: Full stack fintech, international focus, and has a strong lending play, but through the TSP route; it does not lend on its own books. Valued at ~$4B in FY22, and now up to a ~$8.6B market cap in FY26, with a revenue multiple of ~9.7x. FY26 was its first full year of profitability, coming in at ~$53M profits.

International players → All profitable. Wide range, of 2x - 27x.

Note: FY25 is year ended December 2025.

Stripe: Full stack fintech, focus on agentic payments and stablecoins as well. Valued at ~$159B in FY26, with ~$5.8B in (net) revenue (year ended December 2025). Revenue multiple of 27x → it is the outlier here. ~$1.2B in profits in FY25.

Adyen: Simliar to Stripe. Public company. Had a market cap of $30B in FY26, and net revenues of $2.8B. Multiple has dropped from ~30x in FY22 to ~10x in FY26. $1.5B of profits in FY25

Paypal: Public company. Valuation dropped from a peak of ~$85B in FY22, to ~$37B in FY26. Multiple dropped from 3x in FY22, to 1.1x in FY26. $6B profits in FY25.

Block: Public company. Revenue multiple has hovered around 2x from FY22 to FY26. Valued at ~$46B in FY26. Profitable in FY25, of about ~$1.3B.

This sector has been around for a while, and profitability, not just growth prospects matter. Unless the ecosystem provides a path to profitability, I don’t see too many new companies coming in here, in India atleast, most of what will happen is consolidation, investment in mature companies to see them over to IPO, or shut down. Example: Cashfree as reportedly on the blocks, this was reported by The Head and the Tale, with Paytm and PineLabs both submitting bids. No news since then. Pinelabs bought ShopFlo (a checkout optimization company) for ~$9M in 2026. And CRED had ~20% acquired by Meta, with Kunal Shah leaving to head the global Whatsapp business.

What is happening in this space though, is a lot of these payment ‘powerhouses’ are trying to capture the mindspace in market positioning for ‘AI first’ and ‘agentic payments.’ They’re also racing to own the infra in the agentic payments world: stablecoins + agentic payment protocols such as ACP and MPP. (Although every payments infra company is doing this - Adyen launched Adyen Agentic in June 2026 which is a layer that unifies the different agentic protocols, Pine Labs launched P3P, a protocol that builds on top of HTTP 402 and UPI mandates for agentic payments).

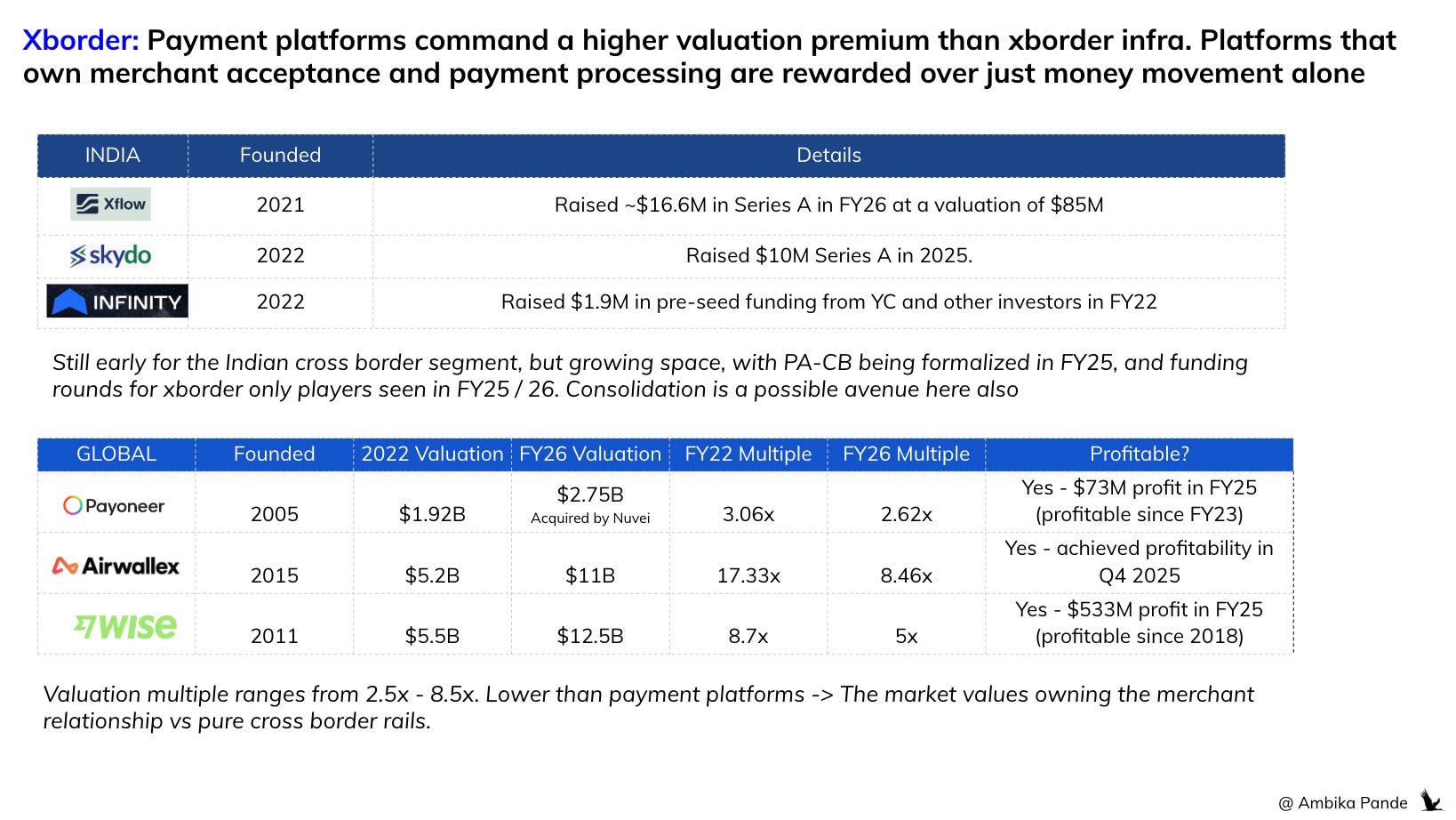

2️⃣ Xborder: Payment platforms command a higher valuation premium than xborder infra. Platforms that own merchant acceptance and payment processing are rewarded over just money movement alone. India is still early.

