[#85] The future of fintech in India: RBI has a vision for payments per its 2028 vision document. Just not for the companies building it

RBI's 2028 vision focuses on fraud liability, MSME financing, and xborder friction. But limited monetization in payments, and the RBI strategy to compete against private fintechs is not addressed

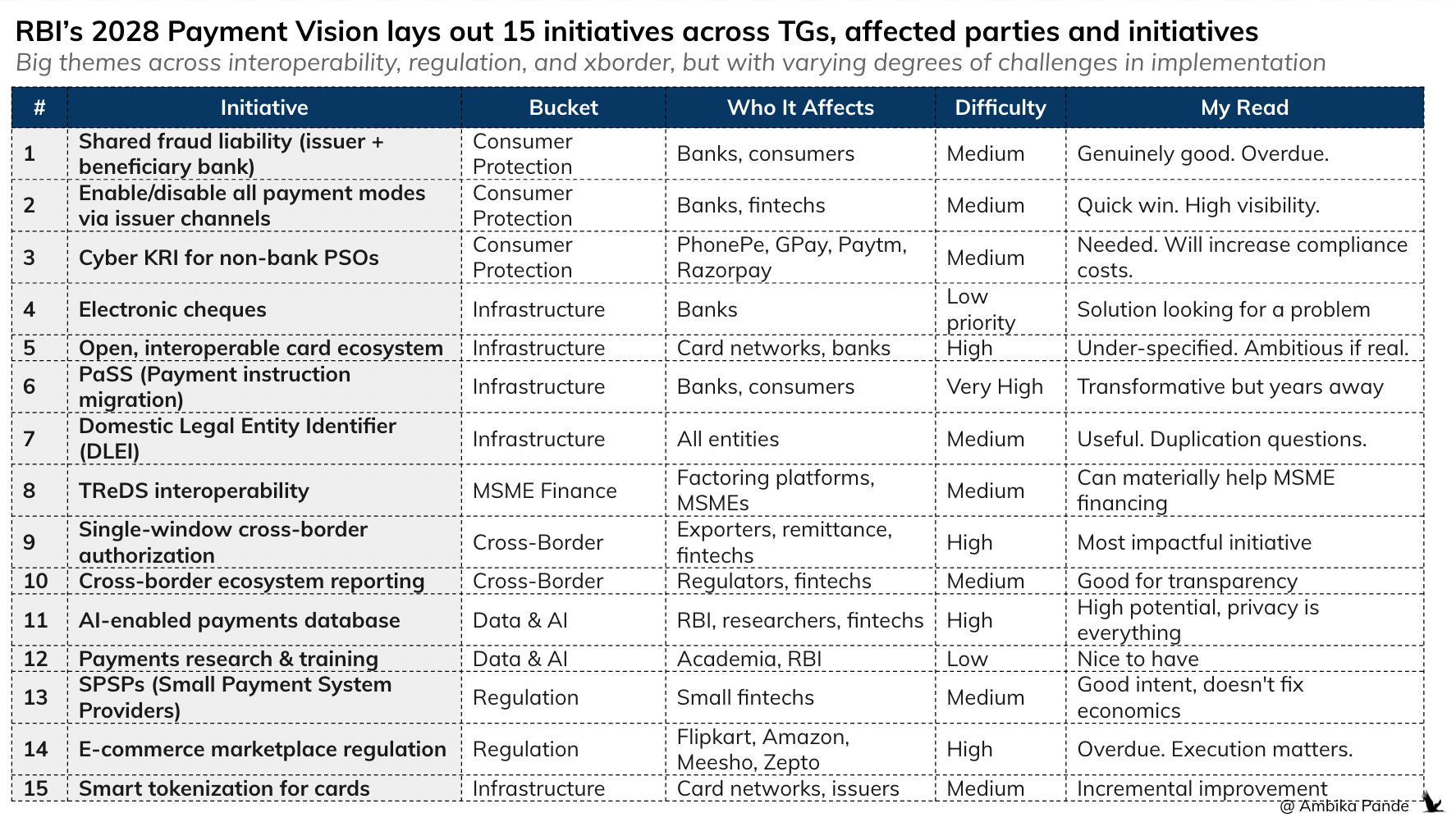

Over the last few weeks, RBI quietly dropped its Payments Vision 2028, which is a 15-initiative, 3 year roadmap themed “Shaping India’s Payment Frontier.” It covered a lot, from fraud liability changes, cross-border simplification, an AI-enabled payments database, and, maybe the most interesting bit - a signal that e-commerce platforms might come under direct RBI regulation.

However, what was also interesting to note was the things it did NOT mention: which is how running a payments business, especially as a ‘start-up’ means that the odds are always stacked against you, because monetization happens on volumes, not margins. This is something I had covered in article below:

[#77] The future of fintech in India: How do we approach monetization in the age of DPI?

![[#77] The future of fintech in India: How do we approach monetization in the age of DPI?](https://substackcdn.com/image/fetch/$s_!uEuO!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9acc84e9-091e-467a-801b-26760781c1f3_1694x966.png)

As India’s Digital Public Infrastructure (DPI) stack expands, we’re seeing open rails emerge across nearly every fintech and fintech-adjacent category, payments (UPI, BBPS), identity (Aadhaar, eKYC), data sharing (AA), e-commerce (ONDC), and now lending (ULI). This is an unprecedented moment: few countries have built such a comprehensive digital foundat…

On the surface, it reads well. Trust, resilience, global reach. All the right words.

But here’s what I was really looking for. A few months ago, in the article above, I wrote about the structural squeeze on Indian fintechs - free DPI compressing margins, standalone TSPs disappearing, the license requirements constraining innovation, even in smaller fintechs, full-stack conglomeration as the only survival strategy. The question I ended with: does free DPI unlock innovation, or constrain it by eliminating economic incentives? So when the regulator releases a vision document for payments, the next three years, the first thing I’m checking: does it address any of what I flagged?

Some of it, yes. Most of it, no. And there’s a whole world - agentic payments, stablecoins, monetization, that I’ve been covering in in past articles, that RBI doesn’t even acknowledge exists.

I think what we do really well, especially from a central / governance perspective is “project” that we’re thinking about the future. What we don’t do well, is defining steps on how to implement some of these things. Which, if you think about, is the most important.

“Payments Vision 2028 recognises that digital payments continue to make inroads into all population segments (a fact objectively captured through RBI’s Digital Payments Index), and the challenge before the ecosystem is no longer one of expansion of reach alone, but of deepening ‘trust’ in payment systems, reinforcing resilience and expanding their global footprint. Anchored in the theme, ‘Shaping India’s Payment Frontier’, this Vision document focuses on user empowerment, safeguards against fraud, efficiency of cross-border payment frameworks and promoting ease of doing business. Regulations and supervision of payments systems, while continuing to be risk-based, would be guided by the need for innovation and inclusion.” - an excerpt directly from the Payments Vision 2028 document that RBI published.

Reads well. But let’s get into it in detail. What I’ve tried to do is go through the doc, which isn’t that long by the way, so I do recommend reading it for yourself. But I’ve tried to map it out into what the initiative is, and what the impact of this could be.