A clarification: these are players that are ONLY looking at international offerings, which could be payments, wealthtech or anything else. What is interesting is that companies operating here have lower multiples than full stack payments. One reason could be because full stack fintechs in payments ALSO have cross border as one of their business streams. But another reason is because a lot of the xborder players here operate as infrastructure (Airwallex for example). Not as the merchant facing entity. So that’s another lever: In a maturing space, clearly, your ‘growth’ potential is seen more promising if you own the merchant relationship.

India is still an evolving market, with most players being founded in2021 - 2022.

Xflow: Founded in 2021. Raised ~$16.6 Series A in 2026 at a valuation of $85M. I also saw a note somewhere that suggested that its operating revenue was INR 30 (~$3M) Cr in FY25, and on track to go ten fold in FY26. So seems to be a multiple of ~24x today.

Infinity; Founded in 2022. Raised $1.9M in pre-seed funding from YC and other investors in 2022.

Skydo: Founded in 2022. Raised $10M Series A in 2025.

International players here are:

Airwallex: Cross border infrastructure player. One of Airwallex’s biggest competitive advantages is that it has spent years acquiring local licenses, regulated entities, and banking partnerships around the world instead of relying solely on correspondent banks. It raised ~$320M in Series H, at a valuation of $11B in FY26, up more than 2x from its funding round in 2022, which valued it at ~5.5B. It raised its Series G in December 2025, where it was valued at ~$8B. And in FY25, it reached an ARR of ~$1.3B, so its FY25 multiple is ~8.4x.

Payoneer: Founded in 2005. Public company. Specializes in global collections and payouts. Acquired by Nuvei (global PSP) for ~$2.8B in 2026. With estimated revenues of ~$1.2B for FY26, this is a ~2.6x multiple it was acquired by. Reportedly it was profitable, making ~$73M profit in FY25.

Wise: Cross border money movement platform. Started out as B2C and then expanded to B2B. Founded in 2011. Public company. FY26 market cap of ~$12.5B, and FY26 revenues of ~$2.5B, so a multiple of 5x. The multiple dropped from ~8.7x in 2022.

The key in cross border is having the licenses to operate. And clearly, consolidation is a theme here as well, not just in domestic payments. And if the themes of ‘platformization - discussed later in this piece’ and ‘owning the merchant relationship directly’ play out, it is possible that there is some consolidation between the ‘full stack fintechs’ and the ‘xborder only’ players.

I’m personally excited to see where this space goes. If RBI’s 2028 payment vision is anything to go by (read more in depth about it here), there is a focus on making it easier for cross border players to get authorized (combining PSS and FEMA requirements is one example in the Vision doc). And there are a lot of corridors to build for, from India to the world. Not just for money movement, but also for travel (Scapia - the travel fintech being an example, which raised ~$63M in Series C in May 2026). As an aside, General Catalyst invested in both Scapia and Xflow, so clearly they’re bullish about this space too.

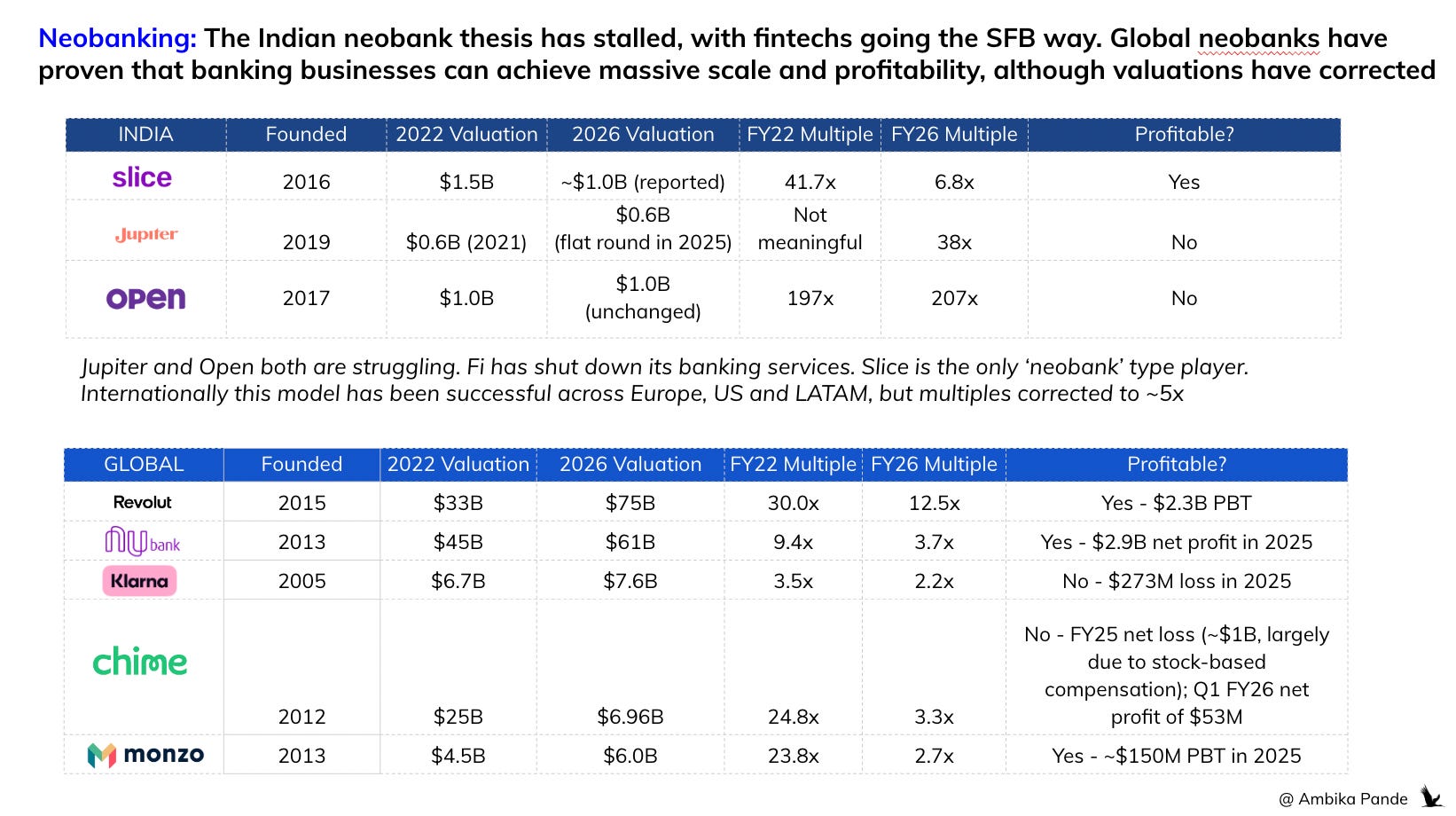

3️⃣ Neobanking: India multiple dropped from ~40x → 6.7x, in the vicinity of global average benchmarks of 5x. SFB investment / merger seems to be the way to go

This only ‘neobanks’ in India seems to be Slice because it merged with North East SFB to form Slice SFB, and of course BharatPe, with 49% stake in Unity SFB. The rest, Fi, Open are struggling, because the RBI does not currently grant standalone banking licenses to digital-only banks or neobanks. In India, the only way to make this work clearly is to merge with a SFB, or to operate as a SFB with a ‘fintech’ mindset. It may be early to say, but Slice in FY26 reported its first year of profitability, of INR 48.6 Cr (~$6M), which is a success story in my book, and hopefully sets the tone for more neo-bank like players. Other SFBs (Shivalik SFB for example which has raised funds from Accel and Quona), could expect either investment, or merger opportunities with fintechs, but that is what I expect for the Indian story.

Globally, this multiple dropped from 18x to 5x, but Slice’s multiple are in the vicinity of what global benchmarks suggest. This also seems to be a profitable business: with Revolut, Nubank, and Monzo all turning over profits in FY25 / FY26.

4️⃣ Lending: India and Global equivalents are both at 6x revenue multiples, and all companies profiled are profitable. This space will continue to attract funding

While in India, the average multiple dropped from 13.2x to 6x, this has actually increased for global companies, from 3x to 6x.

This is a pretty mature segment in India. We’ve seen a few IPO’s already, and others have filed their DRHPs. This is more like ‘tech enabled’ NBFCs. The key: in India, everyone is profitable. Lending clearly is a segment that makes money. And a lot of companies have filed or are filing for IPO’s. Some examples below:

Moneyview: Filed its DRHP in March 2026. Consistently profitable, made INR 250 Cr (annualized) profit in FY26. Valued at $1.6B latest.

KreditBee: Raised $280M in 2026 in pre-IPO funding at a $1.5B valuation. Made INR 478 Cr of profit in FY26.

Fibe: Filed for IPO in June 2026. Made INR114 Cr profit in 2026. Valued at $700M

Snapmint: $187M valuation in 2026. Profitable, made INR 281 Cr in FY26.

Kissht: Valued pre-IPO at ~$340M. IPO’ed in 2026, and is valued at ~$500M - $550M market cap today. Profitable, INR 281.5 Cr in FY26.

Flexiloans: Valued at $140M in 2026. PAT in FY26 of IN 4.1 Cr

The global landscape is more mature, with most of the companies being founded in 2011 and 2012, as compared to 2014 - 2016 in India.

In global companies, what is interesting is that Both Sofi and Affirm started out as lending platforms: connecting borrowers to lenders, but not lending themselves. But in 2022, Sofi got a bank charter, and in January 2026, Affirm applied to become a bank as well. Mirroring what is happening in India. You have to lend yourself.

Lending also seems to be a subset of what neobanks provide.

Klarna, another BNPL start-up which was founded in 2005, became a neobank in 2017. And Nubank, the LATAM neobank used this as a method to strengthen their customer base, they were able to give out credit and credit cards to an underserved base. So globally, it seems like banks are the entity that do most of the lending, and, the evolution is clear: platform distribution → bank → lend on your own books. That is what is happening in India, and what I expect will continue to happen. TSPs will start out as platforms, but eventually go after their own NBFCs. There was also some growth funding in 2025 / 2026 for tech-enabled NBFCs such as Techfino, Stashfin and ZET. And seeing the success, profitability metrics, and scope, I expect more funding to happen here. But the standalone lending TSP game is something that is over, you’re not going to make money unless you’re lending on your own books.