A pattern you’ll notice when you read the paper for yourself: a lot of “examine,” “explore,” and “review” in the language. Very few hard timelines. Very few measurable benchmarks. To sort of compare this to other themes I’ve been talking about - and what is top of mind for me is agentic commerce, I’ve talked about how the real bottleneck for agentic commerce isn’t protocols, it’s about the infrastructure readiness of real stakeholders who are actually involved in the money movement (card networks, banks, etc), which is something that is echoed in Adyen’s whitepaper about agentic commerce, and there is no clarity on that. However, that can be forgiven - very new market, and the whole “agentic” spiel has only been around for the last 2-3 years.

But my concern is that even when you’re talking about payments, and payments fintechs, which are 10-12 years old in India, you probably need a little more clarity and starting pushing on real implementation and “hard” timelines, not just “explore” and come back.

This is what I respected about the RBI circular on alternate authentication, which - if you recall mandated for 2FA in payments (which already exists), but one of the factors needing to be dynamic in nature (like an OTP, or authenticator apps), AND coupled with the fact that the overall view is to move away from OTPs, leads to a lot of interesting changes in the ecosystem. For example: if you’re on linkedin, you’ve probably seen how everyone is launching biometric based payments on checkout, utilizing biometric creds, and passkeys. That is because it’s been pretty obvious that the ask is to move away from OTPs.

Now, getting into the specifics.

What seems to be positive

Let me be fair first. There are things in this document that matter.

1. Fraud liability is finally shared between the issuer and beneficiary bank - shared incentives can add more scrutiny

❓The problem today: Today, if you get scammed via UPI, here’s what happens: your bank says “you authorized it, not our problem.” The beneficiary bank which is the the bank that received the stolen money has zero accountability. They have no incentive to flag suspicious accounts, freeze funds quickly, or cooperate in recovery.

✅ Solution: RBI is proposing to change this. Shared liability between the issuer bank (your bank) and the beneficiary bank (the scammer’s bank). Both are now on the hook. This is meaningful. UPI fraud surged to INR 1,226 crore in FY26. A big chunk of this could be prevented if beneficiary banks had skin in the game, with flagging mule accounts, freezing suspicious inflows, cooperating faster on recovery. Now, it is good that there are more stakeholders in the ecosystem that have a liability - it ensures that everyone is aligned, otherwise if there only one party in the transaction that is on the hook for this, it makes cooperation a lot harder.

👉 But my concern: This needs rule-based design. How exactly is liability managed? 50-50? Based on response time? Based on who flagged first? If the rules are vague, it could actually slow down relief rather than speed it up.

2. Cross-border is getting serious attention

❓The big problem today Today, if you’re building cross-border payment infrastructure, you need separate approvals under separate acts, from separate departments. It’s a nightmare. I’ll elaborate on this.

PSS Payment Systems and Settlements Act governs all entities, and mechanisms that operate a payment system in India. In a nutshell, if money moves domestically in India, then PSS governs the rails and operators, and so, a cross border payments platform first would need to have an authorization under PSS. So, methods such as UPI, RTGS, Netbanking, and players such as Banks, Payment Aggregators, UPI Apps would all be governed under this act.

FEMA (Foreign Exchange Management Act) Regulates cross-border flow of money and foreign exchange in and out of India.

An example: A cross-border payment app (say, Wise) would need PSS authorization for operating a payment system in India and FEMA compliance for the forex/remittance leg. That’s just unnecessary hiccups.

✅ Solution: RBI has proposed a single-window authorization combining PSS Act (2007) and FEMA (1999) requirements. So, for any cross border entity, now instead of having to get authorized under two separate Acts, this will be combined into one.

Other things that RBI covered under cross border are: 1) Dedicated reporting, which is tracking domestic trends and global developments separately and 2) G20 alignment, where efficiency metrics benchmarked to global standards. Now, the jury is still out on what this means since these 2 points mean that we’ll benchmark our products to global standards.

👉 However, my concern is that nowhere are stablecoins mentioned: I’ve spent the last several months writing about how stablecoins are becoming the default rail for cross border and machine payments. What surprised me that RBI doesn’t mention stablecoins once in this document, seeing that stablecoins are becoming the rails on which cross border money movement will happen. (more on this below).

But nevertheless, less regulatory friction for cross-border flows is unambiguously good. This is the one area where RBI is actively trying to reduce friction rather than add infrastructure. I’ll take it.

3. TReDS interoperability for MSMEs

Firstly, why should we care about TReDs? Well, TReDs sees significant volumes, with invoices processed totalling INR 1.38 lakh crore in FY 2023–24, marking an 80% increase over the previous year. And of early 2026, leading platforms are projecting over INR 1.75 lakh crore in annual transactions, so its a big channel for MSME’s to manage their cashflows, and what RBI is clearly betting on to drive the growth of the MSME sector.

Before, we get into this, let us quickly understand what TReDs is:

TReDS is an electronic platform where MSMEs can sell their trade receivables (invoices) to financiers at a discount, to get paid early instead of waiting 30-90-180 days for the buyer to pay. It is NOT a loan, where there is a loan you’re getting

Think of it as: an auction marketplace for unpaid invoices. I’ll give an example:

Let’s say there is a MSME (Acme Corp) that supplies goods to some Corporation (Corp X) and has raised an invoice of INR 10L. Acme Corp will receive payment in 90 days from Corp X.

But the problem is that MSME needs cash NOW to pay workers, buy raw materials, and just continue with business operations. They’re stuck until payment comes in.

TReDS essentially fixes this cash flow gap. MSME’s can upload invoices on TReDs platforms, the Corporation validates it, NBFCs / Banks and bid on the invoice. Whoever offers the MSME the best deal wins. So let us say NBFC X wins the bid, and offers the MSME 9.9L. The MSME gets INR 9.9L immediately and can continue operations. And the corporation pays NBFC X INT 10L in 90 days when the invoice comes due, making INR 10k.

❓The problem today: The problem: these platforms operate in silos. Each one has its own pool of buyers and sellers. So if you’re onboarding on TReDs platform A today, it’s a closed marketplace, where you’ll only be able to find financiers, if they’re onboarded on the same marketplace.

✅ The solution: RBI wants to improve the access that MSME’s get to working capital by proposing the following:

Interoperability across TReDS platforms: Honestly? Usually when anything comes up around interoperability I always get cagey. My big concern around interoperability has always been that this takes away from the key moat of any tech business. If you suddenly start making all this interoperable, then it reduces the margins and the moat that these businesses have. However, the reason that I see this as a “not necessarily something bad” is mainly because there aren’t that many TReDs platforms in India, only ~5 licenses have been given out. RXIL (backed by SIDBI (govt) and NSE (exchange), Invoicemart (Axis Bank + mjunction (Tata Steel & SAIL JV), M1xchange ( promoter-led - Mynd Solutions). Has raised some private capital but not classic VC-funded. C2FO Factoring solutuionsm and then KredX is which is promoter-backed. The point is, this works if there are few companies operating in this space. It doesn’t work if it becomes like ONDC - where everyone can plug into this network, and bigger entities which have put the effort to create their networks then essentially have to give access to it to all newer, smaller players.

Expanding access to export MSME receivables: Right now, TReDs mostly supports domestic invoices. Where, an Indian supplier, suppliers to an Indian company, and gets paid by an Indian lender. But now, RBI is proposed to also “explore” frameworks where an Indian manufacturer which exports goods also has a way to sell invoices.