I had written a piece recently, on how, to win in India, you need to be a full stack fintech, lending, or xborder to make money. Seems relevant

![[#88] Do all roads in fintech lead to license aggregation (Part 8): 2 years later, if you're an Indian fintech, you need to be full stack, lend, or go xborder to make money](https://substackcdn.com/image/fetch/$s_!viWB!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F41b90acd-b74b-4721-8bb0-bbbf74e5b339_1790x1012.png)

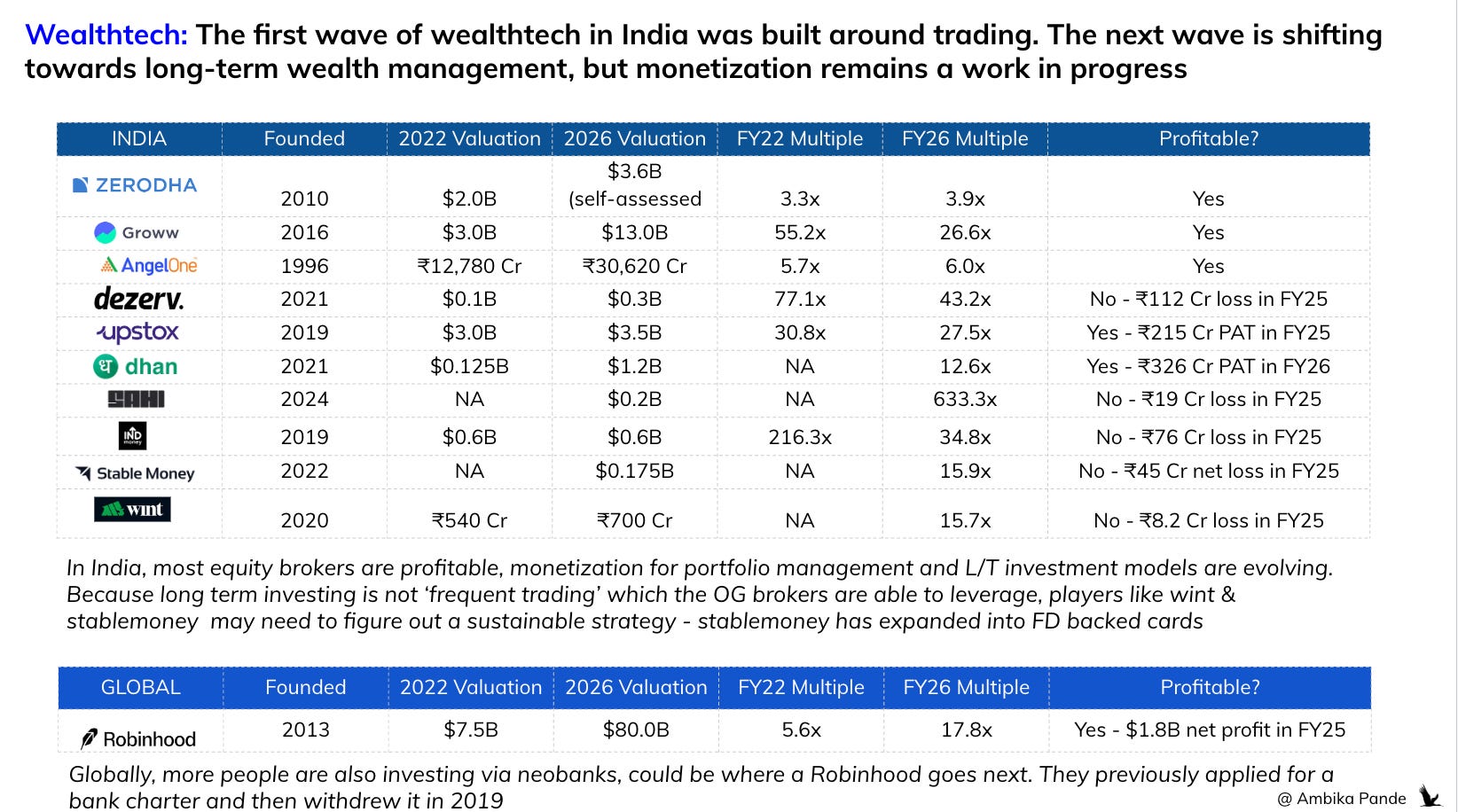

5️⃣ Wealth-tech: India multiple dropped from 35x → 16x. But valuations did increase, clear upside and monetization here, in the broking segment.

Wealth-tech is an interesting space. It’s where, along with lending, I see a lot of funding that has been happening. India wealth-tech valuations have dropped from 35x in 2022 to ~16x in 2026. Everyone who raised, or went public (looking at you Groww), has had their multiple normalized somewhat. What is also interesting is while brokers are making money in this space, ‘wealth management’ services are not.

Profitable brokers → Groww IPO’ed in 2025, Dhan raised in 2026, equity and mutual fund first players are profitable

These all started off as discount stock brokers (Zerodha, Upstox), Groww as a mutual fund distributer, and Dhan as an active trader platform, making money off brokerage fees. Now of course, most have expanded into stock broking, FD distribution, and wealth management. Zerodha and Groww have NBFCs through which they give out loans, most presumable, loans against securities that people take against the securities purchased from their platforms, and their own AMC arm. And in April 2026, Zerodha applied for a merchant banking license which would allow it to provide investment banking and capital markets advisory services, an expansion from its wealth tech focus.

Zerodha: Founded in 2020. The OG. Self assessed valuation at $3.6B, with a revenue of ~$1B (INR 8870 Cr in FY25). The market would probably value this at ~$12 - $15B (12x - 15x), or even higher. Profit of $442M (INR 4200 Cr) in FY25.

Groww: Founded in 2016. IPO’ed in 2025. Was valued at $3B in 2022, and today, post IPO, has a market cap of $13B. However, multiple has dropped, it was valued at 55x in 2022 (~$54M revenue), which has gone to 27x in 2026 ($488M revenue). Profits of $213M (2083 Cr) in FY26. Also a UPI App, with INR 10k Cr volumes transacted via its UPI App in may 2026.

Dhan: Founded in 2021. Raised Series B, $190M in 2025. Profits of $34M in FY25 (INR 326 Cr). FY26 Multiple is ~12.6x.

Upstox: Founded in 2019. Valued at $3.5B in 2025, with its last funding round in 2022. ~ $22M profit in 2025. FY2 multiple is ~27x.

Unprofitable brokers: Stablemoney, Wint Wealth, Sahi raised in 2026, INDMoney in 2025, Sahi is the equity first broker, rest are not.

Stablemoney: It is a broker, but it focuses on fixed deposits mostly, now bonds, and has launched a FD backed card, which according to its website has ~25,000+ users. It raised $25M pre-series C in 2026, at a valuation of $175M. It had revenues of $10M (INR 104.4 Cr in FY25), and had net losses of ~$4M in FY25. It raised in FY26 at a ~15.9x multiple.

Sahi: Founded in 2024. Had a $33M raise, Series B in 2026. Mostly a broker (like Dhan). Raised at a $200M valuation in 2026 (with the founders diluting 60%). Some Some reports say that it is at an ARR of ~$350k in FY26, (Multiple of ~600x, and unprofitable at ~19 Cr loss (~$2M)which suggests either that some serious growth is expected (which is tough in a crowded market, unless they’re able to do what Dhan did, which is identify a niche that was not being served by the market).

INDMoney: Raised $35M, Series D in 2025. Valued at $600M, with revenues of 164 Cr in FY25, and losses of INR 76 Cr. Valuation multiple dropped from 216x in 2022, to ~35x in FY26. INDmoney disclosed that less than 10% of its FY25 revenue came from F&O trading, with the majority driven by long-term investing behavior and recurring financial relationships, so I’d classify it more as a wealth management platform now, and not just broking.

Wint Wealth: Raised a $28M, Series B in 2026. Specializes in corporate bonds and debt securities. Valued at $80M in Fy26, at a multiple of ~15.7x. Revenues of $4.7M, and loss of ~$860k.

And in portfolio management → Dezerv

Dezerv raised $40M, Series C, in 2025. Valued at $300M in 2025, up from a $100M valuation in 2022. Went from a 77x revenue multiple in 2023, to 43x in 2026. $6.7M revenue (INR 66 Cr revenue in FY26), and ~12M loss in FY25. They started out in 2021, with a focus on ‘affluent’ Indians, and then pivoted to ultra HNI’s.

So, brokers, which have a focus on equity first (stocks, MFs, ETFs) are profitable. Like lending and unlike payments, this seems to be a space which has monetization potential. However, the players which are NOT profitable yet are the brokers which are not equity first. I’m assuming 3 reasons:

First, critical mass of volume is still missing, like in the case of Wint Wealth, which has ~300k investors. But could also be a timing thing, Stablemoney was founded in 2022, and Sahi in 2024.

And this makes sense. I’d also assuming the reporting needs to be more precise. Wint Wealth reports registered investors. Stablemoney reports registered users which are ~5M. But Dhan and Groww report active brokerage accounts. Dhan for example has ~1.1M active brokerage accounts. Groww has ~13M active brokerage accounts.

It could also be, despite having critical mass, there is more money to be made on the equities and active trading side, since equity brokers, especially Dhan charge per transaction, while FD’s are more of a ‘buy once and hold’ sort of game.

But it isn’t just Series B and Series C game. There are start-ups raising at pre-seed to Series A

Trackk: Raised $3.7M seed in 2026, investing for GenZ seems to be the pitch, also positioned as #NotYourDaddysInvestmentPlatform. Um. Hope it works.

CREST: Raised $3.1M, pre-seed. Wealth management, with asset allocation, investment oversight, consolidated reporting, tax-efficient structuring, succession and estate planning, governance, philanthropy, real assets, alternatives, and long-term wealth stewardship

PowerUp: Raised $12M, Series A in 2025. Mutual fund advisory.

So, there is funding coming into wealth-tech. Firstly it seems to be a space that has potential to make money (unlike domestic payments). Secondly, active investing for the affluent base is still an open problem that has not been completely been solved. And finally, Indian investors are looking beyond just Indian equities as rising wealth, understanding about this space, the rupee depreciation, and the demand for exposure to global technology companies (AI, need I say more), will drive interest in cross-border investing. And I expect it to become table stakes for existing players.