Enabling factoring with recourse: This is more to do with who bears the risk if the buyer doesn’t pay the invoice. In the earlier example, we used Corp X which has an invoice payable in 90 days. This invoice has been sold to a NBFC. Now if Corp X doesn’t pay the NBFC, who bears the risk? In the earlier structure, this was “without recourse.” Which meant that the financier bore the full risk. Which led to them being SUPER risk averse, and being very careful about which invoices to fund, which resulted in many smaller or “riskier” MSME’s not getting access to capital. With recourse means means that here, the MSME is responsible for paying back the financier if the buyer doesn’t pay. Now, on the surface, this seems like a hit to the MSME - but I actually see this as a good thing. MSME’s may take the hit if some buyers don’t pay, but this actually derisks the financier, and makes THEM more willing to take the risk and fund more MSME’s if their downside is covered.

👉 My concerns: There are lots of good things here. This connects directly to the export factoring problem. Forex costs have been killing factor margins on SME invoices - the double conversion problem where USD gets force-converted to INR and then back. If TReDS platforms interoperate AND the FEMA foreign currency account unlock (October 2025) holds, the addressable market for export factoring grows significantly. More platforms, more buyers, more liquidity, better pricing for MSMEs. But my concerns: a lot of this is “being explored.” I don’t know what that means. At this stage, if a regulator has little clarity, then how much will be implemented.

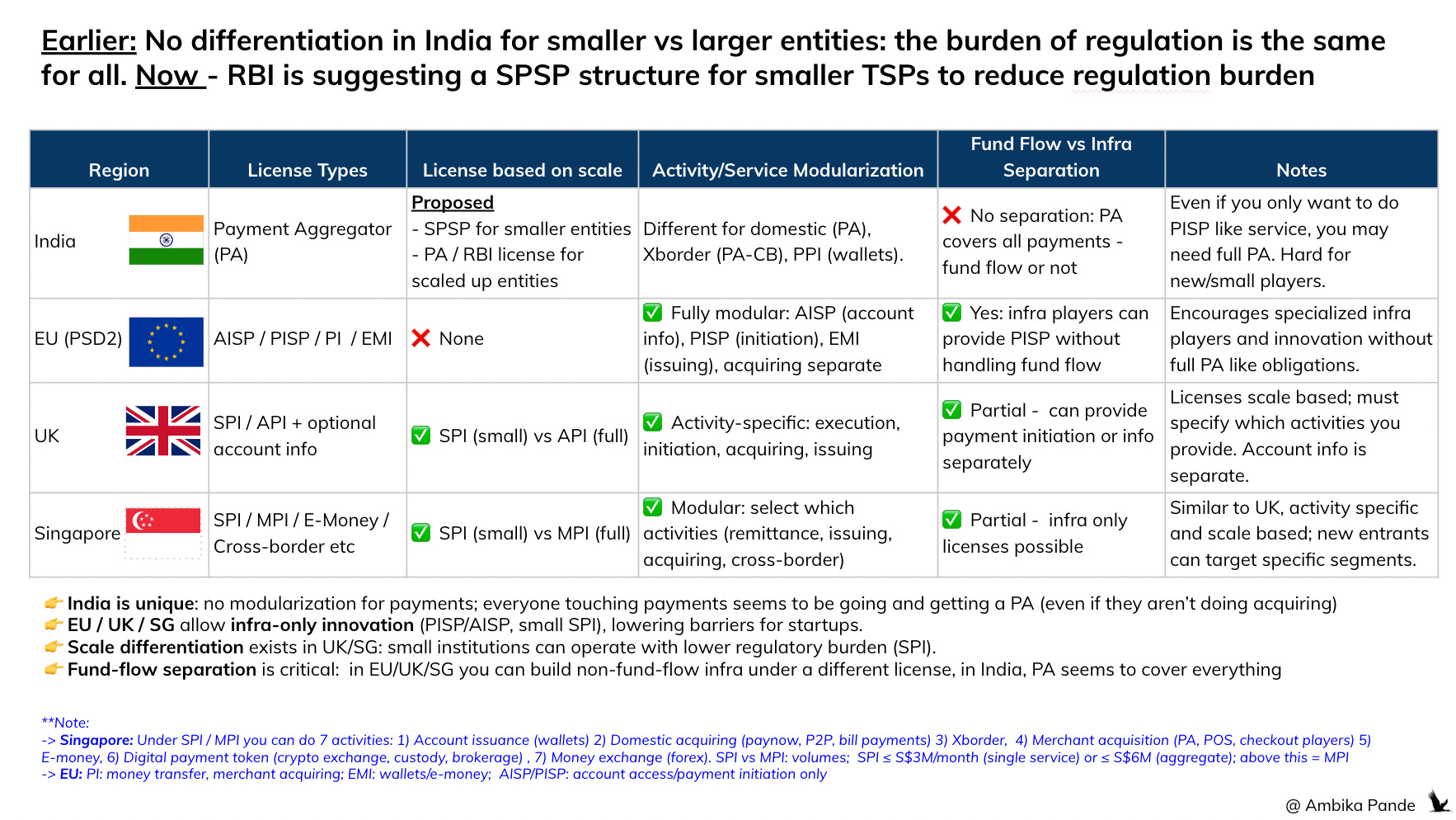

4. Small Payment System Providers - a door for smaller fintechs to operate without taking the “full” compliance burden that a scaled up payment system adheres to

❓The problem today: I’ve actually talked about this in previous articles. While in 2025, with India’s updated Payment Aggregator guidelines moved to a one licence regime in payments - but functionally segmented by flow type and risk profile. Which is: one umbrella PA license, and then individual applications underneath it depending on where the entity wants to operate: online, offline, cross border import, cross border export.

This “umbrella license” policy is similar to other regions I looked at: Singapore, EU, and the UK, which usually have one overall license, and some sub segments underneath the. However, what is different from India and other regions is also stark.

There is no license separation between infra and actual fund flow, which results in everyone going after the same umbrella PA license in India, despite having no play in money movement. Example: even if you are NOT involved in fund flow, but just in payment initiation (think, a payment orchestrator, or even a UPI app), you would still need to probably get a PA license. This severely hits smaller fintechs which may never be involved in fund flow.

There is no compliance reduction based on entity scale in India: Compare this to entities in UK and Singapore. For newer / smaller entities operating at a smaller scale (details here), the license is different, and the compliance and reporting burden is lesser, allowing space for smaller players to come in and compete. In Singapore, MAS offers a Major Payment Institution license and a Standard Payment Institution license, so even small players can operate under regulation without the full compliance burden. And SPI & MPI is differentiated basis the scale they have: volumes: SPI ≤ S$3M/month (single service) or ≤ S$6M (aggregate); above this = MPI. SPI’s & MPIs can conduct the same activitie

✅ The solution: RBI is proposing a new category: Small Payment System Providers, with a perpetual regulatory sandbox. Lower entry barriers. Lighter compliance. A way for smaller players to operate while figuring out full licensing.

So, this is really good from the “regulatory” side of things. The regulatory declarations that a Pine Labs or a Razorpay which are processing hundreds of $billions are at a different scale. A small - just starting out fintech wanting to innovate on money movement should not have to adhere to the same regulatory requirements. They to do - which adds costs, overhead, and makes it hard to operate. And this is in line with what UK and Singapore have currently, so there are precedents for this.