![[#61] The Next Wave in Wealth Management: Acquisitions, niche TGs & consolidated net worth](https://substackcdn.com/image/fetch/$s_!D5-U!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F943e6ab4-1a60-4fef-baf6-465ed60b4ecc_1574x890.png)

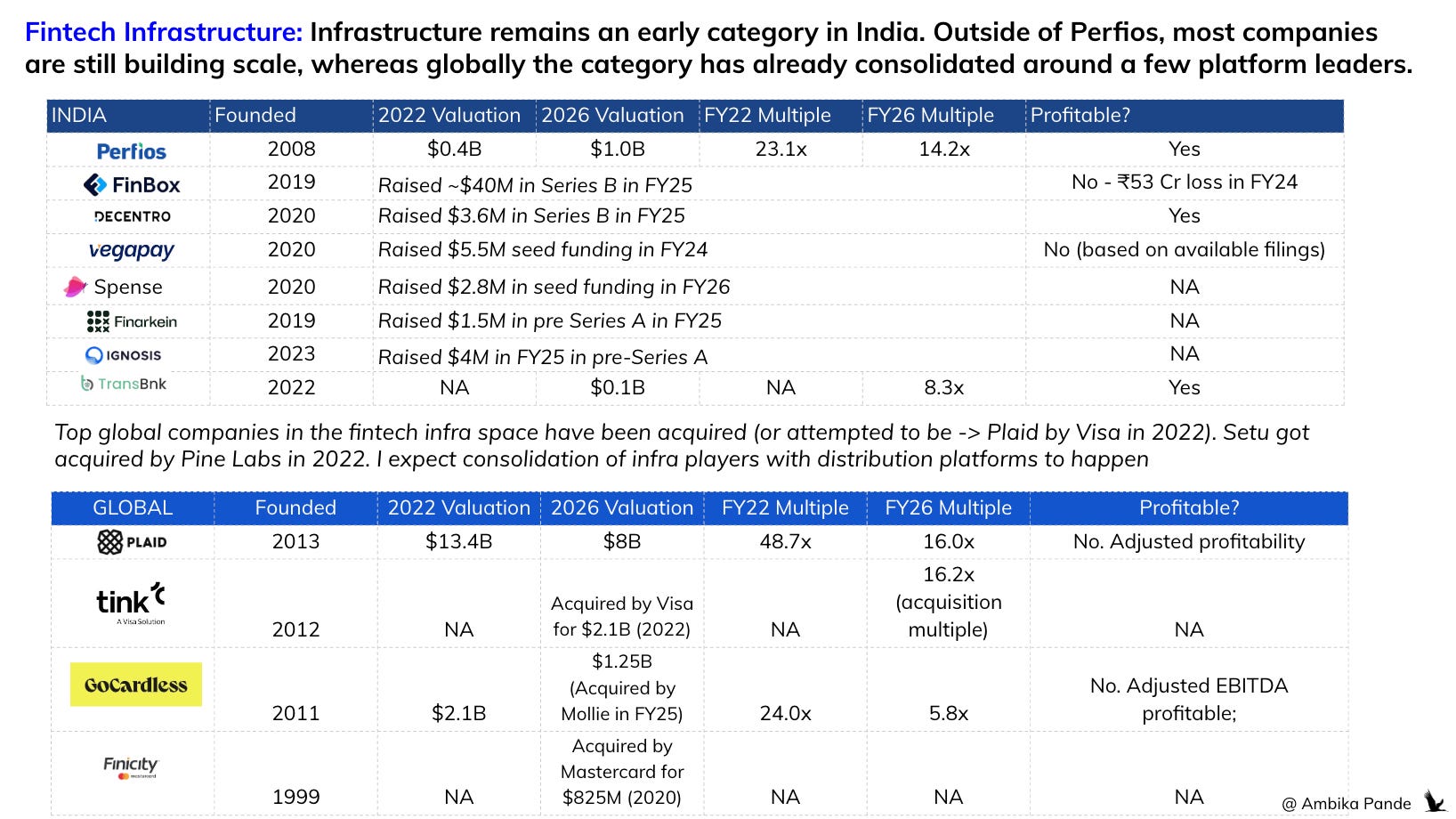

6️⃣ Indian fintech infrastructure plays: Perfios multiple has dropped from 23x in FY22 to 14x in FY26. On par with global infrastructure players such as Plaid and Tink, which are at ~16x. The consolidation play in fintech infra is very real

I’d define fintech infrastructure companies provide the underlying technology, APIs, and services that power financial products behind the scenes. While consumers may never interact with them directly, they enable many of the apps and financial institutions they use every day. An example is: Setu → Its BBPS stack, and Account Aggregator TSP stack is what enables apps like Cred for example accept bill payments, and other apps pull customer financial data. I’ve kept this section pretty broad, this can be any infrastructure: credit underwriting, analytics, collections and banking infrastructure like LOS and LMS systems. Of course, these days the buzzword is ‘AI native.’ In fact, even ‘AI agents’ is something I’d put in under infra

The consolidation angle here is very strong. And I’ll take inspiration from Plaid, Tink, GoCardless and Fincity. All were open finance infra players, aka building APIs that allowed consumers to pull their data into 3rd party consumer apps (behind consent). And 3 out of them were acquired.

Plaid is an open banking platform founded in 2013: It actually got an acquisition offer from Visa in 2021, for $5.3B (this was ~20x multiple at 2022 revenues). This was blocked by U.S. Department of Justice (DOJ) which filed an antitrust lawsuit to block the deal. That didn’t happen, its valuation dropped to FY2025 to ~$6.1B, and now it raised again in 2026 at a valuation of $8B. Its multiple dropped from 48.7x 2022 to ~16x in 2026. It isn’t profitable yet, but seems to be approaching profitability

Tink: Tink is an open banking platform founded in Sweden in 2012. It was acquired by Visa in 2022 for ~$2.1B (this was at FY22 revenues of ~$130M, so a multiple of ~16x).

GoCardless: Founded in 2011 in London. It is an infrastructure platform that specialized in open banking APIs, and account to account payment initiation. It was acquired by Dutch payments player Mollie in 2025 for ~$1.25B, at a valuation multiple of 5.8x. This dropped from their 2022 multiple of 22x, and valuation of $2.1B. They’re not profitable yet (except on an ‘adjusted basis.’)