👉 My concerns: I’ve argued in the past that standalone TSPs are being squeezed out of the market - the Signzy-PowerEdge acquisition was Exhibit A. Others: Razorpay buying a stake in Pop, PayU acquiring Mindgate (UPI switch) are all symptons of this. Even profitable, funded startups are getting absorbed because the economics of operating independently in India’s fintech market are brutal. SPSPs are RBI’s answer to the entry problem. And the fact that they have addressed this entry problem means that somewhere, someone has recognized that it is tough to operate as a small fintech player in India. But the entry barrier was never the JUST the license, it was the economics. Giving someone a license to enter a market with zero margins is still a market with zero margins. And that is something that is glaringly absent from the 2028 payments vision.

The Big Moves: Payments Data & E-Commerce Regulation

Two initiatives deserve their own section because they could reshape the market.

1. The AI-Enabled Payments Database

RBI wants to build an “AI-queryable payments data repository” for policy intelligence and supervision. On the surface, this sounds like a data nerd’s dream - a centralized, structured, AI-accessible database of India’s payments flows.

Practically there is still a lot that need to be done here: at the end of the day, a central structured AI accessible database of India’s payment flows has 2 problems:

Setting up a system like this for payments data requires standardization of data schemas: today every system will probably store and report their data separately. So there needs to be a clear plan on what this database will contain, and how it will be standardized so all the data from different sources is speaking the same language

How are you going to get big payment players to share their data? They have enough volumes to draw pretty decent inferences from it. And this is a moat for them: example; Stripe Radar uses the transactional data it has across all its merchants to match trends, and monitor risk and fraud, since it seems patterns across billions of transactions.

Who gets access? At what granularity? Is this consent-based (like Account Aggregator) or surveillance-grade? Will this be used for innovation or just for supervision? RBI hasn’t clarified.

More data is always better. But this is the same issue that we’ve come across in other payments models and initiatives that has been taken at a central level in India - there is a vision to provide a “greater good” to the ecosystem, at the cost of the major stakeholders in it. If designed well, this could become India’s version of open payments data. Researchers get better signal. Lenders build better risk models. NBFCs price credit more accurately. Policy becomes genuinely data driven instead of vibes-driven.

The problem with setting up these ‘grand visions’ of public infra is 1) execution is a question and 2) when there is monetization / comp designed, then its just strong-arming.

If this becomes another free public good, where payments data available to everyone, then further compresses the moat for companies that built proprietary payments intelligence. Companies that spent years building data advantages on payment flows could see that advantage evaporate overnight. So now, there is more free infrastructure, and less monetizable opportunities. This is the DPI playbook, applied to data.

👉 When this happens, then no one is incentivized to ACTUALLY make this work. Stakeholders do the bare minimum needed to “comply” with the mandate. The way I see this: firstly, execution of this is going to be a question, because I’m not even sure if the framework of this has been thought through. The second: if we don’t start thinking of this in terms of a sustainable business model, this is going to turn into something like CKYC - the right idea, but lack of incentives and “thinking” through the process results in rejection rates as high as 30-50%!

2. E-Commerce Companies could maybe come under RBI regulation because of the payments being processed through them

RBI explicitly says it will examine extending “direct regulation” to e-commerce marketplaces and centralized platforms.

The exact quote from the vision document: “E-commerce marketplaces and centralised platforms have been assuming significant responsibilities that could have implications on orderly functioning of the payments ecosystem.”

I’ve actually covered this in a previous article where I explore how lots of ecomm players are moving into fintech. You can check it out below:

[#66] E-commerce to fintech: A proven path. Fintech to e-commerce: Still a question

![[#66] E-commerce to fintech: A proven path. Fintech to e-commerce: Still a question](https://substackcdn.com/image/fetch/$s_!oTeq!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa10e830e-ce48-4e67-a504-3293d312fd00_1924x1084.png)

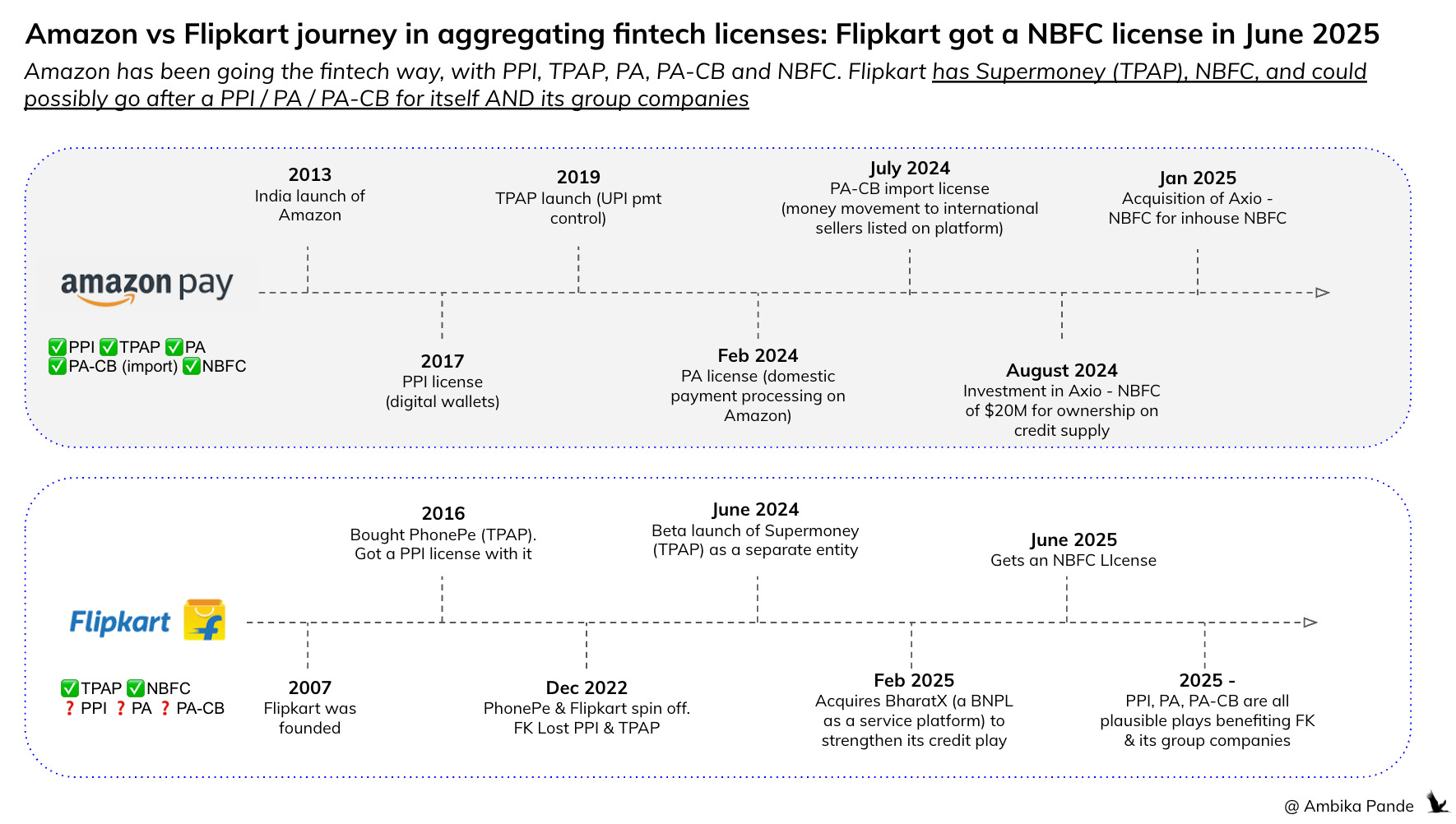

Something interesting but not entirely surprising happened this week (June 2025): Flipkart secured an NBFC license.

Now, from an ecommerce perspective, getting into fintech makes perfect sense.

High volumes = big upside: Even a few basis points saved on massive GMV translates into significant absolute gains.

Own the full CX: Checkout and payments are critical to the user journey. Why let a third party control that experience?

Credit as a VAS: With millions of transacting users, offering embedded credit is a natural and high-value extension.

In short: Fintech isn’t just adjacent for ecomm it’s a logical, margin-boosting next step. The numbers back this up. In February 2026 alone, online marketplaces processed 114.52 million UPI transactions worth INR 6,461 crore. These platforms handle settlement, refunds, escrow, merchant payouts.

👉 But here’s my take on it: I don’t know if this requires RBI oversight. For those players who are getting into this space: Amazon, Flipkart etc, they have already picked up the licenses that they need to.

My prediction: This was that along with Flipkart, Amazon, players such as Meesho, Blinkit, Instamart, Zepto will also want to own more of the payments and money movement step. But they’ll do that via third parties, and some whitelabeled experience (like the Zepto x Snapmint collab to launch Pay in 3 on Zepto). Snapmint is a licensed NBFC that is doing this for Zepto. So this licensing is already being taken care of.

👉 My concerns: Bringing ecommerce players under the regulatory ambit of RBI may not solve anything except for added overhead on everyone.

There’s a difference between “regulate platforms that handle money” (good) and “create compliance overhead that kills quick commerce and small sellers” (bad).

The elephant in the room: What’s NOT in the document

Alright. Now for the part I was really looking for. A lot of times, the ‘absence’ of something speaks louder than what is actually mentioned. And there are some omissions in this vision document that are a bit concerning to me.

The most important: Does RBI address the structural squeeze on fintechs? No it doesn’t