Finicity: Founded in 1997. It’s an open banking and financial data aggregator platform. It was acquired by Mastercard in 2020 for $825M.

So, US, Europe and global players, despite each probably processing $ billions in actual value of transactions powered, still ended up being acquired. I’m not sure how the India story will play out, but consolidation seems like a good prediction. Setu got acquired by Pinelabs in 2022. Poweredge Analytics, a card management start-up founded in 2022, got acquired by Signzy (identity and KYC start-up) in 2025.

While the India infra story is quite early, standalone infra players will find it tough to scale. Even existing full stack players with infra offerings are expanding overseas → Pine Labs built Credit+, and is now expanding into the Middle East, SE Asia, and rolling out a stablecoin offering

There are a lot of players who exist here today. Some examples:

Credit Infra players: Finbox (raised $40M Series B in 2025), Finarkein (raised $1.5M pre-Series A in 2025), Ignosis (Raised $4M in FY25 in pre series A). I’d actually also put standalone Account Aggregators here as well. I expect international expansion here to happen. Finbox in fact raised for two things, among other: international expansion, and potential acquisitions.

Bank infrastructure players: Players building infrastructure for banks, like card management. Examples are Vegapay (Raised $5.5M in 2024), Spense (Raised $2.8M seed funding in FY26).

API first players: Transbnk (APIs for corporate banking → if you’re a business, you may be using different banks for different services, which can become tough to manage. Transbnk ($25M Series B in FY25) is able to provide a unified banking layer with its APIs. Decentro (Raised $3.6M in Series B in FY25) is one API for multiple financial services.

The India market may not be big enough to operate in standalone as a pure infra player. Acquisition, or international expansion will have to happen.

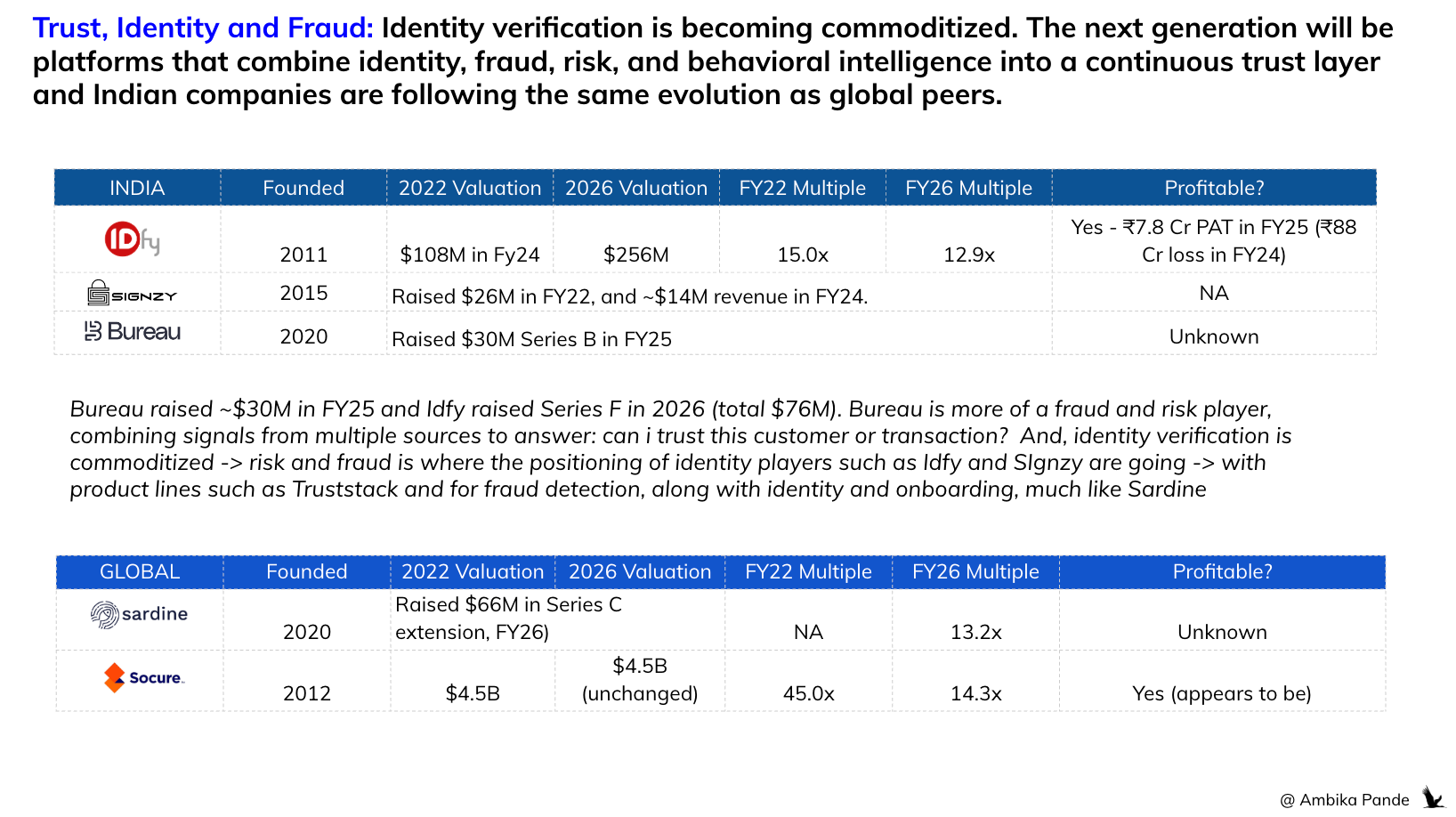

7️⃣ The last category I’ve looked at is Trust, Safety and Fraud. Identity verification is becoming commoditized. The next generation will be platforms that combine identity, fraud, risk, and behavioral intelligence into a continuous trust layer and Indian companies are following the same evolution as global peers.

To be fair, this is fundamentally an infrastructure business, it sits adjacent to fintech infrastructure and has evolved into a distinct category of its own, and hence I’ve clubbed it differently. It’s a little broad, but any player that looks at things like KYC, identity, and core fraud detection, device intelligence etc are players I’ve classified here.

A lot of identity and KYC companies have expanded their offerings from just providing identity verification and customer onboarding into fraud as well. A great example is Idfy.

Idfy started out as a background verification company, and when India’s DPI stack was rolled out for identity, such as Aadhaar, eKYC, DigiLocker, GST, Idfy built these into developer APIs. Then they expanded beyond identity, into OCR, liveliness checks, video KYC, and fraud detection. That is when their positioning changed, in 2024 - 2025, where they went from just customer onboarding and verification, and launched their ‘TrustStack.’ An example is OneRisk, is IDfy’s fraud and risk engine, which uses thousands of data points, from criminal records to financial behaviour, to catch threats early.

Same with Signzy, while it may have started out as an identity / onboarding platform, its product stack now also includes modules for fraud detection. Products such as Transaction Monitoring, for detecting suspicious transactions in real time, and Mule Shield, for preventing mule account fraud, are now part of their stack.

Which makes sense. Any time you’re involved in onboarding a customer, or verifying their data, at its core, what you’re trying to answer is, is this customer real or a fraud, and can I trust them.

Similiar to the core fintech infrastructure category, international expansion and consolidation will have to happen here. That’s what existing players have already started doing.

Idfy: Founded in 2011. Valued at $256M in FY26. Raised its Series F in 2026, picking up ~$53M in February, and $23M in June. Revenues of ~$20M in FY26 (INR 188.5 Cr). Multiple dropped from ~15x in FY22 to ~12x in FY26. It’s profitable, turning profits of ~$825k (INR 7.6 Cr) in FY25.

Signzy: Founded in 2015. Raised ~$26M in 2022. Valuation unknown, but it had revenues of ~$14M in FY24 (INR 111 Cr), so I’m assuming it’s revenue is in and around ~$150 - $250M, keeping Idfy as a benchmark.

Surepass: Founded in 2019. Bootstrapped, and not to many details around its financial or valuation.

Bureau: Founded in 2020. Fundamentally different from the top 3 start-ups, which all have overlapping products, the key being onboarding and identity verification APIs. Bureau primarily started out as a fraud and risk monitoring play. Couldn’t find details around its revenue and valuation, but it raised $30M Series B in FY25. Assuming atleast 15-20% dilution, this would bring valuation to ~$150 - $200M.

Global benchmarks that I have compared against is Sardine and Socure

Sardine is a risk and fraud intelligence platform, trying to answer the question: is this customer, or this transaction fraudulent (using indicators such as device intelligence, behavioural fraud, risk scoring basis internal models, AML monitoring and chargeback fraud). Similar to Bureau in that sense. Sardine was also founded in 2020. In May 2026, it raised a Series C extension round of $25M, bringing its valuation to $660M.

Socure is another. It positions itself as an identity and fraud player. It last raised in 2021, with its Series E round, raising $450M as a ~$4.5B valuation, which is unchanged as of 2026. And with revenue of ~$315M in FY25, this brings its FY25 multiple to ~14.3x.

Rather than buying separate solutions for identity, KYC, fraud, AML, and device intelligence, customers will increasingly prefer integrated trust platforms. Identity verification is becoming commoditized, and the real differentiation will come from combining identity, fraud detection, device intelligence, and behavioral signals, (probably with some AI / agentic layer on top) into a single platform that continuously evaluates trust throughout the customer lifecycle.

The same trend is playing out across every category: from standalone products to full-stack platforms. From point solutions to owning the customer relationship.

Payments: Payment gateways → payment operating systems, spanning online and offline acceptance, B2B and B2C payments, issuing, lending, and financial infrastructure.

Wealth: Single-product apps → wealth platforms, expanding from equities or fixed deposits into multi-asset investing, lending against assets, retirement, and international investing.

Infrastructure: Individual APIs → integrated infrastructure platforms, increasingly combining payments, banking, lending, analytics, and compliance.

Trust: Identity verification → continuous trust platforms, combining identity, fraud detection, device intelligence, risk, and behavioral signals throughout the customer lifecycle.

The other shift is equally important. The “India premium” that once existed has largely disappeared.

Indian fintech companies are no longer being valued simply because they’re building for a large market. They’re being valued on the same metrics as their global peers: revenue quality, profitability, product depth, monetization opportunity, and the ability to compound over time.

I don’t think that’s a negative. It marks the end of the hope premium and the beginning of something healthier. The benchmark is no longer to be the best fintech company in India, it is to build a company that can stand alongside the best fintech companies in the world.

That’s ultimately what this re-rating represents. Not a reduction in ambition, but a rather, a reset in expectations. The next generation of Indian fintech companies won’t earn a premium for where they’re built, but by building businesses that deserve one.

Shoutout to Yogendra Sankhala for working with me on this. He’s a BITS Pilani Goa alumnus. and currently, a Software Engineer at Silence Laboratories, building privacy-preserving cryptographic systems and secure infrastructure for digital identity, authentication, and AI agents.