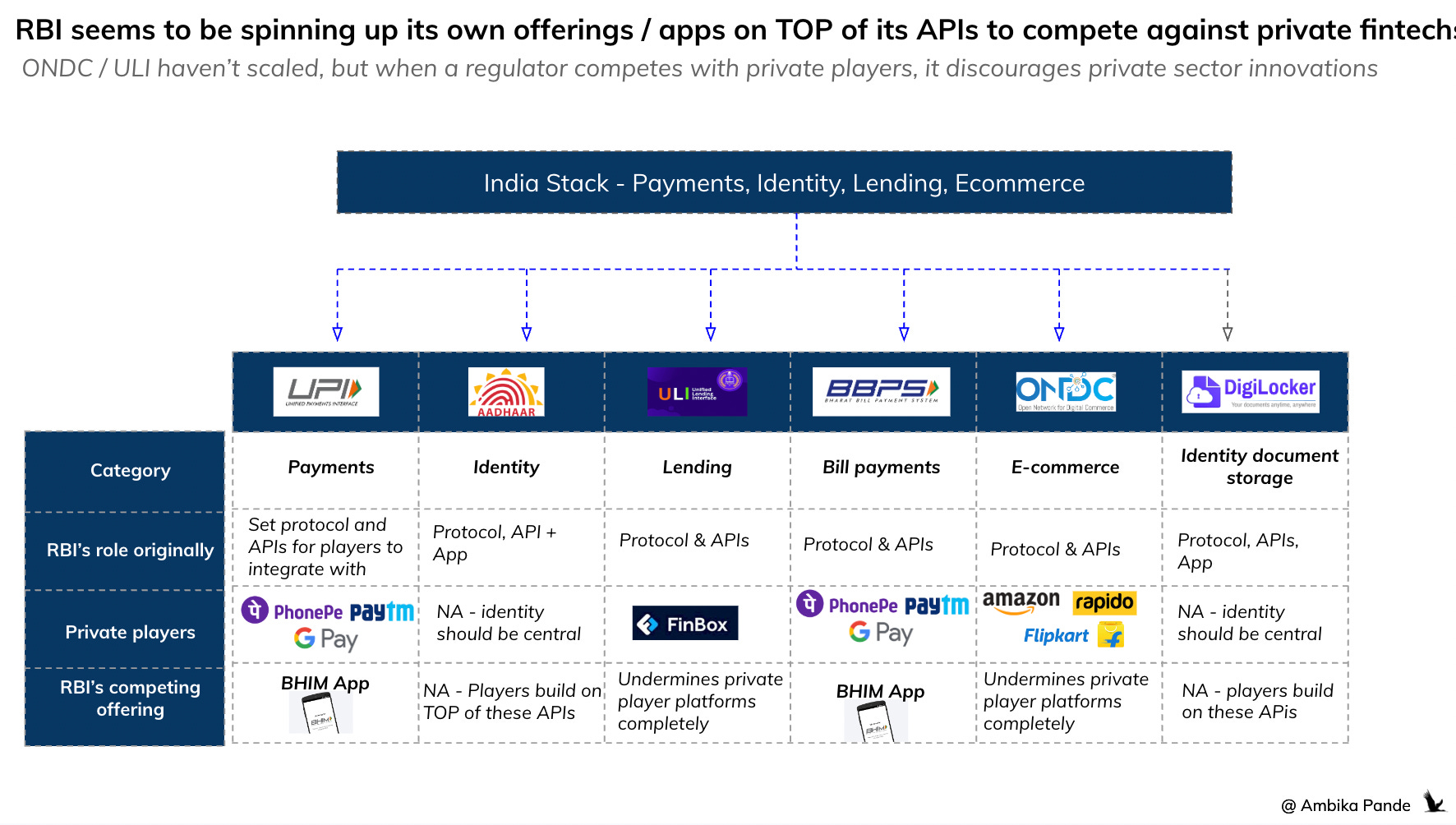

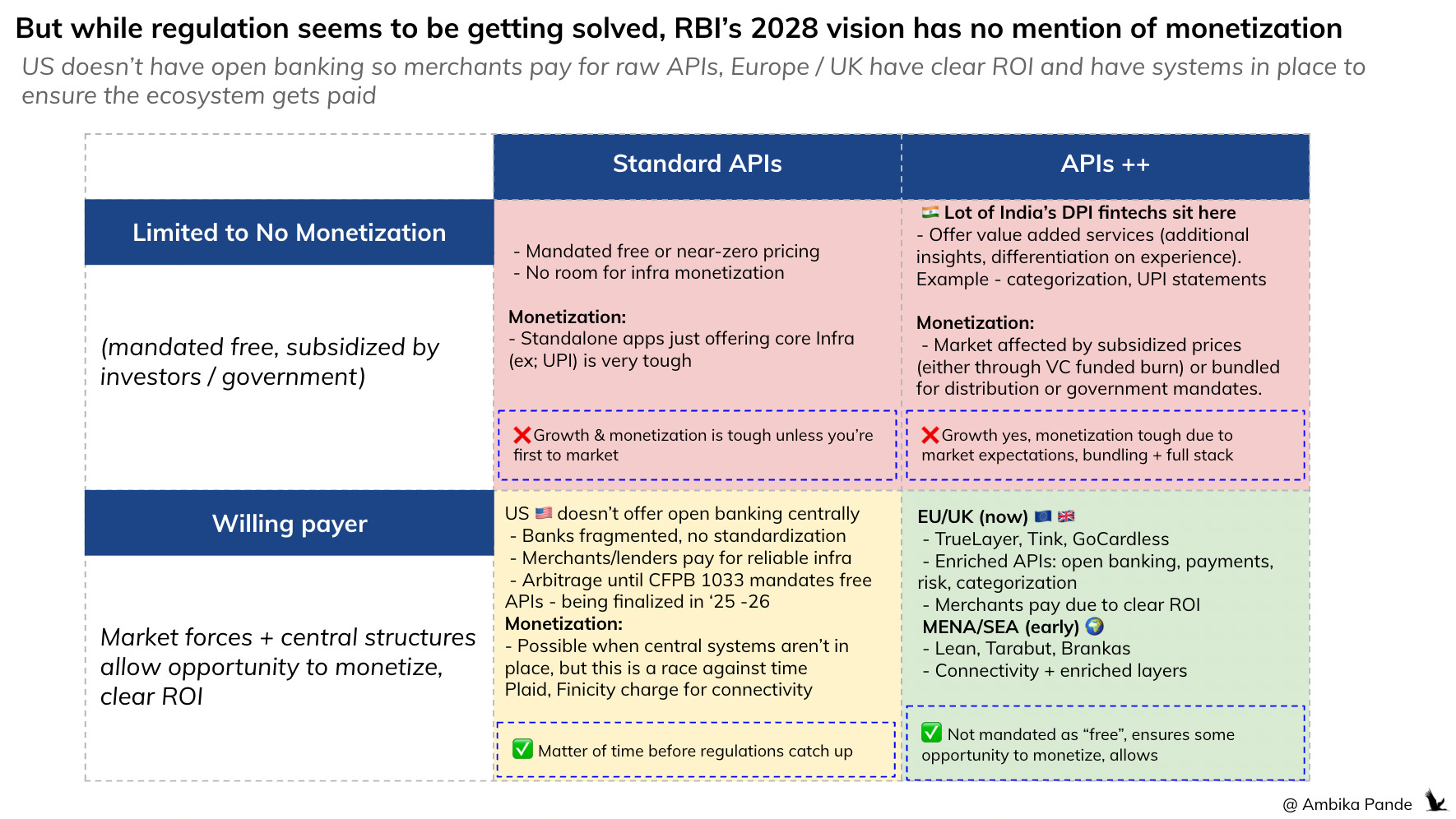

In my past articles on UPI, DPI, and monetization, my core thesis (which has increasingly beein validated) is that India’s DPI approach - UPI, Account Aggregator, ONDC, ULI builds world-class infrastructure and positions it as free public goods. This drives incredible adoption and inclusion. But it also compresses the entire monetizable surface area for private fintechs. And the strategy for adoption seems odd: look at what happened with UPI.

UPI originally was being pushed by NPCI via banks, not fintech apps. And by the way: in all other markets - Pix being an example (Brazil version of UPI) it is driven via bank apps. But in India, banks were slow to adopt. That is when fintechs came in: PhonePe, Paytm, Gpay, and drove adoption with the hope monetization will come in. Adoption happened, but monetization didn’t, so they had to pivot to doing other things: broking (share.market, Paytm Money), lending, insurance, and essentially everything under the sun.

And now, after UPI adoption has happened, and customer behaviour is set, NPCI is promoting its OWN UPI app called BHIM App, targeting a 5% market share.

So, it isn’t enough that the question of “structural profitability” is not being addressed. Now, RBI wants to launch competing products that will compete with these fintechs in the first place.

NPCI made ~1552 Cr of profit in FY25. PhonePe had a loss of INR 1727 Cr in FY25. NPCI can afford to promote its own app, give cashbacks, and sign up Dhoni to promote the app. I have heard customer feedback such as “The BHIM app is what a UPI App should be. It isn’t cluttered, and isn’t trying to cross sell multiple products to me.”

That is fair feedback. But it is also happening because for fintechs, they HAVE to make money, and they HAVE to cross sell. BHIM doesn’t have to, since it is essentially a government initiative.

When the reference price is zero, margins collapse. And to add to that RBI is now introducing its own competitors into the fray (ONDC, ULI along with BHIM are examples)

Standalone players can’t survive. Full-stack conglomeration becomes the only viable model. And innovation slows - not because fintechs lack capability, but because they can’t afford to build at those price points.

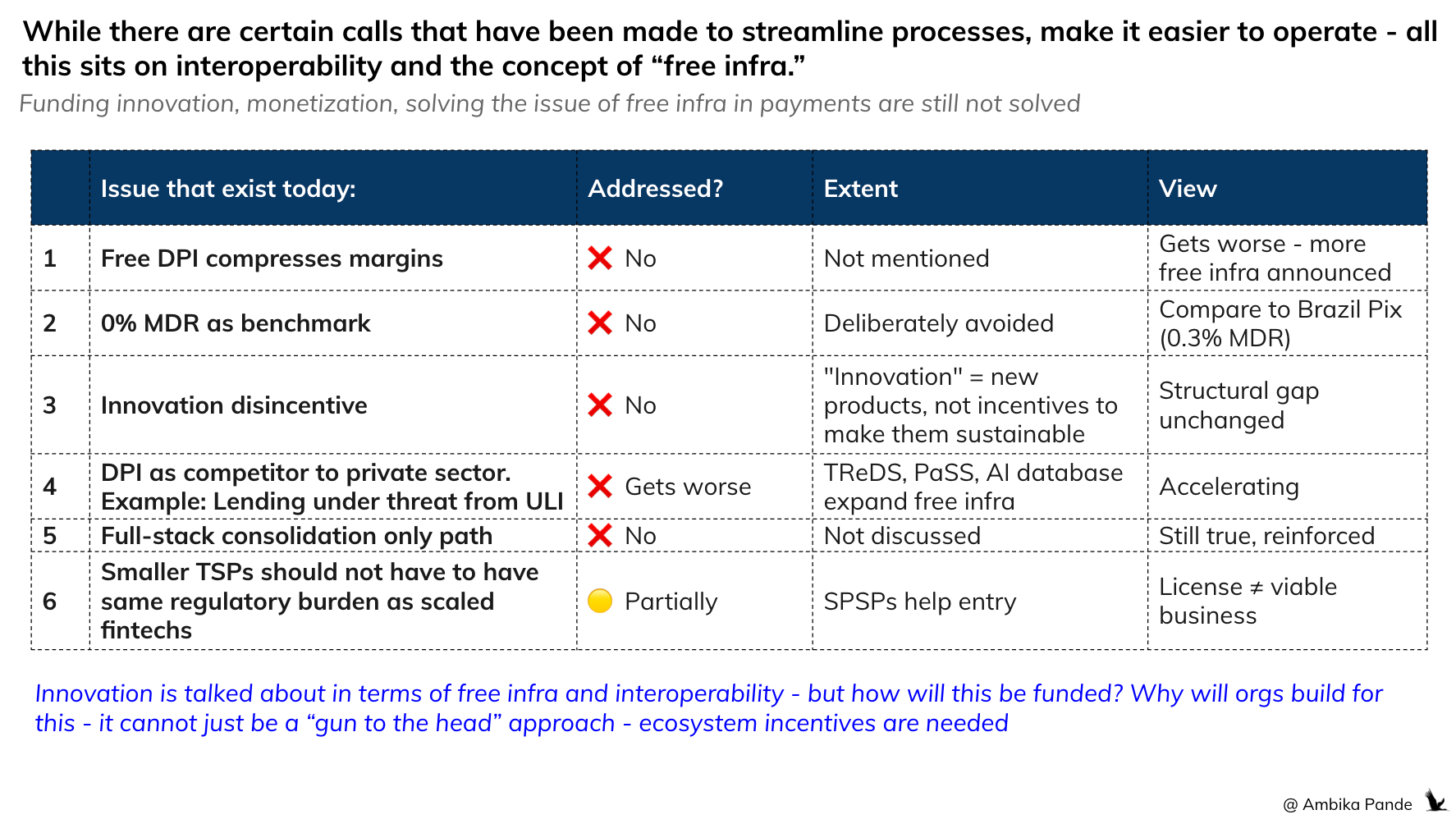

In fact, RBI has leaned into the whole “free infra” piece even more, by promoting interoperability, and not talking about monetization at all

🔴 Issue #1: Free DPI compresses margins not addressed: Not mentioned. Infact this gets worse, there is more “free infra” (assumed free due to absence of monetization framework) such as the AI powered payments piece. In fact, with the focus on “greater good” type initiatives, interoperability - somewhere, I’m questioning ohw sustainable this ecosystem is. We cannot keep relying on government subsidies. And let us be honest, in this whole “narrative” of keeping these as ‘public good’ it is the average Indian who is funding this from taxes. If I’m anyway paying for it (indirectly), then why not just make it into a framework that promotes innovation, instead of stakeholders having to rely on government handouts?

🔴 Issue #2: 0 MDR benchmark not addressed: There is nothing on pricing or a monetization focus in the fintech sector. Now, while there have been reports that the Standing Committee of Finance is evaluating some MDR on UPI (per calculations, global benchmarks are at 0.3% MDR, and UPI requires 0.15% per transaction to sustain the eecosystem. For calculation details, you can check out my article on this here: [#56] FY25 Budget Implications on UPI (Part 1): MDR on regular UPI transactions is now essential. But it is very surprising that despite all the chatter, all the proposals, there is nothing about this in the 2028 vision document for payments!

🔴 Issue #3: Innovation in products, but no incentives to make them sustainable: Interoperability in TreDs, the centralized payments data. Great initiatives, sure. Who’s going to pay for it? And then what incentives are there for businesses actually operating here?

🔴 Issue #4: DPI as a competitor to the private sector. This gets worse. TreDs, PaSS etc. Add to this the whole push of ULI, ONDC. The BHIM App piece that I already mentioned. What’s the point of waiting for innovation to come in and building a competing product centrally? This actually de-incentivizes any innovation here.

🔴 Issue #5: And because of the above, the whole issue of “full stack” being the only way forward, and it being an uphill battle for newer TSPs / players in the market to come in, since monetization depends on scale, is still not solved.

🟡 Issue #6: Smaller TSPs should not have the same regulatory burden as scaled up fintechs: This is partially solved with the Small Payment System Provider (SPSP) tag - which doesn’t make regulation a blocker atleast. But, regulation was only one half of the issue. Monetization was the other. No mention of this in the doc.

The verdict: RBI doesn’t just not address the margin problem - it doubles down on the same approach.

More free infrastructure, more standardized rails, more public goods. The SPSPs framework is a nice gesture for small players. But it’s treating the symptom (hard to get a license) rather than the disease (nothing to monetize once you have one).

A concern: The Agentic Payments blind spot

And now for what I find most striking. There is absolutely nothing in this vision about agentic payments, and agentic commerce in general.

Globally, this space is moving at breakneck speed. Stripe launched MPP (Machine Payments Protocol). Coinbase’s x402 has crossed 150M+ transactions. Google launched AP2 and UCP. Visa launched TAP. Mastercard has AgentPay and “Know Your Agent” protocols. Alipay hit 120M weekly agentic transactions. And in the machine payments world, stablecoins are becoming the default settlement rail — Stripe acquired Bridge for $1.1B, Mastercard bought BVNK for $1.8B, Visa partnered with Bridge for stablecoin cards.

And, an argument that could be made is: it’s because the Indian consumer - the average Indian consumer is quite some time away from using agentic commerce. And more immediate needs are: more access to credit, insurance, savings, and wealth management products.

But, the agentic economy is not just about consumers using AI. It is also about systems being upgraded, so that they are “AI native” or “AI friendly,” so we are prepared for the next decade.

In some of my past pieces, I’ve talked about how AI is a layer on TOP of existing systems and data. And if those systems systems, and data are not AI friendly (and what I mean by that is: systems for agent identity, systems build for agent querying, which will need higher TPS as compared to humans, data schemas being standardized), privacy and encryption guardrails built to protect against jailbreaks, AI will never work. Garbage in, garbage uut.

RBI’s Payments Vision 2028 mentions none of this. Zero. Not stablecoins. Not agentic payments. Not machine-to-machine transactions. Not autonomous commerce. Not AI agents initiating payments.

In a document about the future of payments through 2028, the fastest moving segment in global payments doesn’t get a single line. That is very surprising to me. Because, its not really about consumer behavior at this stage. It is about system capability.

👉 In Agentic Payments for example, the real test is whether banking systems can adapt to recognize new payment authorities - AP2 mandates, Visa TAP tokens, delegated credentials. If the issuer bank doesn’t recognize an agent-initiated payment instruction as valid, it doesn’t matter how elegant the protocol is. And it isn’t even about these protocols - it is about using the computing power of LLMs, and AI to improve experience, and optimize away inefficiencies. That requires structural changes. RBI’s vision document doesn’t even acknowledge these protocols exist. It talks about a central payments data system that can be queried using “AI” but it really start at the foundational level - that to do this, it will also require systems to be AI first.

I predicted that “friction is a feature, not a bug” and that fully autonomous payments are years away. RBI’s silence on agentic payments actually aligns with this view - they’re not building for autonomous agent payments because they don’t see it as imminent.

Maybe they’re right for now. But the infrastructure gap between India and markets where these protocols are being actively deployed will widen. And when the shift does come, India will be playing catch-up. So the answer, at least for the next three years in India, seems to be: the banking system won’t adapt, because the regulator isn’t asking it to. And that is where my trepidation lies.

👉 And on stablecoins specifically, there is absolutely no mention: This is particularly jarring given that RBI’s own FEMA amendment (October 2025) unlocked holding foreign currency accounts for exporters for more time (1 month to 3 months). The cross-border section of this document talks about reducing friction - but doesn’t once mention stablecoins as a settlement rail, even as every major global payment company and network is investing billions in exactly that.

Despite the above, there are some opportunities that can be inferred by reading of this document

Despite the gaps, and maybe partly because of them - there are real opportunities if you read between the lines.

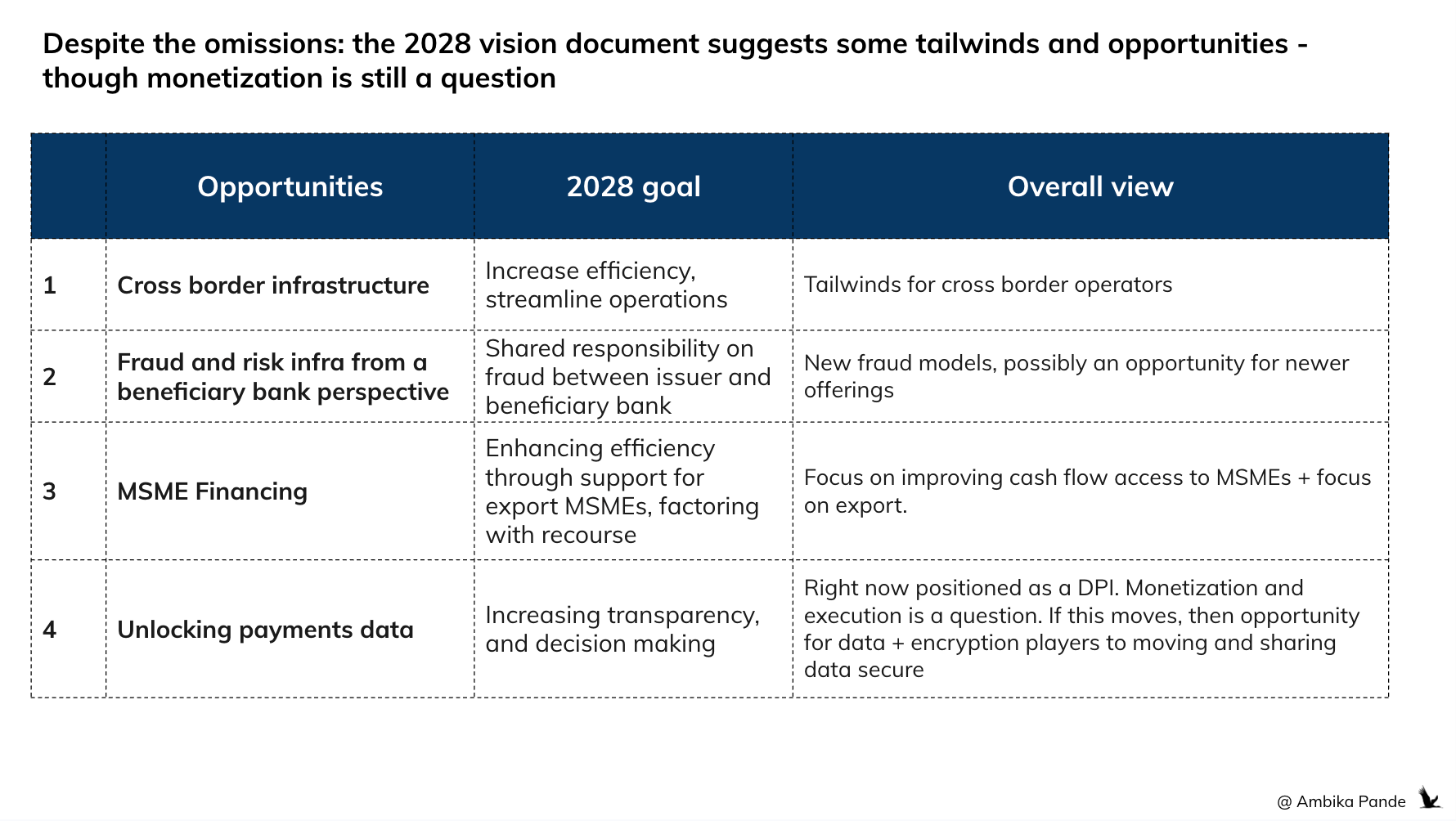

1. Cross border infrastructure - tailwinds

The single-window authorization is a genuine unlock. Anyone building cross-border rails: remittance, trade finance, FX, export payments should benefit from reduced regulatory friction. This helps both fiat-native models and stablecoin-settled models (like OpenFX, which settles FX on-chain with local fiat pools)

The FEMA simplification + TReDS interoperability + foreign currency account unlock is a three-part combo that could meaningfully expand the cross-border trade finance market. If you’re building in this space, the regulatory tailwinds are real. However, monetization questions etc are very real.

2. Fraud and risk infrastructure from a “beneficiary bank” perspective

Shared fraud liability + Cyber KRI framework = demand for fraud detection, risk scoring, and KYT (Know Your Transaction) tools. Every bank and non bank PSO will need better fraud infrastructure to manage their new liability exposure, from a beneficiary perspective. Before this document, the liability was 100% on the issuing bank.

3. MSME Financing via TReDS expansion

TReDS interoperability + export receivables access as well as factoring “with recourse” could be an opportunity for banks / NBFCs and especially some newer tech focused NBFCs to look at invoice discounting as a possible opportunity. The interoperability part isn’t great for the platforms that are facilitating this, but for lenders / financiers it reduces risk liability.

This could also signify tailwinds in the MSME financing space.

4. Enabling usage of payments data and analytics in a secure and monetizable way

While I’m not too bullish on this idea of a “central payments database” - I still have a lot of open questions on the practicality and execution of this. And the companies that have built proprietary payments data advantages could see that edge disappear - something like this is akin to “scaled up players” subsidizing efforts of newer competitors to build their own intelligence.

But it does look like that somewhere, the regulator view is that there is a lot of “alternate” data that can and should be used to improve risk models, lending, and so on. The opportunity then, are tools that enable this: data encryption and privacy, enabling computing on encrypted data and inference sharing without the raw data EVER moving. (Something that the company I current work at does by the way, so if you’re a payments company interested in exploring some of these options feel free to DM).

Now of course, a lot really depends on the opportunity to monetize this. If the view is that companies should share this free of cost, then good luck to everyone.

RBI Payments Vision 2028 is “payments plumbing” vision, not a “payments economy” vision. It talks about how money moves. It doesn’t talk about who makes money moving it.

Fraud accountability, cross-border simplification, this is all overdue, all welcome. It makes India’s payment infrastructure safer and more resilient. On those terms, it delivers.

But the structural issues that everyone who is a fintech operator has been talking about: margin compression, DPI crowding out private innovation, the zero MDR pricing problem, standalone players being squeezed out, remain completely unaddressed. If anything, this document reinforces that trajectory. More free infrastructure, more standardized rails, more public goods. The destination for Indian fintech stays the same: full stack conglomeration or death.

And the next wave of fintech innovation - stablecoins, agentic payments, machine to machine transactions, ensuring that systems are prepared for whenever this wave hits India, don’t exist in RBI’s worldview. The global payments stack is moving toward agent native, stablecoin settled, autonomous flows. India’s regulator is still building for a human to merchant, bank settled, friction as default world.

The opportunities are real - cross-border infrastructure, fraud tools, and MSME financing, But they’re at the edges, not at the core.